ChainThink

Stay ahead, master crypto insights

From Robinhood to xStocks, the Mechanism of Tokenization of US Stocks Revealed

From Robinhood to xStocks, the Mechanism of Tokenization of US Stocks Revealed

2025-07-03 09:43

After Trump's return to power, the U.S. regulatory environment has undergone significant changes, bringing a policy windfall for security tokenization. Platforms such as Robinhood, Bybit, and Kraken have entered the space, sparking a "Tokenized Stocks" wave, attempting to reconstruct the global asset trading logic through on-chain methods. This revolution of capital and crypto is driven not only by the ambition to disrupt traditional brokerage models but also by in-depth considerations of compliance strategies and product paths.

Three Main Models of U.S. Stock Tokenization

Current attempts at U.S. stock tokenization can be roughly divided into three paths: the "third-party compliant issuance + multi-platform access model" represented by Backed Finance; the "licensed broker self-operated closed-loop model" represented by Robinhood; and the "contract for difference (CFD) model" adopted by platforms like Bybit. These three paths differ not only in technical architecture but also represent different understandings of compliance responsibility, user relationships, and market structure.

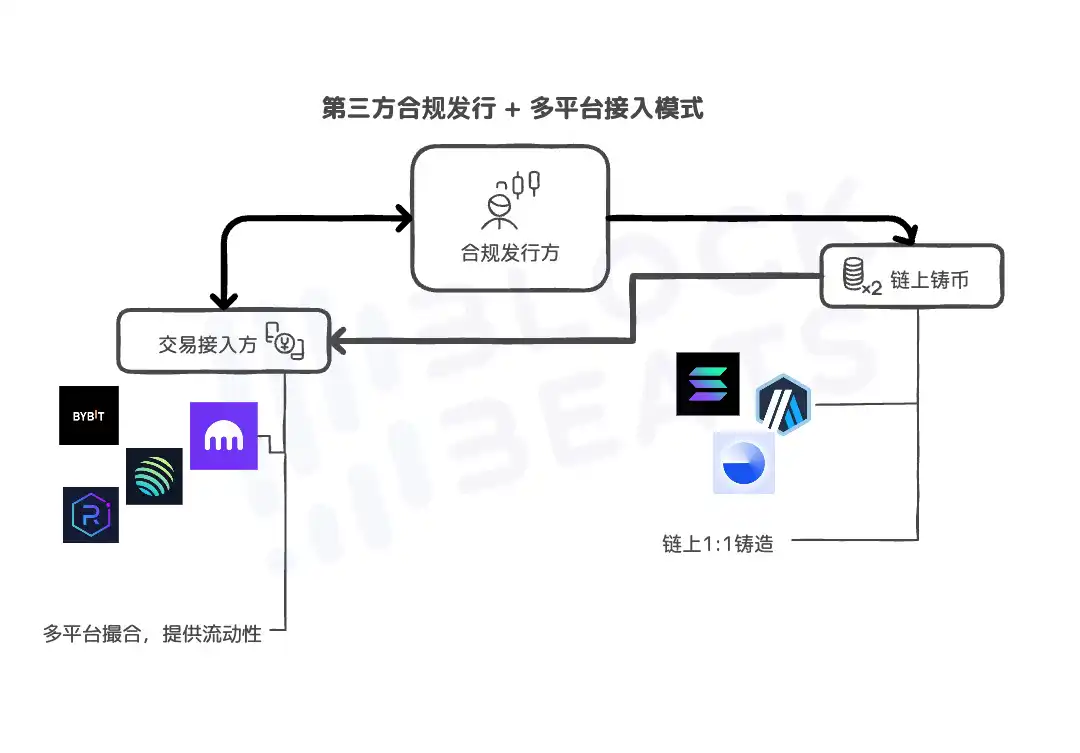

Third-Party Compliant Issuance + Multi-Platform Access Model

The core of this model is the separation of "compliant issuance and platform access." It is mainly led by xStocks, which recently formed an alliance with Kraken and Bybit. The specific operational path involves institutions such as Backed Finance, which hold Swiss or EU regulatory licenses, purchasing stocks in the U.S. market via the IBKR Prime channel and custodied under regulated custodians such as Clearstream and Interactive Brokers.

Once the stocks are actually purchased and accounted for, corresponding stock tokens (such as TSLAx, AAPLx, NVDAx) are minted 1:1 on public blockchains such as Solana (with future expansion to Ethereum ERC20), and provided with liquidity support and secondary trading matching services by cryptocurrency exchanges such as Kraken, Bybit, and Jupiter, both within their internal platforms and on the blockchain.

The greatest feature of this model is that "the issuer is the primary responsible entity," with all compliance requirements, asset transparency disclosures, and off-chain actual custody being undertaken by institutions such as Backed; platforms act solely as front-end access parties, without bearing the compliance pressure of security token issuance, thereby enabling large-scale compliant circulation in non-U.S. markets.

This path has advantages in clear asset ownership logic, with all tokens fully corresponding to actual shareholding, managed by custodians in separate accounts. It offers openness and liquidity, supports on-chain trading, 24/7 full-time trading, and can seamlessly integrate with DeFi applications, connecting smoothly with later extended "crypto-equity" DeFi protocols. Moreover, the compliance path is clear, requiring only the issuance end to have regulatory licenses, while the platform end, theoretically acting as a "distributor," can expand its business infinitely, quickly expanding into "non-U.S. markets."

In fact, as early as the late 2020s, FTX had attempted to tokenize stocks using this path. At that time, FTX allowed users to trade tokens of well-known U.S. companies such as Tesla (TSLA) and Apple (AAPL) on its platform. These tokens were issued by FTX's Swiss subsidiary Canco GmbH and were linked to real stocks held at third-party brokers, achieving a "1:1 pegged" mapping relationship.

At that time, users could participate in investing in popular U.S. stocks with as little as about $1, 24/7. To further "comply," FTX collaborated with German financial service providers CM-Equity AG and Digital Assets AG to jointly build a compliance framework, making these U.S. stock tokens legally valid and capable of financial integration. However, this business was halted in November 2022 when FTX declared bankruptcy due to serious issues such as fund misappropriation and fraud accusations.

This path also has obvious limitations. Although the SEC is not as "strict" as during the FTX period, it has not yet recognized the compliance of such products, so products based on this path are restricted to U.S. users. Moreover, because the path is easy to replicate, if major platforms fail to reach consensus, multiple "tokenized" stocks of the same company may emerge, resulting in fragmented liquidity.

Most importantly, trust in the issuer is still required. Although the custody system is independent, there is a "black hole period" (data falsification or delayed redemption) in the data disclosure and asset redemption by the issuer. For example, in the case of xStocks, the underlying issuer Backed, some doubts have emerged in the community. KOL Crypto Brave, "cryptobraveHQ" on X, expressed concerns about the background of Backed's team members. The three main co-founders of Backed, Adam Levi, Yehonatan Goldman, and Roberto Klein, were respectively the co-founder and former CTO, COO, and head of legal and regulatory affairs of the "zeroed out" project DAOstack. Crypto Brave further stated, "After raising approximately $30 million in the $GEN ICO, the team didn't even bother to list it, and after the token was issued, it was left to zero out."

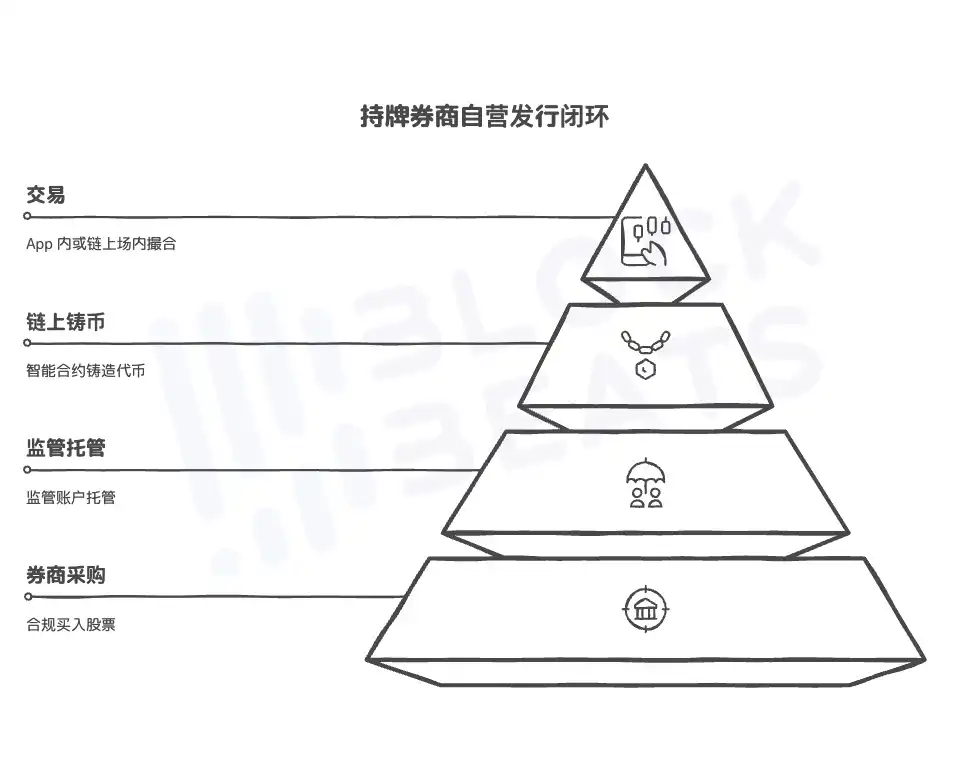

Licensed Broker Self-Issuance + Closed-Loop On-Chain Trading

The current project with the most complete planning of this path is Robinhood, which takes a more thorough "broker-driven on-chain model." Compared to the xStocks model, it does not rely on third-party compliant issuers but uses traditional broker licenses as a foundation, integrating the entire chain of stock procurement, token minting, user trading, and settlement.

Specifically, Robinhood's European subsidiary holds a Lithuanian securities license, allowing it to legally purchase and custody U.S. stocks, ETFs, private equity, and other assets. Subsequently, tokens (such as TSLA-t, APL-t) are minted on Arbitrum, and traded in a closed manner within its own app. Each token transaction synchronizes the on-chain state, with the backend inventory dynamically reflecting the actual shareholding situation, ensuring that "on-chain total = regulated custodial position." Robinhood plans to migrate this system to its self-developed Robinhood Chain in the future, achieving full on-chain autonomy and cross-chain transfer capabilities.

This path is difficult to replicate, as Robinhood itself, as a regulated entity, possesses full-chain capabilities including securities issuance, clearing, and dividend execution. Therefore, whether it is off-chain stock procurement, on-chain minting, or transaction settlement and fund flow, it can be completely controlled in a closed loop without relying on third-party custody or matching. Additionally, the business line is broader. Although it has only announced the tokenization of "OpenAI and SpaceX" stocks, from stocks to private equity, bonds, RWA, etc., Robinhood has the institutional basis and technical system for real assets.

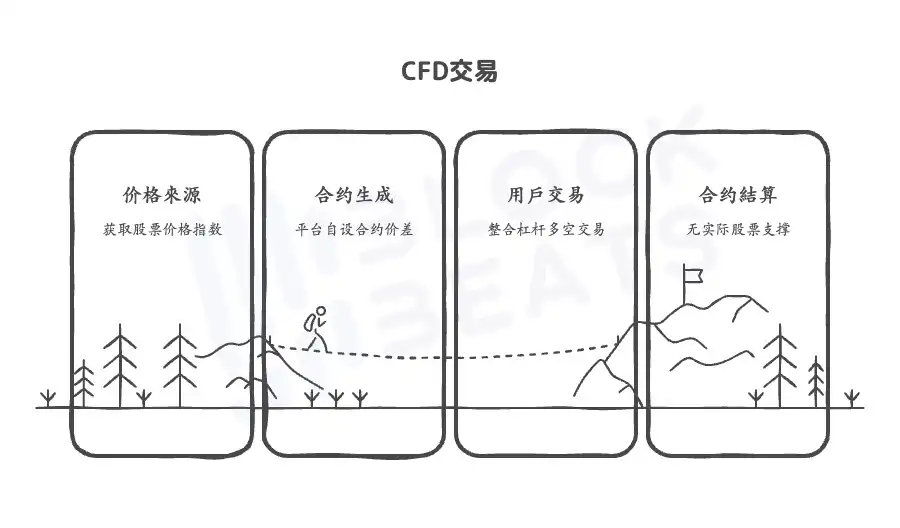

Contract for Difference (CFD) Model

The CFD path does not touch the stock assets themselves, but rather uses the stock price as an index source, and realizes price speculation through platform-designed contracts. For example, Bybit provides the TSLAUSDT perpetual contract, whose underlying assets do not hold any Tesla shares, but instead provide users with leveraged, bidirectional trading contract products based on oracle price sources and market-making logic.

The advantage of CFD is obvious, it is easy to deploy and quick to launch, and it does not require actual stock purchase or custody links, allowing any U.S. stock-related listing to be launched. After the launch of Bybit TradFi, users can trade most traditional financial assets on the Bybit App, such as oil, gold, stock CFDs, and foreign exchange, totaling over 100 assets, and supporting high-frequency trading, leverage operations, etc. Moreover, since it is not actual securities issuance, the platform operates according to derivative product regulatory standards.

However, the problems with this path are also obvious. CFD is not a true path in the sense of "tokenized securities," but rather a speculative response to the demand for U.S. stocks by crypto platforms. Users do not truly hold these assets, and the centralization risk is obvious, with the asset structure even posing greater risks than on-chain Memecoins.

Two Sides of One Path, Who Will Win Between Robinhood and Coinbase?

As the trend of U.S. stock tokenization intensifies, Coinbase and Robinhood, two fintech companies from San Francisco, have taken two distinct paths. One tries to break through U.S. regulatory barriers using technology and law, while the other starts from a brokerage and first implements closed-loop scenarios in Europe, gradually building a global tokenized trading network.

How Is Robinhood the First to Successfully Implement the "On-Chain Broker" Model?

Today, as global exchanges compete to explore tokenized stocks, Robinhood is no longer satisfied with the label of "zero-commission revolutionary," but is trying to reshape the entire traditional asset trading infrastructure. From the tokenized stock trading launched in Europe to the development of the Robinhood Chain for global developers, this American brokerage giant is advancing a deeper transformation at an unprecedented pace, allowing stocks, private equity, and even financial derivatives to fully enter the on-chain world.

Robinhood's on-chain strategy is far more than simply mapping real shares into tokens; it involves a deep restructuring around compliance licenses, on-chain clearing, and multi-market collaboration. This makes it fundamentally different from other crypto platforms that only provide token trading. Robinhood is the only one that has integrated "broker + Layer2 + real share custody" into a prototype of an on-chain broker.

Starting from Europe, Building the First Compliance Test Field for Tokenized Assets

In early June 2025, Robinhood completed the acquisition of Bitstamp, a Luxembourg-based cryptocurrency trading platform, for $200 million in cash. This move added over 50 licenses and registrations to its cryptocurrency department, as well as a mature institutional exchange with over 5,000 institutional clients. Meanwhile, in May, Robinhood announced its acquisition of Canadian cryptocurrency platform WonderFi for approximately $179 million to strengthen its business in the Canadian market. With this, Robinhood has secured an important piece of the puzzle in its "U.S. stock tokenization" plan.

By the end of June, Robinhood announced the launch of a stock token trading platform based on Arbitrum in 31 European countries, with over 200 U.S. stocks and ETFs listed initially, and plans to expand to unlisted company equity tokens such as SpaceX and OpenAI. These tokens are fully held and minted by Robinhood, ensuring a 1:1 correspondence with real shares, and supporting real-time dividends and stock splits simultaneously.

Different from previous centralized platform attempts, Robinhood did not rely on third-party issuing institutions but used its European subsidiary's Lithuanian MiFID securities license to purchase real stocks within the compliance framework and place them in regulated accounts, building its own custody-minting-trading closed-loop process. In addition, Robinhood did not stop at upgrading the token trading interface but also upgraded the original Robinhood Crypto App to a comprehensive investment platform, integrating perpetual contract trading, cryptocurrency management, on-chain staking, and AI investment assistants into one app, providing a complete investment toolkit to accompany user migration.

Familiar? Phase One - Token Issuance, Phase Two - Finding Liquidity, Phase Three - Decentralized Finance

But European business is just the first step for Robinhood. The launch of Robinhood Chain is a comprehensive declaration of the future form of the asset internet. This Layer2 network, built in collaboration with Offchain Labs based on Arbitrum, not only carries the trading and settlement functions of all Robinhood tokenized assets, but will also open up to global third-party developers, forming an on-chain ecosystem centered around real asset issuance.

Its underlying design logic is divided into three phases: the first phase, where Robinhood brokers purchase real shares and custody them before minting on-chain tokens; the second phase, introducing Bitstamp as a supplementary liquidity source, allowing token trading to continue even during weekends when traditional markets are closed; and finally, users can self-custody Robinhood-issued token assets and migrate them to other chains or DeFi protocols for use.

Throughout this process, Robinhood controls the purchase right, custody right, minting right, trading entry point, and user relationship, thus achieving the on-chain closed-loop of "tokens ≈ stocks." The blockchain is just the accounting layer, with all actions synchronized off-chain. This model sacrifices the transferability of tokens but greatly enhances regulatory controllability, paving the way for its subsequent expansion to Robinhood Chain, a public chain compatible with traditional finance and blockchain assets globally.

Robinhood's logic is that, since I am a broker, I will buy stocks myself, store them myself, and mint them myself. Throughout the process, Robinhood controls the purchase right, custody right, minting right, trading entry point, and user relationship, thus achieving the on-chain closed-loop of "tokens ≈ stocks." The blockchain is just the accounting layer, with all actions synchronized off-chain. This model sacrifices the transferability of tokens but greatly enhances regulatory controllability, paving the way for its subsequent expansion to Robinhood Chain, a public chain compatible with traditional finance and blockchain assets globally.

This means that Robinhood is no longer just a terminal trading platform but is transitioning into a "on-chain broker base" that integrates asset issuance, clearing, and trading. Particularly worth noting is Robinhood's layout in private equity. Its tokenized issuance not only breaks down the high threshold structure of traditional private equity investment but may also change the liquidity logic of early-stage tech equity, forming a new species similar to a "crypto primary market." The "ICM" that Solana has been shouting about recently may be realized on this traditional broker side.

Coinbase: Starting from the Blockchain, Seeking "Exchange + Compliant Issuance" Synergy

Although it has not yet launched stock business, Coinbase, which recently acquired Circle and brought its perpetual contract business back to the U.S., cannot be ignored here. In fact, Coinbase's logic is another path: first building the infrastructure, then lobbying regulators, seeking licenses, exemptions, or precedents, and then proceeding with asset tokenization.

According to Reuters report, on June 17, Coinbase's Chief Legal Officer Paul Grewal stated that relying on its own Base blockchain and Layer2 technology stack, as well as Dormant's broker-dealer (not yet activated securities brokerage entity), it has applied to the SEC for a no-action letter, hoping to obtain legal exemption for tokenized stock products.

Coinbase's plan is that once approved by the SEC, it can issue tokens representing equity on the blockchain, and with on-chain smart contracts, complete T+0 settlement, fractional share splitting, and real-time dividends. Its native stablecoin assets, native Layer2 Base, and already top-tier institutional exchange will bring significant advantages on the "sales side."

Compared to Robinhood's "post-regulation" approach, Coinbase chooses the "compliance-first" path. This reflects its sensitivity as a publicly listed company in the U.S. and is also a high-risk strategy that, once broken through, could capture the largest market share in the U.S.

Technology vs License, Open Source vs Closed Loop: Who Will Win the Last Mile?

From the underlying structure, Robinhood is an "license-driven" on-chain broker, while Coinbase is an "infrastructure-driven" on-chain platform. The former follows a closed-loop control path, while the latter seeks open collaboration.

Robinhood currently has full-chain qualification for securities issuance and stronger capabilities in connecting with fractional shares and real equity; while Coinbase, although not yet achieving actual issuance, has a more mature technology level in its Base blockchain and deeper matching depth on the exchange side, giving it the potential to become a "global on-chain securities standard network."

This showdown ultimately comes down to a multi-party coordination game of who can convince users, regulators, and the market. If Robinhood can connect on-chain liquidity and multi-platform collaboration, and if Coinbase can get the green light from the SEC, it may directly become the traffic entrance for tokenized equity in the U.S. market. One starts from the traditional industry, the other from cryptocurrency, the route competition for the future of on-chain securities has just begun.

Although tokenized stocks have made significant progress in technology, compliance, and user experience, they still face several challenges in scaling, such as fragmented liquidity, high hedging difficulty, complex on-chain dividend and governance, and differing regional regulations. However, looking at the trend, with the entry of major players with compliance qualifications such as Robinhood and Coinbase, tokenized stocks will move from "gray experiments" to "legal entry points," and the next stage of asset transformation may be coming soon.

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

FusnChain

FusnChain