Musk's "One-Man Dynasty," Ringing the Bell on June 12

Musk's "One-Man Dynasty," Ringing the Bell on June 12

On May 20, U.S. local time, SpaceX formally submitted its S-1 filing to the U.S. Securities and Exchange Commission (SEC), initiating the Nasdaq IPO process with the ticker symbol "SPCX." The company plans to raise between $70 billion and $80 billion through this IPO, targeting a valuation of $1.75 trillion to $2 trillion. The listing is expected to take place on Nasdaq on June 12.

This marks the largest IPO in human history and Elon Musk’s first public market debut under absolute control. Post-IPO, Musk will retain 85.1% of voting power, leaving public shareholders with negligible influence.

Earlier on April 1, SpaceX had already confidentially filed its draft S-1 registration statement with the SEC under the internal codename "Project Apex"—the first formal legal step in the IPO process.

According to the prospectus, investment bank Goldman Sachs leads as the lead underwriter, with Morgan Stanley, Bank of America, and 16 other underwriters serving as joint bookrunners in this issuance.

The submission of the prospectus also marks the first time SpaceX has disclosed its financial fundamentals—Starlink is the cash cow, while xAI is a cash-burning black hole. Musk has effectively rebranded a spaceflight company into a supercharged narrative of “AI + Space.” So what exactly supports a $2 trillion valuation?

01 Starlink Generates $11.4 Billion Annually; AI Division Loses $6.4 Billion in One Quarter

SpaceX’s financial data reveals a stark dichotomy: ice and fire.

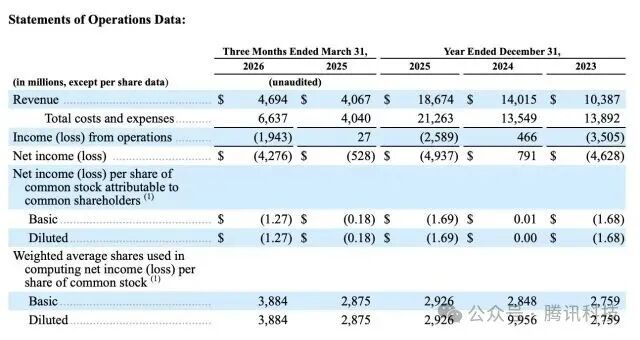

SpaceX Key Financial Metrics

In 2025, SpaceX achieved consolidated revenue of $18.67 billion, adjusted EBITDA of $6.584 billion, but incurred an operating loss of $2.589 billion and a net loss approaching $4.94 billion. The losses were almost entirely driven by the AI business—xAI lost $6.4 billion in 2025, while Starlink contributed $4.4 billion in operating profit during the same period. Profits from the sky were completely consumed by ground-based large model expenditures.

In Q1 2026, the company reported revenue of $4.694 billion, adjusted EBITDA of $1.127 billion, and an operating loss of $1.943 billion.

By segment, connectivity services—primarily Starlink—generated $3.26 billion, accounting for nearly 70% of total revenue and serving as the dominant driver. AI operations (xAI) brought in $818 million, while space operations (including rocket launches and government contracts) generated $619 million.

Core Business Financials of SpaceX

From the balance sheet perspective, as of March 31, 2026, SpaceX held $15.9 billion in cash and cash equivalents, $7.8 billion in marketable securities, total assets of $102.1 billion, and total liabilities of $60.5 billion, including debt and lease obligations of approximately $30.3 billion.

Despite holding over $15 billion in cash, the company faces immense cash flow pressure due to annual capital expenditures exceeding $20 billion.

Starlink's operational metrics are equally impressive.

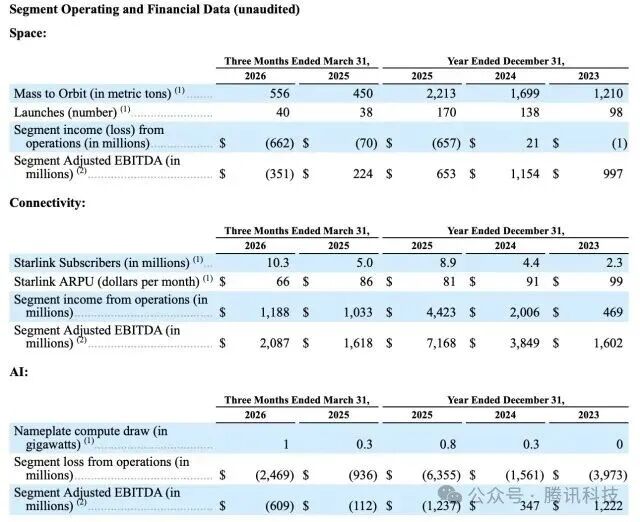

SpaceX Space Operations Highlights

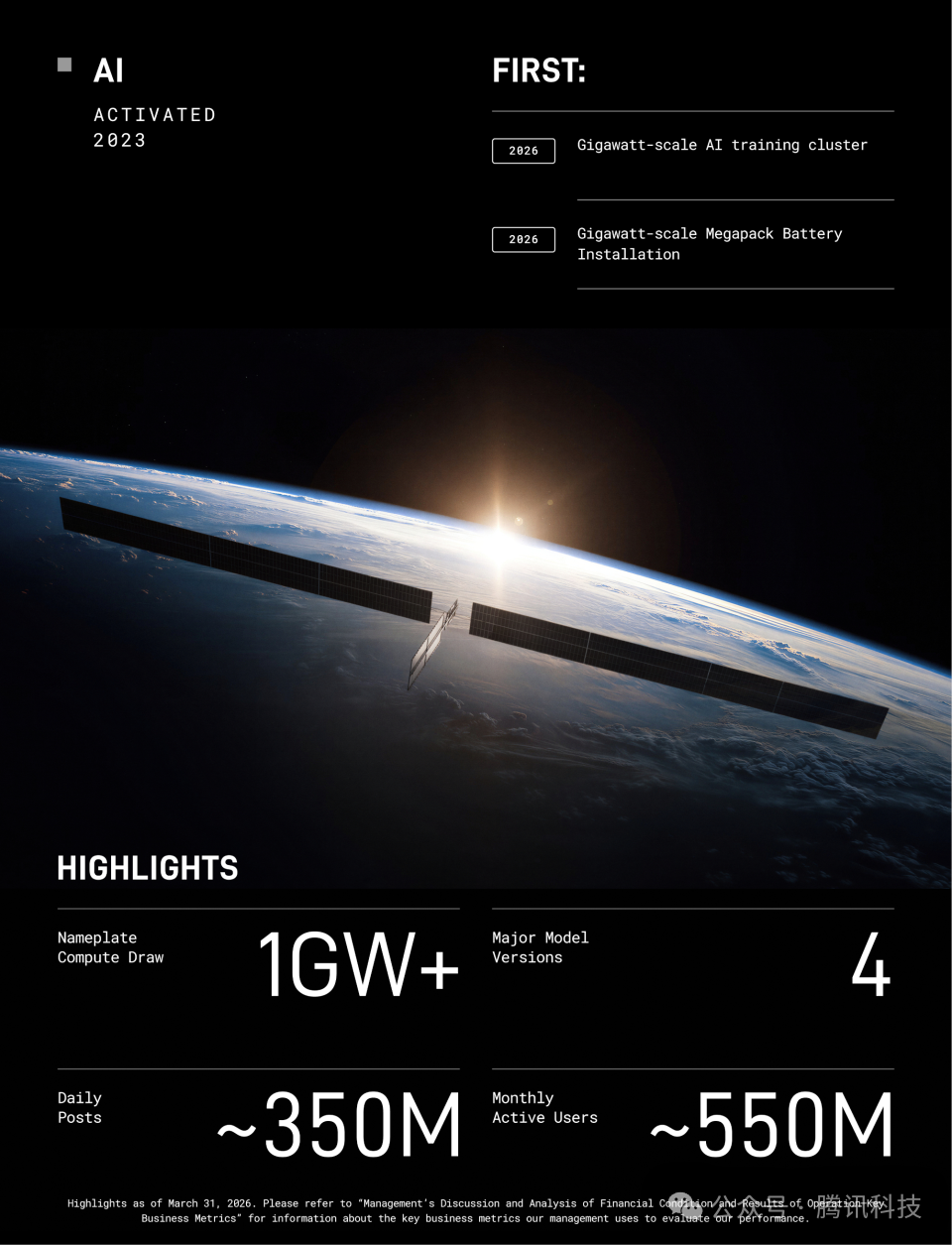

The prospectus reveals that as of March 31, 2026, Starlink had reached 10.3 million users—up from 8.9 million at the end of 2025, representing a net increase of 1.4 million users in one quarter. Approximately 9,600 satellites are currently operational. Starlink’s adjusted EBITDA reached $7.2 billion, with an EBITDA margin of 63%, up 22 percentage points from 41% in 2023, and free cash flow of around $3 billion—the only business segment generating positive cash flow within SpaceX.

However, average revenue per user (ARPU) for individual Starlink customers declined from $99 in 2023 to $81 in 2025, and further to $66 in Q1 2026—a reduction of over 30% in just two and a half years.

This reflects a classic trade-off: SpaceX has actively lowered prices to rapidly expand user base, but as scale grows, individual user monetization capacity declines. If ARPU continues to fall, achieving long-term revenue targets requires user growth to consistently outpace price erosion.

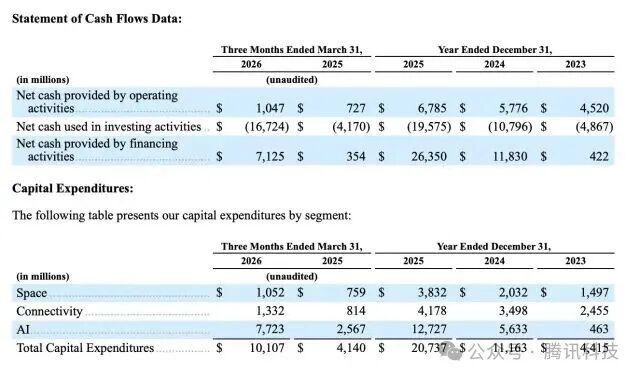

SpaceX’s total capital expenditure in 2025 amounted to $20.7 billion—exceeding its entire annual revenue—and the AI division alone accounted for $12.7 billion in spending, surpassing the combined costs of aerospace and satellite operations.

Capital Expenditure and Cash Flow of SpaceX

xAI burns through approximately $1 billion per month, totaling around $14 billion annually. For comparison, OpenAI and Anthropic burned roughly $9 billion and $4 billion respectively in 2025—SpaceX’s AI segment alone exceeds their combined burn. While spending aggressively, xAI lags significantly behind both competitors in terms of revenue scale and growth rate.

Even more concerning is the valuation multiple.

SpaceX’s target IPO valuation ranges from $1.75 trillion to $2 trillion—about 266 times its adjusted EBITDA. In contrast, Meta trades at 16x, Alphabet at 25x, NVIDIA at 36x, and even Tesla, known for high valuations, stands at only 119x.

With a valuation multiple more than double that of Tesla, SpaceX’s entry into the public markets poses the first major test: is this value discovery or speculative bubble?

The prospectus explicitly states: “The company does not intend to pay dividends to Class A shareholders in the foreseeable future.” This means investors can only bet on stock price appreciation—a pure growth stock with no safety net.

02 85% Voting Power: Musk’s “One-Man Dynasty”

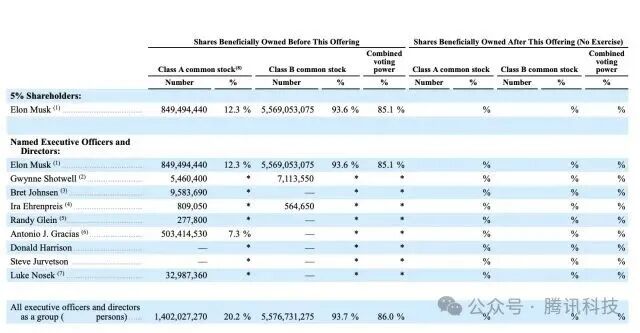

SpaceX employs a dual-class share structure. The company issues Class A common shares (one vote per share) to public investors, while Class B common shares (ten votes per share) are held by Musk and insiders.

Management and Director Shareholding Structure

According to the prospectus, Musk holds approximately 42.5% of SpaceX’s equity but controls about 84% to 85.1% of total voting rights via his Class B super-voting shares. This means post-IPO, regardless of how many shares public investors purchase, Musk alone determines board composition, major M&A decisions, and even amendments to the corporate charter.

The prospectus also discloses that Musk will continue serving as CEO, CTO, and Chairman of the Board, with unilateral authority to remove or appoint Class B board seats. SpaceX will apply for “controlled company” exemption, avoiding the requirement for a majority of independent directors.

Aside from Musk, the prospectus shows no other shareholder owns more than 5%. However, the shareholder list includes notable institutions: Alphabet (Google’s parent) as an early strategic investor, now holding ~5%; Fidelity Investments (~2%); Silicon Valley venture capital firms Valor Equity Partners, Founders Fund, Sequoia Capital collectively owning ~10%; plus hedge funds D1 Capital, Darsana, and Middle Eastern sovereign wealth funds. SpaceX has also established a large stock option pool for employees to incentivize core technical teams.

In Silicon Valley, dual-class structures are common. According to Fenwick’s 2025 Corporate Governance Survey, 27.3% of the top 150 tech companies in Silicon Valley still use dual-class shares—a proportion far exceeding the 10.1% among S&P 100 constituents. Yet designs vary across firms.

But SpaceX takes this control mechanism to an unprecedented degree—85% of voting power concentrated in one individual—making it exceptionally distinct among tech giants.

Looking back at Musk’s other publicly traded company, Tesla, the situation is starkly different. Tesla follows a “one share, one vote” principle without super-voting rights, forcing Musk to frequently confront activist shareholders.

03 xAI Merger: The “Narrative Engine” Behind the $2.5 Trillion Valuation

The “COLOSSUS II” Facility in Memphis, Tennessee

In February, SpaceX completed its acquisition of xAI at an overall valuation of $1.25 trillion, with xAI valued at $250 billion. Prior to the merger, SpaceX’s standalone valuation was approximately $1 trillion—an AI story adding roughly $250 billion in premium.

This transaction delivered two immediate outcomes: first, revenue uplift—AI operations contributed $818 million in Q1 2026. Second, narrative upgrade—SpaceX transformed from a spaceflight company into a hybrid entity of “AI + Space.”

Wall Street’s valuation expectations for SpaceX have since risen from $1.25 trillion to $1.75 trillion to $2 trillion.

The prospectus also reveals bolder long-term ambitions. SpaceX plans to deploy the first orbital AI computing pods before the decade ends, operating AI compute infrastructure in space.

xAI Business Highlights

Musk believes producing AI compute in space is cheaper than on Earth.

Meanwhile, SpaceX also mentions “space mining”—extracting metal resources from near-Earth asteroids. These initiatives currently generate no revenue and lack even prototype technology, yet they form some of the most compelling pages in the prospectus—and the biggest source of valuation divergence.

04 Terafab, Cursor Acquisitions, and Financial Services: Musk’s “Ecological Backflip”

The prospectus hides several overlooked strategic moves.

Notably, SpaceX and Tesla jointly announced the Terafab project, aiming to integrate all stages of semiconductor production into a single system, manufacturing two types of chips: one optimized for Tesla’s Full Self-Driving system, Optimus humanoid robots, and Robotaxi fleets—edge inference processors—and another, high-power, radiation-hardened chips for space applications.

According to public disclosures, the project’s total investment could reach up to $119 billion, using Intel’s 14A process technology, with the goal of directing 80% of compute capacity toward orbital AI data centers.

Additionally, SpaceX plans to acquire Cursor post-IPO, using Class A common shares as consideration, with an implied equity value of $60 billion. SpaceX has secured exclusive rights to acquire Cursor at a $60 billion valuation, with the deal executable 30 days after IPO completion and a reverse breakup fee as high as $10 billion. Core engineering talent from Cursor previously joined xAI.

The company also plans to launch a financial product encompassing payments, banking, and other services, expanding into the financial services sector.

These ventures share a common trait: all are in early stages, require massive capital expenditure, and depend heavily on SpaceX’s fundraising capacity and Musk’s storytelling prowess.

05 Market Divide: Wall Street’s Dream Team vs. Skepticism

The underwriting lineup saw an unexpected reversal—one that reflects Wall Street’s deep divisions.

Morgan Stanley, long a close partner of Musk, was bumped from the top spot by Goldman Sachs—a move surprising to some market observers, especially given Morgan Stanley’s prior leadership in Tesla’s IPO and Twitter acquisition financing.

Florida State University scholar and “IPO Man” Jay Ritter stated clearly: if SpaceX reaches a $2 trillion valuation, he would short the stock upon listing. Ritter further noted that new offerings with revenue exceeding $100 million (in inflation-adjusted terms) and P/S ratios above 40x typically underperform the broader market by a significant margin over three years post-IPO.

Larger concerns stem from the AI unit’s losses: xAI lost $6.4 billion in 2025, while Starlink’s $4.4 billion profit fails to cover the gap. If AI continues burning cash without commercialization meeting expectations, SpaceX’s overall profitability pressure will surge dramatically.

BNP Paribas analyst James Picariello bluntly warned that SpaceX’s IPO will “fragment” the retail investor base supporting Musk, potentially pressuring Tesla’s stock price.

UBS analyst Joseph Spak earlier cautioned clients that massive investments in hardware AI may be just the beginning. Meanwhile, Musk simultaneously leads Tesla, SpaceX, xAI, X, and other entities—raising questions among institutional investors about whether his management bandwidth is stretched too thin.

06 Conclusion

June 12 will be a nationwide referendum testing the “Musk Premium.”

Starlink provides a solid cash cow. xAI delivers a sexy narrative. Musk offers absolute control. The upside is extreme decision-making efficiency; the downside is no brakes.

Goldman Sachs calls this IPO a once-in-a-generation opportunity—but some analysts liken it to buying a lottery ticket: the grand prize is Mars, the consolation is Earth.

Cook handed Apple to Tim Cook, a hardware engineer-turned-successor. Musk, however, has no intention of handing SpaceX to anyone—going public adds a group of non-voting passengers, but the cockpit remains occupied by him alone.

Well, it’s very Musk.

Written by Su Yang; Edited by Xu Qingyang

Original Source: DeepTide TechFlow

Disclaimer: Contains third-party opinions, does not constitute financial advice

Iranian state media denies the existence of a memorandum of understanding between Iran and the U.S.

10 mins ago

Binance Alpha Citrea (CTR) Airdrop Threshold: 211 Points

14 mins agoChina accounts for over 80% of the global humanoid robotics market

26 mins agoGlassnode: Approximately 7.75 million BTC are currently in a loss position

43 mins ago

Bytedance has issued equity incentives for a specific business unit for the first time, opening up "DouBao Shares" subscription rights to Seed employees this month

43 mins agoData: NEAR Intents has generated over $33 million in fees since launch

49 mins ago

Data: 21Shares and Bitwise ETF collectively purchased $68 million worth of HYPE last week

51 mins ago