Circle’s Second Growth Curve: After $222 Million in Arc Funding, Is CRCL Still the Future or ARC?

Circle’s Second Growth Curve: After $222 Million in Arc Funding, Is CRCL Still the Future or ARC?

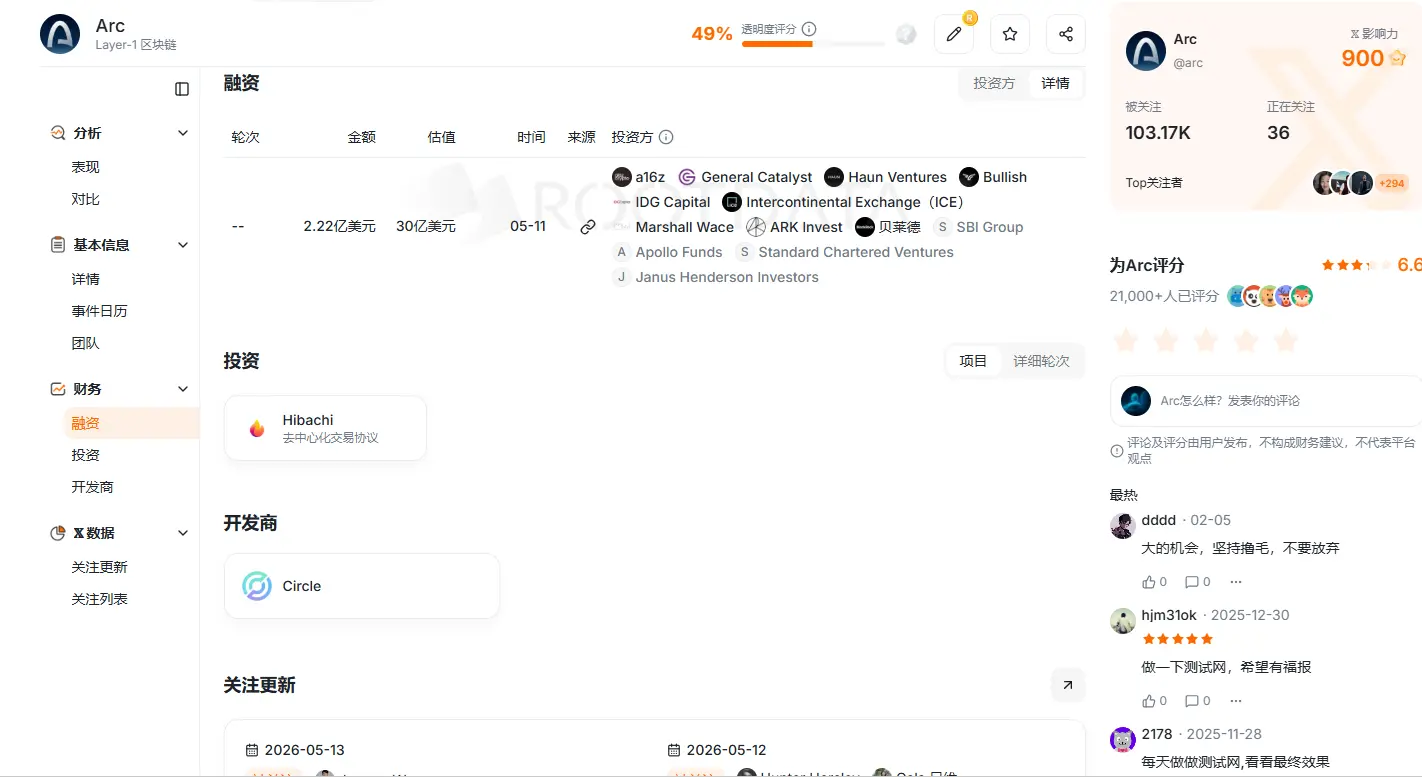

On May 11, Circle announced the completion of a $222 million token sale for Arc, the native token of its public blockchain Arc, with a fully diluted valuation of $3 billion, coinciding with the release of its Q1 2026 financial report.

Leading the round was a16z crypto with a $75 million investment, followed by institutional backers including BlackRock, Apollo, ICE (parent company of NYSE), SBI Group, Standard Chartered Ventures, and ARK Invest.

CRCL stock surged nearly 16% on the day, pushing its market cap above $30 billion.

Image source: RootData

The market now faces a core question: Circle is already a publicly listed company—why issue an ARC token if one can simply hold CRCL shares to bet on its future? Both aim to capture value from the Arc network. What do they each represent?

1. Why Did Circle Build Arc Itself?

Why didn’t Circle continue issuing and using USDC on Ethereum or Solana, instead investing heavily in building its own blockchain?

a16z Crypto explained that as global finance increasingly migrates on-chain, only a select few blockchains will serve as the foundational infrastructure for the “on-chain economic system.”

Last year, stablecoin transaction volume approached $9 trillion—on par with global payment networks like Visa and PayPal. Cross-border payments, B2B settlements, and foreign exchange are becoming core use cases for stablecoins, elevating them to a central layer of global financial infrastructure.

Yet current blockchain infrastructure remains primarily designed for crypto-native users and individual developers, lacking native support for large-scale institutional needs.

Industry insiders note that institutions face several critical pain points when operating on-chain: complete chain-on-chain and off-chain reconciliation for asset issuance and redemption; deterministic finality for payments; compliance capabilities embedded at the protocol level; configurable privacy protection; and predictable gas costs using USDC.

These requirements cannot be natively met by existing chains like Ethereum or Solana.

For Circle, the business has historically relied on interest income from USDC reserves for profitability. In Q1, USDC’s circulating supply reached $77 billion, up 28% year-over-year. As scale grows, relying solely on existing chains fails to fully address deep institutional demands.

Hence, Circle launched Arc—its primary goal being to fill this gap. Owning stablecoin circulation on someone else’s chain does not mean the financial ecosystem belongs to you. This is the fundamental logic behind Circle’s decision to build its own L1.

Image source: X user @vanisaxxm

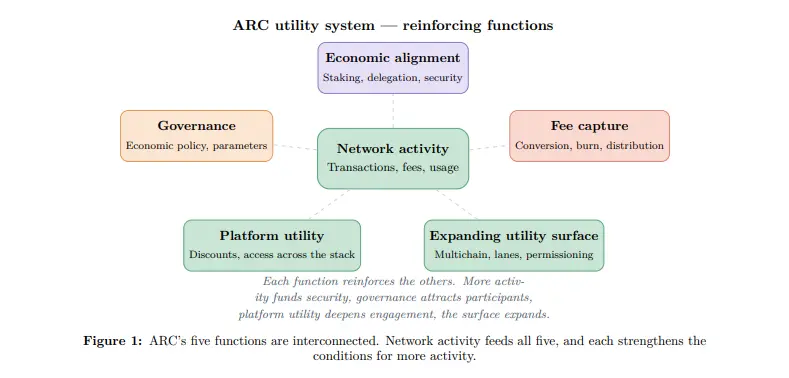

2. USDC Solves Transaction Issues, ARC Solves Coordination Problems

Since USDC already serves as Arc’s gas token, why issue a separate ARC token?

USDC effectively resolves stability at the transaction layer. Institutions can pay fees in USD-denominated terms—costs are predictable and bookable—avoiding the financial headaches caused by volatile crypto asset prices.

But long-term network health requires more than just solving transaction issues—it also demands coordination mechanisms.

According to the official whitepaper, Arc will transition from PoA to PoS over time. Validators must stake assets to secure the network. The core mechanism relies on economic incentives binding validator behavior—malicious actions trigger slashing. However, USDC maintains a fixed $1 peg, making it unable to truly align validator stakes with network success. Only the native token ARC can provide dynamic economic incentives.

Governance also requires alignment of interests. Key decisions such as fee rates, inflation parameters, and burn ratios must be made with a long-term perspective. If voting is done exclusively with USDC, holders may lack sustained motivation—vote once and exit. ARC holders’ asset value is directly tied to network performance, giving them stronger incentives to choose decisions that benefit long-term network health.

The whitepaper explicitly states that ARC governance has phased boundaries. Economic parameters are decided via token holder votes, but critical matters—including protocol upgrades, security incident handling, and validator qualification reviews—are initially retained by Circle, with gradual delegation as the governance framework matures.

In short, USDC is the bloodstream of the Arc network, enabling efficient daily operations; ARC is the equity, permanently aligning all stakeholders’ interests. This dual-token design transforms part of the ecosystem development cost—from Circle’s fixed cash outlays into incentive structures tied to network success.

3. CRCL vs. ARC: Who Eats Which Slice of the Cake?

Now that Circle holds both public company equity (CRCL) and a native network token (ARC), both capturing value from the same Arc network—what exactly are they each eating?

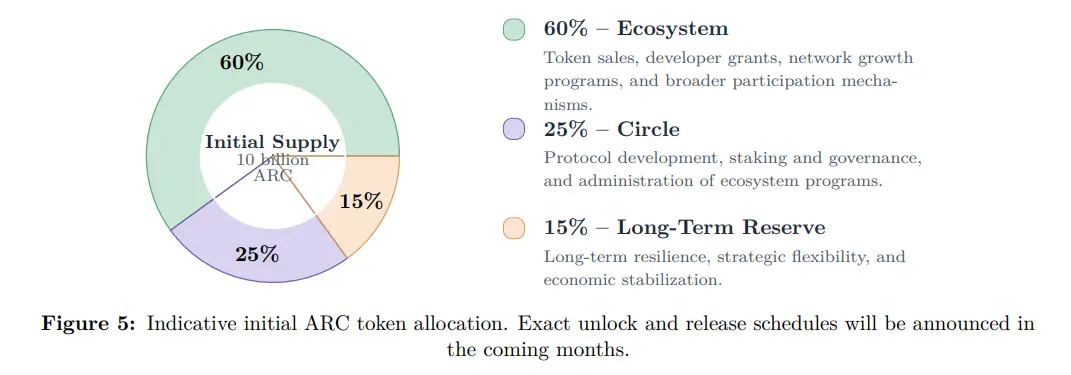

According to the whitepaper, Arc’s total supply is 1 billion ARC tokens, allocated as follows: 60% for the ecosystem (developer rewards, network growth initiatives, and user participation incentives); 25% held by Circle for operating validator nodes, staking, and governance; and 15% reserved for long-term network stability and strategic flexibility.

Regarding fee mechanics, all protocol fees on Arc—regardless of which asset is used for payment—are converted into ARC at the protocol layer. A portion is permanently burned, while another is distributed to stakers and validators. The more active the network, the stronger ARC’s value capture becomes.

CRCL shareholders primarily benefit at the corporate level: Circle continues earning core revenue from USDC reserve interest, along with gains from other business lines like the CPN payment network. Additionally, Circle’s 25% ARC holding allows indirect participation in network-level rewards.

Cryptocurrency analyst BTCdayu proposed a three-dimensional valuation framework for CRCL: First dimension—the reserve interest income, currently the most stable cash flow, forming the valuation floor; second dimension—the payment network revenue, which could approach a Visa-like fee model as CPN scales; third dimension—the network optionality value, reflecting market expectations of Circle’s transformation from a stablecoin issuer into a financial infrastructure platform.

In simple terms, CRCL captures the company’s overall stable cash flows and existing business growth, while ARC captures the network’s growth elasticity—gas fee conversion, ecosystem expansion, and long-term network effects.

The two form a clear dual-track structure. The more successful Arc becomes, the higher the USDC usage and business synergy, benefiting Circle at the corporate level. Simultaneously, rising ARC value increases the worth of Circle’s 25% stake, ultimately flowing back to CRCL shareholders.

However, legally, the two are entirely independent. Officially, ARC does not represent equity in Circle, nor does it confer any claim on Circle’s revenue, profits, assets, or CRCL shares. This means ARC holders have no fiduciary protections akin to public company shareholders—they earn returns based purely on real-world network adoption and tokenomics design.

4. How Can Ordinary Users Participate in the Opportunity?

After understanding how CRCL and ARC distribute value, a practical question arises: who bought the ARC tokens, and how can ordinary users participate at low cost?

The first group consists of institutional strategic investors. They entered through the $222 million pre-sale at $0.30 per token, with lock-up periods ranging from 1 to 4 years. These institutions aren’t just capital providers—they’re also potential users and builders of Arc. For example, BlackRock has tested tokenized asset settlement on the testnet; ICE, parent of NYSE; and SBI Group, one of Japan’s largest financial conglomerates—are all laying groundwork for future operations on Arc.

The second group includes ecosystem builders and long-term holders. Developers and liquidity providers earn ARC rewards through contributions—60% of the ecosystem allocation is dedicated to this purpose. They prioritize long-term network growth, similar to early employees receiving equity.

The third group comprises retail speculators and participants. They focus on early narratives and ecosystem incentives, hoping for price volatility post-mainnet launch.

For users without pre-sale access, Arc offers multiple low-cost entry paths.

Arc Testnet launched in October 2025 and has already processed over 244 million test transactions. The mainnet is expected to go live in summer 2026. Users can claim free test tokens to perform swaps, bridges, and smart contract deployments, gaining hands-on experience.

Arc House is the primary gateway for ordinary users. Participants can accumulate points by registering, staying active, posting content, reading, and answering questions—additional points awarded for accepted answers.

Advanced pathways include content creation, video sharing, event organization, and even hosting offline meetups. Users with teams or products can apply for Circle Developer Grants.

Note: Arc House points are solely for community recognition and carry no monetary value or guaranteed rights. Specific rules are subject to the latest official announcements.

Conclusion

Currently, the institutional on-chain race is fiercely competitive—not dominated by Arc alone.

Digital Asset, parent of Canton Network, is raising funds at around $2 billion valuation, led by a16z crypto; Plasma positions itself as a stablecoin-native settlement layer, offering relatively attractive valuations; and Visa has included Arc, Canton, Plasma, Base, and Tempo in its stablecoin settlement testing pilot in April. This indicates the space remains in a phase of parallel competition among multiple players.

Against this backdrop, Arc’s $3 billion pre-sale FDV sits at a relatively high level. Retail investors participating in secondary markets must thoroughly assess project narrative potential and internal competitive dynamics.

From a long-term view, holding ARC with annual inflation of 2% to 3% requires sufficient real transaction fees to offset issuance pressure—only then can intrinsic value grow. CRCL, backed by USDC reserve interest and payment network revenue, enjoys clearer cash flow support. The two face different risk-return profiles.

In the short term, market sentiment often follows its own logic. The narrative surge around mainnet launch may present temporary opportunities, during which Circle’s 25% ARC stake will appreciate, benefiting CRCL shareholders as well.

Regulatory-wise, the implementation of the GENIUS Act strengthens Circle’s moat. Meanwhile, the updated draft of the CLARITY Act has been released and is under congressional review, potentially bringing greater regulatory clarity to the digital asset ecosystem—a significant positive for Circle.

Overall, Arc represents one of Circle’s most important strategic moves. As the whitepaper states: “A global economic operating system cannot be coordinated by a single entity—it will transform Arc participants into maintainers of Arc.” Whether this vision materializes depends ultimately on whether Arc attracts substantial real institutional trading and economic activity after mainnet launch.

Until actual data lands, all narratives remain just narratives.

Author: Zhou, ChainCatcher

Source: ChainCatcher

Disclaimer: Contains third-party opinions, does not constitute financial advice

Yi Lihua: The rebound is basically over, and we are now in the "darkness before the dawn."

12 mins ago

Bitcoin briefly breaks below $78,000

17 mins agoMinistry of Public Security Criminal Investigation Bureau: Online fraud targets minors, with illicit funds flowing overseas through virtual currencies

34 mins ago"Smart Money" that previously accumulated ETH at an average price of $3.45 has bought 647.137 ETH after one year

53 mins agoCerebras' IPO ignites AI capital markets, with institutions linked to Trump's son emerging as investors

1 hour agoMusk Responds to Discussion on "Post-SpaceX IPO Tax Avoidance Strategy": Will Not Sell Any Shares

1 hour agoSources: U.S. and Israel May Resume Military Operations Against Iran as Early as Next Week

2 hours ago