"Cancel insurance, invest in stocks": South Korea's seniors over 60 are borrowing to bet on Samsung

"Cancel insurance, invest in stocks": South Korea's seniors over 60 are borrowing to bet on Samsung

How manic has the South Korean stock market become recently?

KOSPI has surged from 4,000 points to nearly 8,000 points within half a year. According to *JoongAng Ilbo*, at Seoul’s Gangnam district department store, restrooms are completely packed every day at 3:30 PM—the closing time—because employees hide inside to monitor their trading positions.

As of mid-May, retail investors’ margin borrowing balance with brokers in South Korea reached a record high of KRW 36.47 trillion (approx. CNY 17 billion), doubling over just one year.

Yet, the money flowing into this frenzy comes from an unusual source.

According to *Korea Herald*, total policy surrender volume for South Korea’s three largest life insurers reached KRW 4.9 trillion (approx. CNY 23 billion) in the first quarter—a 16.3% increase year-on-year. Savings-type life insurance policies saw the sharpest drop, rising by 23.2% in cancellations.

Savings-type life insurance is designed to leave financial legacies for families. Surrendering these policies guarantees a loss, as the book value falls below paid premiums. Nevertheless, more and more people are choosing to take the hit and cash out.

Where does the withdrawn money go? Most likely, it flows into another stock brokerage account.

Data obtained by a South Korean National Assembly member from the Financial Services Commission reveals that as of the end of Q1, retail investors borrowed KRW 27 trillion from the top ten brokers for stock trading, with over 62.3% of the funds taken by those aged 50 and above.

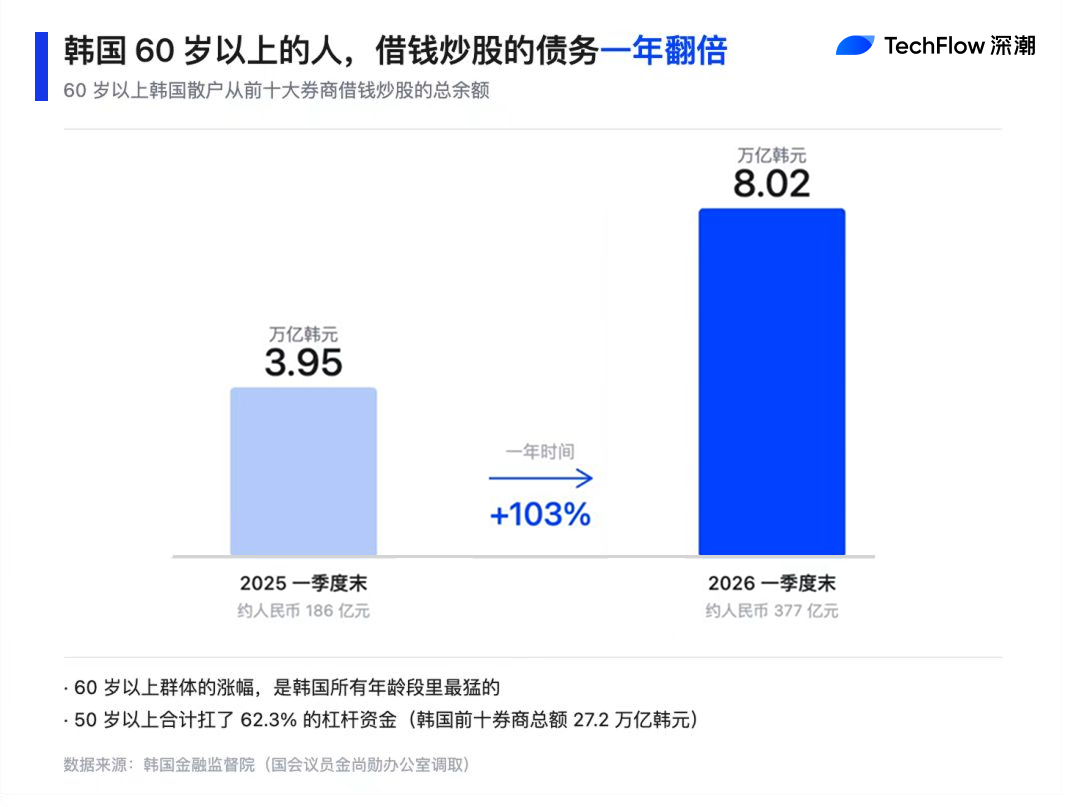

For individuals aged 60 and above, debt levels rose from KRW 3.95 trillion to KRW 8.02 trillion within a year—the steepest increase across all age groups.

Retirees are betting their future savings on today’s bottom-up rally.

Is It Madness Because of Bull Markets?

Adding leverage during bull markets is called “amplifying returns”; doing so during bear markets is known as “accelerating zero.” South Korea’s elderly have already experienced a rollercoaster ride once before.

Early in March, joint U.S.-Israel airstrikes on Iran triggered global market panic. South Korea’s stock market suffered two consecutive daily circuit breakers, with KOSPI plunging nearly 13%.

A report released by the Financial Services Commission at the end of March revealed that during this downturn, among the nation’s 4.6 million retail investor accounts, those using margin loans lost an average of 19%, while non-leveraged investors lost only 8.2%. Margin traders lost 2.3 times more than those without leverage.

Breaking down by age group, the 60+ cohort using leverage suffered the worst losses, averaging −19.8%, the lowest return across all demographics.

Even worse followed: forced liquidation.

Leverage accounts have a maintenance margin threshold. When the market value of holdings drops below this level, brokers sell automatically—no negotiation involved. The Financial Services Commission received numerous complaints from retail investors at the time, such as “My stocks were sold without my knowledge” and “I was charged exorbitant interest fees.”

A significant portion of these complaints came from elderly investors unfamiliar with trading rules. Yet, paradoxically, those who bought in during March’s circuit breakers ultimately profited.

South Korea’s stock market recovered the entire loss within two months and has been rising ever since. Investors who endured the crash in March have fully recouped their losses—some even made profits.

Volatility paired with upside potential makes this a successful “boarding experience,” even when done via borrowed capital.

Such success becomes justification for bolder moves next time. After March’s circuit breakers, retail margin borrowing didn’t contract—it continued rising. Public data shows that total margin loan accounts peaked at KRW 25 trillion by late April, setting a new record; by mid-May, they surged further to KRW 36.47 trillion.

In just one and a half months, South Korea’s retail investors borrowed an additional KRW 11 trillion (approx. CNY 52 billion).

On an individual level, early in May, a South Korean civil servant posted a screenshot on Blind, a popular Korean workplace community:

His account held KRW 2.3 billion (approx. USD 1.7 million) invested entirely in SK Hynix, with KRW 1.7 billion borrowed from his broker. That means he used KRW 600 million of personal capital to lever up KRW 1.7 billion.

Four days later, he updated: he had already made KRW 267 million in profit.

On the same day, another 20-something employee working for Seoul Metro posted online: rather than miss this wave, she’d rather “go completely bankrupt” and go all-in, using 150% margin financing to buy SK Hynix shares. The borrowed funds were then reused as collateral to borrow again.

Posts like these appear daily on Blind’s Korean community.

Regulators aren’t blind to this FOMO-driven frenzy. In late March, the Financial Services Commission convened major brokers to tighten risk controls. Some brokers temporarily restricted new margin loans on overheated stocks. But the money already lent remains, accruing interest at annual rates between 7% and 9%.

At an 8% rate, South Korea’s retail investors collectively pay brokers nearly KRW 3 trillion (approx. CNY 14 billion) in interest annually.

But borrowing at 60 versus 30 years old is fundamentally different. A 30-year-old who blows up can rebuild over decades. A 60-year-old’s blowup could wipe out their entire pension—leaving only exhausted bodies and the reality of no more earning capacity.

If another circuit breaker hits, there may not be a “two-month recovery” story this time around.

Old People’s Intelligence Network in Tago Park

Like all South Korean retail investors, elderly Koreans are borrowing to bet on Samsung Electronics and SK Hynix.

Since the beginning of the year, Samsung Electronics has risen 138%, SK Hynix 189%. KOSPI overall gained 80%, but excluding these two stocks, gains were only 30%.

Together, these two companies account for over 43% of KOSPI’s weight. As long as they rise, the entire South Korean market rises.

The majority of borrowed funds flow into these two stocks. Of all net inflows by South Korean retail investors this year, one-quarter went to these two firms. The remaining three-quarters were scattered across other equities—but those stocks have seen only 30% gains overall this year.

Tago Park in Jongno District, Seoul, is one of the city’s oldest public parks. Young people rarely visit. Its regulars are retired elders, gathering each morning for free coffee, casual conversation, chess games—time moving so slowly it feels suspended.

According to *Kyung Hyang News*, the park’s topic has changed this year.

During coffee breaks, someone might say, “My Samsung shares went up again.” Chess players ask, “Did you buy Hynix?” An 77-year-old man told his middle school classmate that recent gains in Samsung and Hynix had brought him some profit in his account.

A corner of Tago Park filled with elderly chess players

Source: Seoul News

But he didn’t mention whether he borrowed money—or how much.

Discussions popularized in senior parks don’t emerge from thin air—they resemble village bulletin board exchanges. For instance, one elder hears another made money, goes home to check his own account the next day, starts borrowing a little, then possibly ends up borrowing more and more.

But if you ask why South Korea’s elderly are now in leveraged stock accounts, it ties back to their retirement security.

According to OECD data, South Korea’s relative poverty rate for those aged 65+ stands at about 40%—the highest among OECD nations. The national pension system’s replacement rate has remained low for years, averaging around 50% across OECD countries, while South Korea’s hovers near only 31%.

Meanwhile, South Korea’s labor participation rate for those aged 65+ is the highest among OECD countries—meaning a significant portion of retirees must continue working after retirement.

Thus, free coffee at Tago Park is essentially a form of social welfare. At under KRW 500 per cup, it's a staple in the daily lives of retirees receiving less than USD 1,000 monthly in pensions.

But today, these seniors aren’t just here for free coffee and chess. Their phones may also be open to real-time KOSPI price feeds.

Since President Yoon Suk-yeol took office, he has pushed for nationwide stock market participation. In public appearances, he calls himself the “Great Ant”—a colloquial term for retail investors in Korea. He even included “KOSPI surpassing 5,000 points” as a key policy target.

In other words, borrowing money to invest in stocks—especially among the elderly—is, to some extent, officially encouraged in South Korea.

What these seniors are truly betting on is anxiety. If they don’t get on board now, they’ll miss the train.

This is their final chance before retirement. The semiconductor industry in South Korea is cyclical—over the past three decades, it has undergone multiple dramatic swings from boom to bust.

SK Hynix lost KRW 4.26 trillion in 2023—the worst performance in a decade. Yet, within two years, it transformed into a quarterly operating profit margin of 72% (surpassing NVIDIA). This rapid cycle shift itself serves as a warning: the cycle could reverse again.

And for elderly investors leveraging their futures, time may be their most precious resource.

The seniors in Tago Park are desperately trying to capture version-specific alpha. Coffee remains free. The market feed on their phones never stops.

Author: Ku Li, DeepFlow TechFlow

Disclaimer: Contains third-party opinions, does not constitute financial advice

Iranian state media denies the existence of a memorandum of understanding between Iran and the U.S.

10 mins ago

Binance Alpha Citrea (CTR) Airdrop Threshold: 211 Points

14 mins agoChina accounts for over 80% of the global humanoid robotics market

26 mins agoGlassnode: Approximately 7.75 million BTC are currently in a loss position

43 mins ago

Bytedance has issued equity incentives for a specific business unit for the first time, opening up "DouBao Shares" subscription rights to Seed employees this month

43 mins agoData: NEAR Intents has generated over $33 million in fees since launch

49 mins ago

Data: 21Shares and Bitwise ETF collectively purchased $68 million worth of HYPE last week

51 mins ago