Talks stalled again, U.S. stocks pull back from highs, can Bitcoin hold the $80,000 level?

Talks stalled again, U.S. stocks pull back from highs, can Bitcoin hold the $80,000 level?

Following Axios's exclusive report on "both sides nearing a deal" the previous day, markets briefly basked in optimism, with the S&P 500 hitting a new all-time high and the Nasdaq simultaneously breaking its record. On Wednesday, the S&P 500 surged 1.46% to close at 7,365.12, while the Nasdaq soared 2.02% to reach 25,838.94—both marking historic closing highs.

This positive sentiment didn’t last 24 hours.

The Iranian Foreign Ministry spokesperson stated on Wednesday that Washington’s peace proposal remains under review, with two core demands—freezing uranium enrichment and reopening the Strait of Hormuz—still unresolved. Iran’s red line on uranium retention remains unchanged. The accumulated long-side confidence from the prior day was swiftly eroded by this news, triggering a reversal in risk sentiment. All three major U.S. indices closed lower, with the semiconductor sector leading the decline, and small-cap stocks bearing the heaviest burden.

Core Narrative: Peace Agreement Still Far Off

Market interpretation of the conflict has become highly binary—either a deal is struck, or fighting continues.

This week’s diplomatic rhythm generated significant volatility. On Monday, Trump announced the suspension of the “Freedom Operation” escort mission; Pakistan as intermediary relayed positive signals. On Tuesday, Saudi media even speculated that access rights through the Strait of Hormuz could break through within “hours,” prompting oil prices to plummet—West Texas Intermediate (WTI) dropped over 5% intraday, and Brent crude fell below $97.

But Iran quickly cooled down. The Iranian Foreign Ministry explicitly declared uranium enrichment as a red line, not a bargaining chip. Concurrently, the Islamic Revolutionary Guard Corps announced plans to establish a new “control system” over the Strait of Hormuz, implying that even if passage were reopened in the future, it would be selectively managed under Iranian dominance rather than restored unconditionally.

Meanwhile, the U.S. Treasury Department announced additional sanctions targeting Iran-linked oil networks on the same day. Reports also indicate that U.S. forces used force against an Iranian oil tanker violating the blockade within the strait. Economic pressure and military deterrence are being applied in tandem, signaling no sign of U.S. retreat.

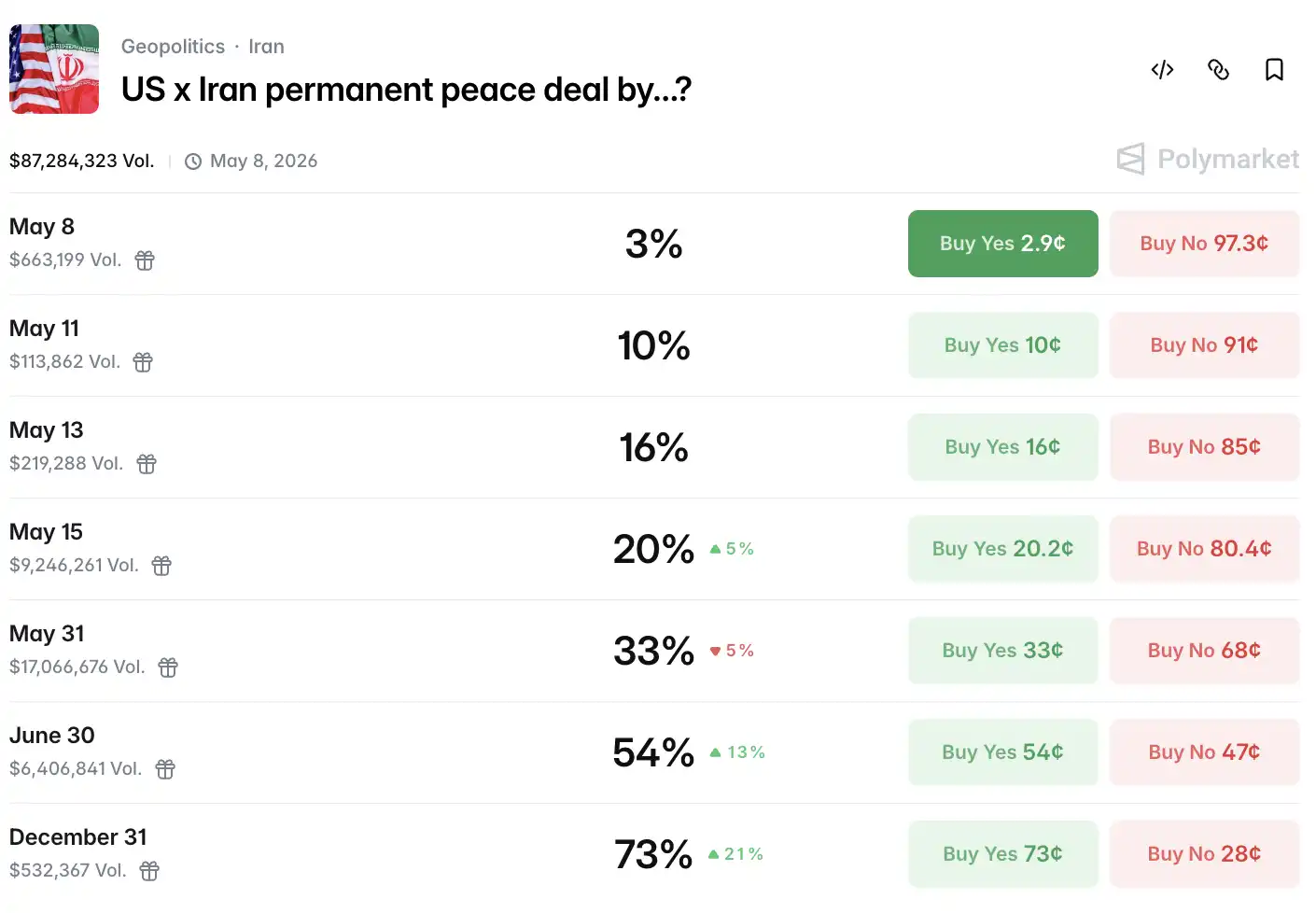

Polymarket data shows the probability of a peace agreement by May 15 has fallen to 15%, rising slightly to 20% at press time.

Thus, oil prices carved out a sharp V-shaped reversal.

Intraday, Brent crude futures plunged to $96.73—down over 12%. As talks deteriorated, longs re-entered the market, and Brent settled near $100 by the close, while WTI ended around $90.5, both narrowly holding key psychological levels.

Notably, spot Brent has now dipped below the front-month futures contract—a reversal of the contango structure, signaling that physical crude supply is relatively abundant in the current market, creating a structural divergence from the risk premium priced into futures driven by geopolitical tensions.

Outside the strait, U.S. crude exports hit an all-time high last week, as global buyers accelerate shifting toward American supply sources to avoid Middle East shipping risks.

Meanwhile, Aldo Spanjer, Head of Energy Strategy at BNP Paribas, has outright abandoned trading energy markets: “The outcome is too binary—headline-driven triggers are setting off stop-losses. This has happened five times this week alone—trading is nearly impossible.” Scott Shelton, energy analyst at TP ICAP, described the current environment as a “risk desert,” where only hedgers remain in the market.

Can Bitcoin Hold the $80,000 Mark?

Turning to the asset most closely watched by crypto investors—Bitcoin.

Bitcoin continued to face downward pressure amid this backdrop, with spot Bitcoin declining approximately 1.56% during the day and finding support near $80,000.

Differing from prior rounds of panic selling, this correction exhibited a relatively healthy structure. On-chain data reveals that long-term holders’ share has risen to 78.3% of circulating supply, exchange balances have declined to a seven-year low, and whale addresses have net bought roughly 270,000 BTC over the past 30 days. BlackRock’s Bitcoin ETF holdings have climbed to approximately $62 billion, indicating a stabilizing institutional ownership structure.

On Ethereum, overall sentiment benefited from rising expectations around U.S. crypto regulatory legislation, with ETH gaining about 5.6% over five days, trading in a range of $2,360–$2,412, and market cap remaining around $233 billion.

Notably, April marked the strongest single month of net inflows for U.S. spot Bitcoin ETFs since October 2025, with $2.44 billion in net inflows. Institutional pipelines continue to open, which aligns internally with Bitcoin’s relative resilience amid macro turbulence.

From a narrative perspective, the impact of the Middle East situation on the crypto market is showing structural divergence. Rising oil prices and renewed inflation concerns have increased expectations of Fed rate hikes, pressuring Bitcoin. Yet simultaneously, capital from certain Middle Eastern regions is accelerating migration into decentralized channels to hedge against potential sanctions and liquidity constraints in traditional banking systems. On the same day the U.S. Treasury added sanctions to Iran-linked oil networks, on-chain data showed a minor spike in anonymous mixer transaction volume—not a conclusion, but a signal worth continuous monitoring.

On the regulatory front, market expectations around the rollout of a U.S. regulatory framework are supporting sentiment. The stablecoin and digital asset market structure bills in both the House and Senate are progressing. If enacted this year, they would provide crucial compliance scaffolding for institutions to further expand their allocations.

Equities Trade Higher with Semiconductor Reversal

Wednesday marked the second directionally ambiguous trading session of the week.

The S&P 500 closed down 0.38% at 7,337.11; the Dow lost 313.62 points (-0.63%) to finish at 49,596.97; the Nasdaq posted a more restrained decline of 0.13%, closing at 25,806.20. The Russell 2000 small-cap index dropped 1.63%, the largest decline among major indices.

All sectors closed lower, with energy suffering the steepest losses, while consumer staples held relatively firm.

Within tech, performance diverged sharply. Tesla rose 3.28%, Nvidia gained 1.76%, Microsoft advanced 1.68%, Meta added 0.64%; Apple slipped 0.03%, Alphabet declined 0.01%, Amazon dropped 1.39%. The Big Seven composite index rose marginally by 0.69%, one of the few bright spots of the day.

Semiconductors were hit hardest. The Philadelphia Semiconductor Index closed down 2.72%, with AMD shedding 3.07%, TSMC ADRs dropping 1.28%. Qualcomm and Fortinet beat earnings expectations, and Datadog’s analyst day provided some support to software stocks—the software index is poised to end the fourth consecutive week in the green—but this masked the systemic sell-off in the chip sector.

Goldman Sachs trading desk data offered a more striking dimension: the high-beta momentum portfolio fell 8% on the day, while the S&P 500 and Nasdaq 100 declined by less than 0.5%—a dispersion gap ranking among the top ten worst daily extremes over the past five years, and already occurred five times this year.

Additionally, the VIX fell 1.78% to 17.08, exhibiting a rare divergence from equities' downturn. Typically, falling stocks drive up the fear index; here, both moved lower together, suggesting the market may be awaiting Friday’s nonfarm payroll data, reluctant to take directional bets in the short term.

Recent earnings reports from U.S. stocks were particularly telling. Arm Holdings released FY2026 Q4 results after the market close on May 6, reporting adjusted EPS of 60 cents and revenue of $1.49 billion—slightly exceeding analyst estimates. Licensing revenue grew 29% year-over-year, royalty revenue rose 11%.

The numbers themselves weren’t poor. However, during the earnings call, management noted that the company’s latest AGI CPU data center chips faced supply bottlenecks, with an additional $1 billion in demand temporarily unconvertable into revenue. Raymond James analyst Simon Leopold directly wrote: “Supply constraints are forcing management to temper revenue outlook upgrades.”

Stocks initially spiked 13% after hours, then erased all gains, opening down over 10% on Thursday—making Arm one of the biggest decliners among tech stocks. This marks the third time in the past year that Arm has delivered a “beat-and-bleed” outcome following a strong earnings report.

After Arm, CoreWeave took the stage. Q1 actual revenue exceeded expectations, with backlog expanding to $99 billion. Nvidia injected another $2 billion in capital during the quarter. However, Q2 revenue guidance came in below consensus, and full-year 2026 capital expenditure was raised to $31–35 billion—more than double the $14.9 billion spent in 2025. Despite this, post-earnings shares dropped over 10%.

CoreWeave’s losses are real, its debt is real, but so are its orders: $99 billion in forward revenue commitments and continued Nvidia backing. Yet clearly, the market questions whether these future revenues can outpace today’s capital expenditures.

Fed Remains Hawkish, Nonfarm Payrolls Looming

Finally, on the Fed front, short-term interest rate markets showed a slight hawkish tilt, with the probability of an unexpected rate hike by year-end rising to around 20%. However, the market largely dismissed this as noise—labor data remains strong, with initial jobless claims modestly rebounding to 200,000, far from any material cracks in the labor market.

The 10-year U.S. Treasury yield rose about 4.8 basis points to 4.393%, moving in sync with the oil price recovery.

Offshore RMB briefly breached 6.80 during the session, hitting a four-year high, before retreating slightly to close at 6.8078 in New York. The DXY rose 0.08% to 98.10.

Gold saw spot gold surge intraday to above $4,700—the highest level in two weeks—closing up 0.22% at $4,701.61 per ounce. Amid inflation fears fueled by oil spikes and safe-haven demand from waning peace prospects, gold found its footing. Silver outperformed, with COMEX silver futures closing up 3.02% at $79.64 per ounce, while spot silver briefly broke above $82 intraday.

In Europe, the STOXX 600 dropped 1.02%, the UK FTSE 100 fell 1.55%, France’s CAC 40 declined 1.17%, and Germany’s DAX slid 0.99%.

The Hormuz variable remains unresolved. The next market trigger lies in Friday’s nonfarm payroll report. Initial jobless claims rose slightly to 200,000, still below the 206,000 consensus—indicating mild hiring pressures. With the Fed’s chance of a rate hike this year now hovering around 20%, this data will likely serve as the next anchor for market repricing.

Source: BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

16 days ago

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

16 days agoAmazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

16 days agoBinance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

16 days agoBinance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

16 days ago

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

16 days agoSlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

16 days ago