ChainThink

Stay ahead, master crypto insights

AAVE Yields Leadership Position — Who Will Replace AAVE as the New King?

AAVE Yields Leadership Position — Who Will Replace AAVE as the New King?

2026-04-24 10:53

Ethereum and Solana's lending landscapes have followed remarkably similar scripts, with the only truly comparable phase transition (Phase 1 to Phase 2) occurring approximately 25% faster on Solana. The third phase has just begun, and whether Solana can sustain this momentum remains uncertain.

Ethereum Phase 1 to Phase 2 (from Compound’s peak to Aave’s dominance): ~2 years

Solana Phase 1 to Phase 2 (from MarginFi’s peak to Kamino’s dominance): ~18 months

Both ecosystems are now in Phase 3, with new challengers steadily closing the gap.

But this time, I don’t believe the outcome will be the same. The following explains why, step by step.

Phase 1: The Reign of Compound and MarginFi

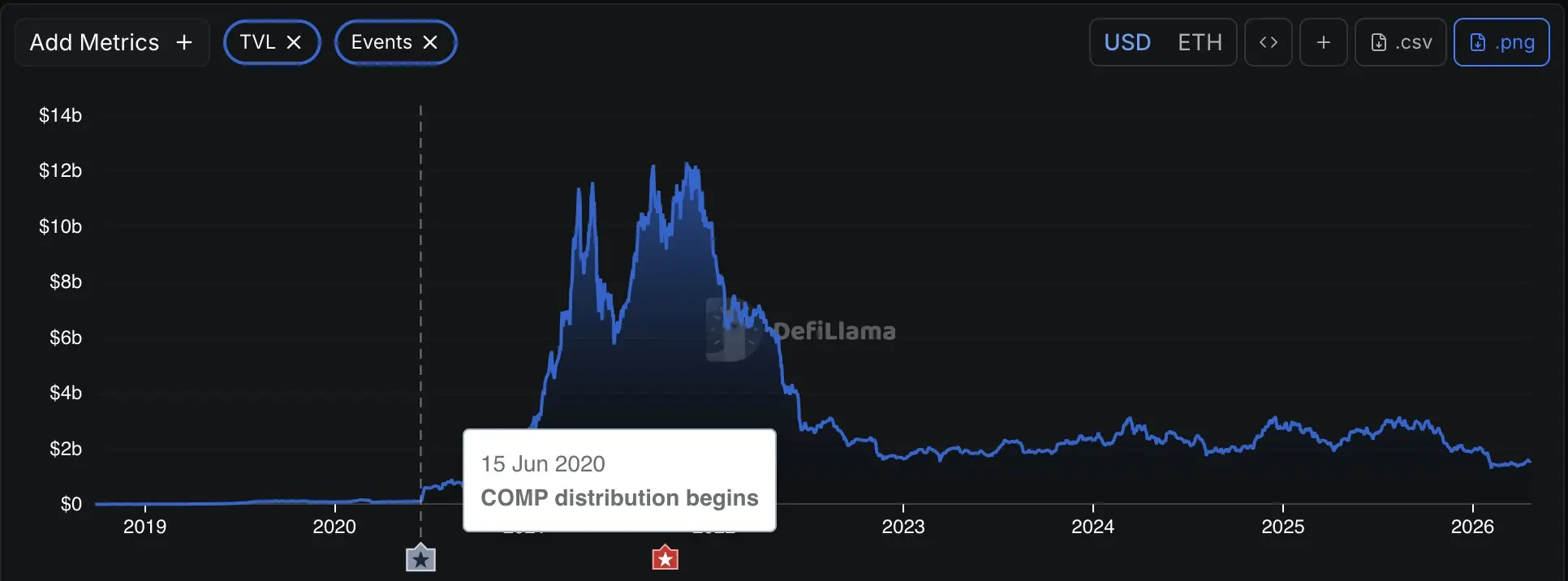

Ethereum: Compound was the protocol that truly ignited the "DeFi Summer." The launch of COMP token in June 2020 directly triggered the entire liquidity mining era. At its peak, Compound’s TVL was roughly five times that of Aave.

Solana: After FTX’s collapse, MarginFi launched a long-term token allocation program centered on future airdrops, successfully attracting massive capital. Its peak TVL was about four times that of Kamino.

The early dominance of both leaders was driven primarily by token incentives and airdrop expectations—not deep product fundamentals. Once market sentiment shifted, this distinction became critical.

Phase 2: The Rise of Aave and Kamino

Ethereum: Compound’s TVL was essentially composed of mercenary capital. During the 2022 bear market, collateral values plummeted, causing COMP to crash simultaneously—mining yields were no longer sufficient to retain capital.

The erosion of trust began earlier—September 2021 saw a governance vulnerability leading to an over-distribution of approximately $90 million in COMP tokens. Such events leave lasting impressions on users. The final blow came in 2023 when founder Robert Leshner publicly announced a strategic pivot toward Superstate, signaling that the core team had effectively abandoned the protocol.

Aave surpassed Compound due to several tightly interconnected factors. It rapidly onboarded new collateral assets, particularly stETH, wstETH, and weETH, making it the default hub for Ethereum LST borrowing and lending cycles. It also initiated cross-chain expansion early, deploying natively on Polygon and Avalanche through strategic partnerships.

Purely incentive-driven models often exhaust token treasuries or destabilize token prices, but Aave leveraged partner chains to achieve compounding growth in users and TVL without depleting its own budget.

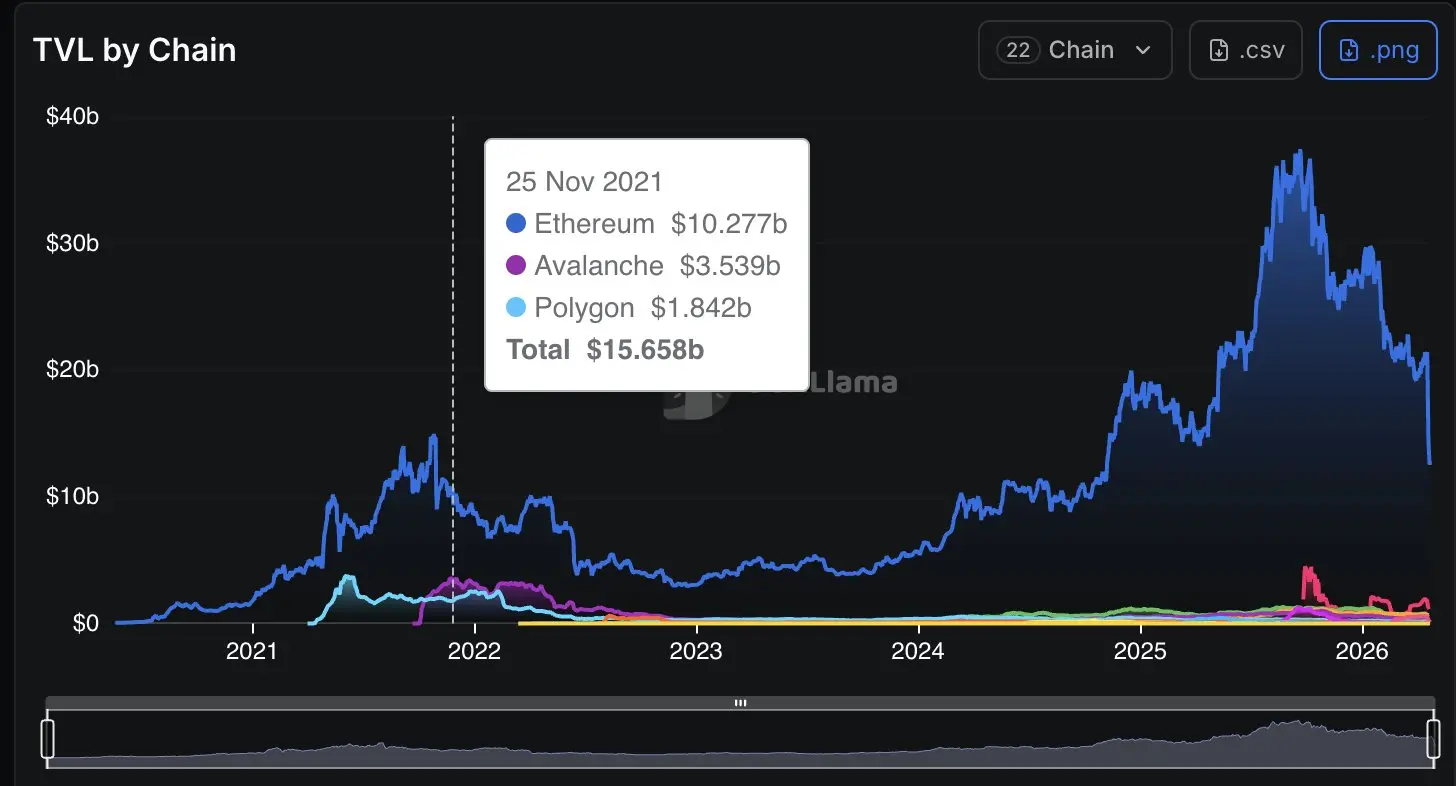

It also possessed genuine product depth: flash loans (a feature Compound never launched) and a security module that created real demand for the AAVE token via staking. Today, Aave’s TVL stands at around $16 billion, while Compound’s is only about 10% of that.

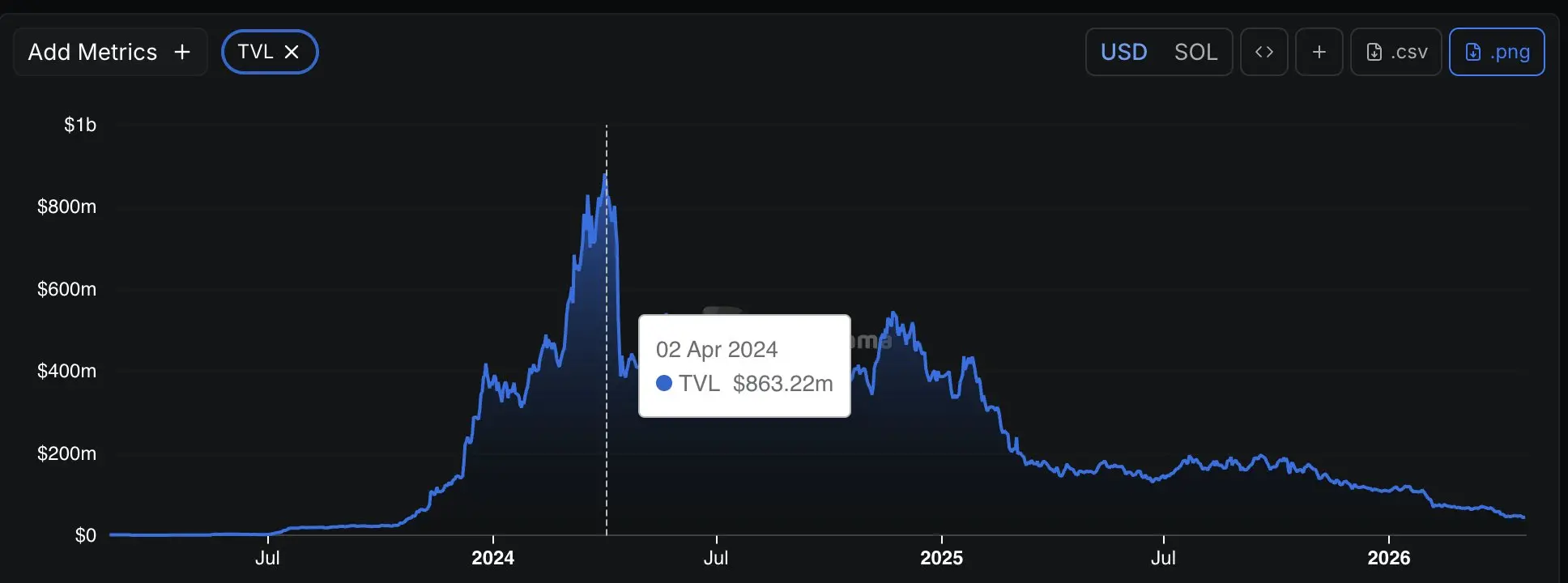

Solana: MarginFi’s decline stemmed from a prolonged and delayed airdrop campaign. Users provided liquidity, only to wait indefinitely for a token distribution that ultimately arrived under unacceptable conditions—culminating in widespread frustration and mass exits.

Kamino’s rise was more structural than incentive-driven. Initially not a lending protocol, it was built as a management tool around concentrated liquidity vaults; the lending markets evolved alongside it.

During Solana DeFi’s resurgence from 2023 to 2024, new assets flooded in—LSTs (jitoSOL, bSOL), yield-bearing tokens (JLP), and stablecoins (PYUSD). Kamino’s positioning was perfectly aligned: it offered vault products for managing DEX liquidity, lending markets that gave utility to new assets, and Multiply—a product specifically designed for circular lending.

This made Kamino the preferred destination for asset issuers deploying incentives on Solana. If you’re launching a new LST or stablecoin on chain, Kamino is often your first integration point.

Today, Kamino’s TVL is approximately $1.6 billion, compared to MarginFi’s $45 million—just 3% of Kamino’s total.

Kamino’s TVL growth is primarily driven by integrations with new LSTs, stablecoins, and yield-bearing assets.

Phase 3: Morpho and Jupiter Lend Emerge

This month, both Aave and Kamino faced external shocks. Kamino had no direct exposure to the Drift incident (dSOL was not compromised by hackers), yet depositors withdrew approximately $300 million as a precautionary measure.

Aave suffered a heavier impact—rsETH was widely used as collateral for circular lending on Aave, causing TVL to drop from ~$26 billion to ~$16 billion.

The ratio changes were as follows:

Morpho vs. Aave TVL ratio: from 26% to 42%

Jupiter Lend vs. Kamino TVL ratio: from 50% to 60%

Headline protocols suffering external shocks does not mean they’ve been outcompeted. This reveals a hidden truth in the lending space: the top projects hold the most trusted collateral (weETH, rsETH, JLP)—precisely because they are leaders. Everyone naturally gravitates toward winners.

In good times, this concentration drives TVL growth; but when a key integrated asset fails, the leader suffers the most severe consequences due to its own success. The challenger’s strong metrics appear favorable only because their risk exposure is smaller—an illusion caused by lagging indicators, not structural advantage.

Why I Don’t Believe the Outcome Will Be the Same This Time

The foundations of current market leaders are genuinely solid. Compound and MarginFi were self-destroyed: Compound fell due to sluggish governance and founder departure; MarginFi collapsed due to unfulfilled airdrop promises.

Morpho is infrastructure; Aave is a product. Morpho Blue provides an immutable, permissionless mechanism for creating markets, with vault risk managed independently by curators (Gauntlet, Steakhouse, MEV Capital).

Aave operates as a single monolithic liquidity pool governed via on-chain voting—essentially a super-curator. Morpho’s bet is that risk management should be decoupled and white-labeled, not about building a better Aave.

Jupiter Lend is a feature within a super-app; Kamino is a standalone product. Jupiter retains users within its ecosystem, covering DEX aggregation, perpetual contracts, prediction markets, stablecoins, LSTs, and now lending.

Users don’t need Jupiter Lend’s rates to be the absolute best globally—they just need adequate rates in a familiar environment. Its moat lies in distribution channels, not product excellence.

What Would Change My Mind

If Aave v4’s modular architecture fails to gain meaningful market adoption, and Aave v3 becomes marginalized.

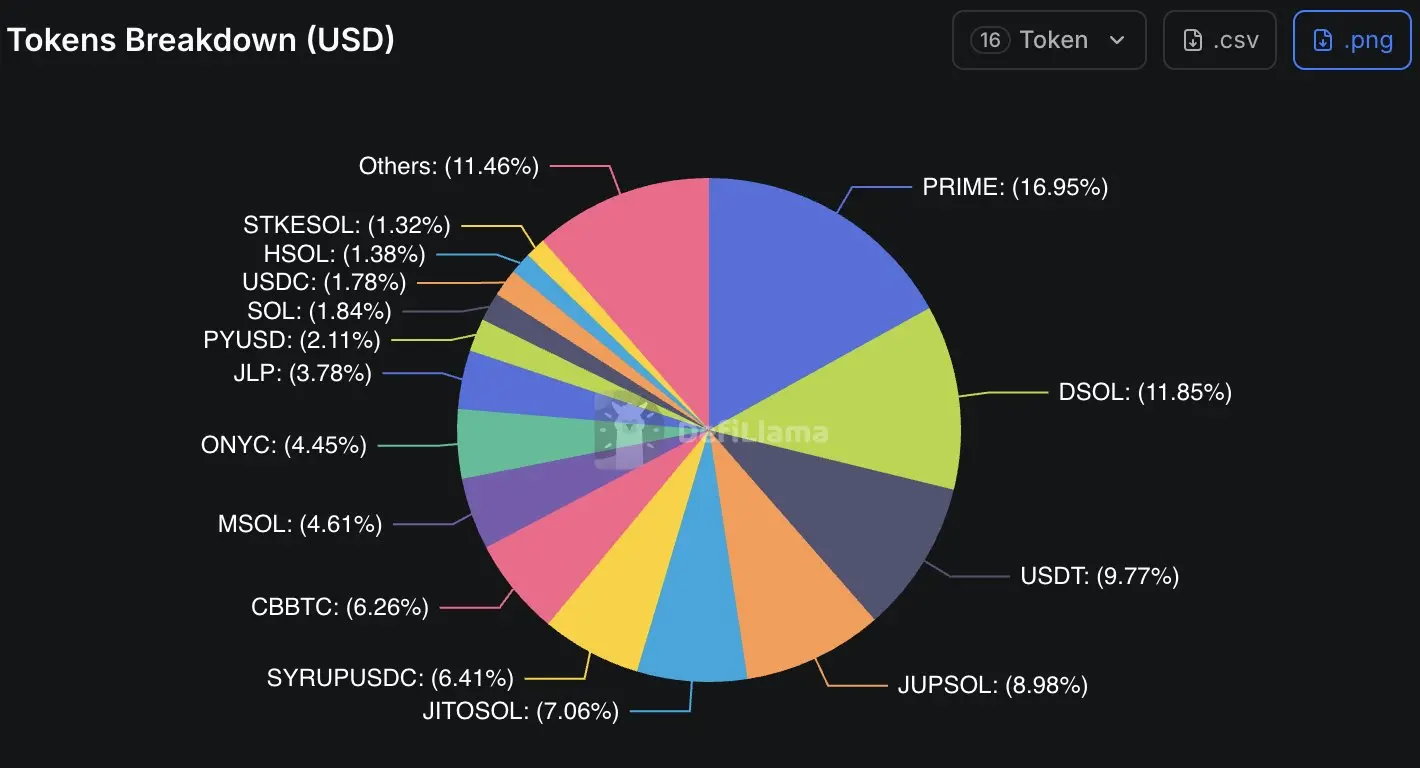

If one of Kamino’s largest collateral assets, PRIME, experiences a major failure. Currently, PRIME represents 20% of the protocol’s total size.

Core Lessons for Protocol Growth

Reliance on internal incentives alone cannot scale a lending market. Aave and Kamino’s success has been built on co-growth with ecosystem partners (blockchains and asset issuers). Pure incentive spending often drains budgets or collapses token value before product depth is established.

In early stages, narrative velocity and business development (BD) execution matter more than protocol depth.

Aave was first to list stETH, wstETH, and weETH, then partnered with Ethena on sUSDe recycling, with Maple on syrupUSDC, and with Pendle on PTs.

Kamino has been the first to integrate nearly every major Solana LST and stablecoin upon launch. In both cases, rapid capture and execution of narratives—not just technical features—have been the true competitive edge over years.

Author: Tom Wan

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

FusnChain

FusnChain