Why Have Forex Stablecoins Never Taken Off?

Why Have Forex Stablecoins Never Taken Off?

Stablecoin digital banking represents the next major frontier for retail adoption, with foreign exchange (FX) emerging as its core component.

Tether and Circle have spent over a decade building liquidity, distribution channels, and network effects around USDT and USDC—making it extremely difficult for new FX stablecoin issuers to replicate.

Rather than competing via spot FX stablecoins, a better path lies in synthetic FX: users continue holding USDT/USDC at the underlying layer, while their account balances are denominated in their preferred local currency.

Stablecoin digital banks are transcending crypto-native communities, disrupting how global consumers and enterprises transact. In the past year, approximately $6 billion in risk capital has flowed into this frontier.

Yet, current on-chain FX infrastructure effectively reduces stablecoin digital banks to mere dollar-denominated banks. This limitation creates massive opportunity, as 95% to 99% of global accounts are not denominated in USD.

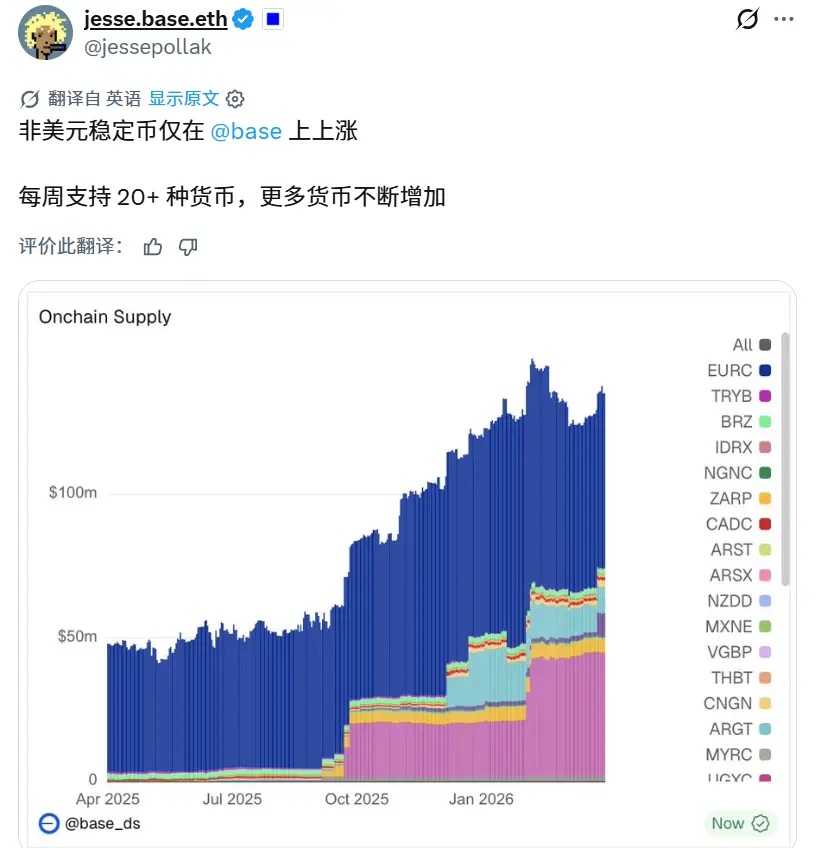

Less than One Year, 24x Growth

A smart friend from Tether once told me that diversifying the holder base is one of the company’s top three North Star metrics. A whale-dominated holder structure introduces unnecessary volatility to USDT’s total value locked (TVL).

All stablecoin issuers aim to win over retail and enterprise users who use stablecoins for daily transactions and banking—not more traders and whales.

In short, 1 billion people each holding 10 USDT is far superior to one whale holding 10 billion.

Stablecoin digital banking offers an ideal opportunity for stablecoins to reach everyday retail and enterprise users. Beyond trading, mass-market users will experience the convenience and superiority of stablecoins as payment, savings, and investment vehicles—surpassing today’s dominant trading use cases.

A snapshot of the rapid rise of stablecoin digital banking: crypto card spending surged 525% in 2025, jumping from $14.6 million to $91.3 million, led by EtherFi at $55.4 million.

Yesterday, @ether_fi card daily spend just broke $3.7 million. That equates to an annualized stablecoin spend of $1.35 billion—24 times higher than last year.

When something grows 24x in less than a year, you must pay attention. Meanwhile, @ether_fi launched their Euro product last week—I’ll dive deeper into that shortly.

Stablecoin digital banking is a new battleground with no clear leader yet. Since 2018, stablecoins with fiat redemption liquidity and broad acceptance across centralized exchanges have been considered the best, capturing the largest growth potential.

How do you win this new battle? What kind of stablecoin is truly suited for digital banking?

Why Stablecoin FX Matters

Historically, single-currency digital banks have uniformly failed to gain market traction. Major fintech giants like @Wise, @Revolut, and @airwallex began as FX companies. When PayPal went public in 2002, FX accounted for over 40% of its revenue.

International fund transfers are significantly harder than domestic ones, giving these successful digital banks opportunities to shine in FX and establish dominance in specific payment corridors or consumer/enterprise segments.

Thus, if stablecoin digital banks only offer USD accounts, they face significant hurdles in growth and differentiation—and even more so when competing with established fiat digital banks. Globally, 95% to 99% of accounts are denominated in non-USD currencies.

Currently, stablecoin digital banks cannot serve any of these enterprises or consumers.

600M vs 400B

Despite numerous excellent teams and blockchain ecosystems (especially @base and @CodexFX) eyeing the FX opportunity, the harsh reality remains: total value of all FX stablecoins combined is a minuscule fraction of USD stablecoin scale—around $600 million versus $400 billion, a staggering 700x gap.

If @tether’s success taught us anything, it’s that stablecoins are a business with extreme network effects. @Tether is the highest-quality stablecoin because of the vast ecosystem built around it.

Given the limited TVL of FX stablecoins, unfortunately, most face the following challenges:

Limited liquidity leads to fragile pegging (e.g., the PAXG depeg event on October 10 could happen to any FX stablecoin with limited liquidity and TVL—PAXG has $12B TVL, nearly three times larger than EURC, the largest FX stablecoin)

Not accepted by fintech platforms or centralized exchanges

Even if accepted, fiat redemption channels have very limited liquidity

Limited liquidity against key trading pairs, including USDT/USDC

Almost no yield opportunities

Extremely complex compliance and licensing issues across regions

Most importantly, due to untested peg mechanisms, stablecoin digital banks and broader fintech sectors are hesitant to adopt them until they reach meaningful scale—a classic chicken-and-egg problem likely requiring significant time and resources to resolve.

What Makes a High-Quality Stablecoin?

An exceptional digital bank stablecoin must excel across all of the following dimensions:

Liquidity in fiat redemption channels

Strong peg stability independent of overall market liquidity

Yield opportunities

Liquidity against major trading pairs

Wide acceptance across CeFi, TradFi, and payments

Strong influence on low-Gas chains

Brand and token name recognition

The Traditional Finance Answer

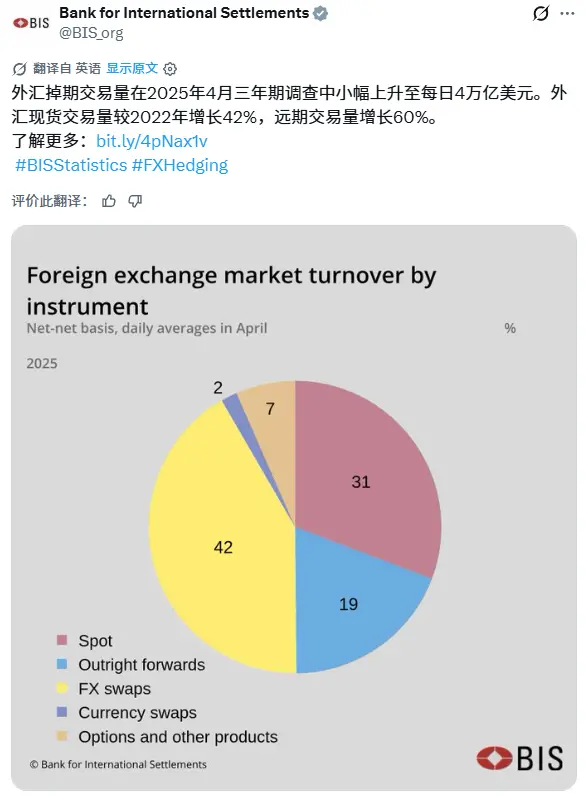

According to BIS data, only about 31% of global FX turnover comes from spot trading, while roughly 69% originates from derivatives markets. This indicates modern FX markets are primarily driven by synthetic exposure, hedging, and financing activities—not physical currency conversion.

Thus, the notional amount settled daily through FX swaps reaches up to $4 trillion.

One of the most important non-spot FX instruments is the Non-Deliverable Forward (NDF): a cash-settled FX forward contract where no physical currency delivery occurs. The counterparties do not exchange the underlying currency but instead settle the profit or loss difference, typically in USD.

NDFs are especially common in cases involving restricted currency convertibility, fragmented offshore access, or insufficient offshore liquidity to enable efficient physical delivery—making synthetic exposure settled in USD operationally easier than directly acquiring and settling local currency.

Example:

A company wants exposure to Swiss Francs (CHF) over the next three months.

Instead of acquiring and settling physical francs, it enters a CHF NDF—effectively holding USD while its account is denominated in CHF.

At maturity, only the profit or loss difference relative to the agreed rate is exchanged, denominated in USD.

Many modern NDF structures are mark-to-market (MtM), meaning unrealized profits and losses are periodically collateralized or settled throughout the contract lifecycle, reducing counterparty risk and improving capital efficiency.

Mark-to-market NDFs effectively allow accounts to remain underpinned by USD, while economically valuing balances and profits/losses in another currency.

On-Chain FX Optimal Solution: Go NDF, Not Spot

For currencies lacking deep or efficient spot liquidity, mark-to-market NDFs offer a powerful solution—widely used in traditional finance for pairs like USD/CHF, USD/KRW, USD/INR, USD/BRL, and USD/TWD.

Corporations, banks, and offshore investors commonly use them to gain synthetic FX exposure without physically delivering local currency.

The crypto space faces similar structural constraints:

Not all currency pairs have deep spot liquidity

Maintaining fully collateralized local fiat stablecoins is operationally challenging

Therefore, mark-to-market NDF structures are ideally suited for crypto-native FX systems.

Users can:

Keep their funds entirely in USDT/USDC

Simultaneously synthetically short USD and long foreign currency via mark-to-market NDF structures

Effectively convert account value and P&L into target currency denomination without leaving the USD settlement network

Advantages include:

Strong peg based on oracles: exposure tracks reliable FX reference rates, not fragmented local spot liquidity

Retain USD stablecoin network and yield: users continue holding USDT/USDC, enabling access to deepest on-chain liquidity and yield opportunities

Superior liquidity and channels: USDT/USDC possess the strongest global fiat redemption channels, exchange integrations, and trading liquidity across the entire crypto market

Scalability across currencies: any currency with a reliable USD oracle can be synthetically supported—no need to build local banking infrastructure, local custody, or sovereign bond reserves like traditional fiat stablecoin issuers

Fund efficiency: only periodic settlement or collateralization of FX P&L differences required, not full spot conversion

This perfectly mirrors how institutional FX markets operate off-chain: overlaying synthetic exposure and cash-settled risk transfer on top of dominant USD financing and collateral systems.

Who Uses On-Chain NDF FX?

Simple narratives or the idea that “FX is obviously next” won’t work. Details matter. Building an FX stablecoin with TVL reaching tens to hundreds of billions (hundreds of millions to trillions) is no small feat.

Teams pursuing this direction cannot expect holders to flood in immediately upon launch. At @SupernovaLabs_, we are crystal clear on three fundamental questions:

Who are your holders?

Why do they hold?

How do you distribute to them?

1. Digital Banks, Custodians, Wallets: Multi-Currency Accounts Are Essential

Total deposits are one of the most critical metrics for digital banks and the blockchains hosting stablecoins. Without native FX infrastructure, multinational corporations cannot safely hold operating funds on-chain—they’re forced to move capital back to local banking systems.

Thus, many stablecoin digital banks and blockchains risk becoming mere capital transit pipelines rather than true financial operating systems.

Mark-to-market NDF infrastructure changes this dynamic.

Stablecoin digital banks, custodians, wallets, and payment platforms can integrate @SupernovaLabs_' API to deliver synthetic FX-denominated services directly on top of the USD stablecoin network. For end-users, the experience becomes a simple toggle:

Switch account denomination from USD to EUR, CHF, SGD, HKD, etc.

Or hold multiple currency-denominated balances within a single account

With the underlying settlement, collateral, and liquidity infrastructure still rooted in USDT/USDC

Stablecoin digital banks, custodians, and wallets share highly aligned incentives with mark-to-market NDFs:

Unlock international user acquisition channels

Increase deposits and retention of balances

Reduce outflows to traditional banking systems

Enable multi-currency accounts for competitive differentiation

Thus, multinational enterprises or individual users can:

Keep funds fully on-chain

Retain access to deep USD stablecoin liquidity and yield

And economically hold foreign currency exposure via synthetic FX markets

This product benefits from macro tailwinds: over the past year, USD has depreciated 10–12% against EUR, increasing demand for non-USD denominated accounts—while users continue keeping funds within the USD stablecoin channel.

2. FX Carry Yield: Scale and Stability Far Exceed Ethena

FX derivatives are widely used for carry trades—one of the largest macro strategies globally. The classic example is the Japanese yen carry trade:

Borrow low-yielding JPY

Go long high-yielding currencies like Brazilian Real (BRL)

Earn the interest rate differential—the “carry”

Brazilian Real rates often sit above 10%, making it one of the most favored carry currencies among hedge funds and macro investors. These trades are typically executed via NDFs, forwards, and FX swaps—not spot conversion.

Compared to crypto basis trading products like @ethena:

FX carry is linked to sovereign interest rate differentials, not crypto market funding rates

Market size is substantially larger, with higher institutionalization

Due to the immense scale of global FX derivatives markets, its capacity is far deeper

Yields are generally lower than peak crypto basis trading returns but historically more stable and scalable

This creates a prime opportunity for on-chain FX carry vaults:

Users deposit USDT/USDC as collateral

Use mark-to-market NDFs to synthetically gain foreign currency exposure

Earn sovereign FX carry yields on-chain—without leaving the USD stablecoin channel

3. Enterprise Global Payments: Stripe Has Validated the Path

Over the past year, @Stablecoin has enabled corporate clients to receive fiat in EUR, MXN, BRL, COP, GBP—and automatically convert funds into USDC.

However, currently, FX is only received on-chain, not held on-chain. For enterprises managing or accounting in currencies like Swiss Francs or Singapore Dollars, this means they must still withdraw funds to local banking networks.

This limitation is especially acute when serving global enterprises—a domain @tempo is actively driving adoption and expansion in.

Stripe provides NDF-style FX hedging support for its fiat global payments. If a merchant wants to settle in Currency A while customers pay in Currency B, the merchant can hedge FX exposure within a specified window and offer customers a stable, locked-in price in their local currency.

Stripe’s NDF FX API for fiat payments

Stablecoin payments can apply a similar model on-chain: users continue holding and using USD stablecoins for transactions, while merchants or wallets can synthetically hedge to their preferred local currency denomination—without relying on spot FX liquidity or local stablecoin issuance.

I want to emphasize just how remarkable Stripe’s FX product profitability is. Despite serving largely non-speculative, highly predictable enterprise and retail payment flows, the product charges ~20 basis points per transaction.

Annualized, this amounts to roughly 73% hedging cost—a remarkably high margin for FX risk transfer.

This not only highlights the business’s profitability but also shows users’ price insensitivity when facing seamless global payments and exchange rate certainty.

No Interest Rate Stability, On-Chain Economies Can’t Scale

At @SupernovaLabs_, we are committed to introducing interest rate stability into on-chain systems, propelling DeFi into its next institutional phase by building financial infrastructure at the operating system level—not just for crypto natives, traders, and whales, but for everyday enterprises and retail users.

We started with interest rate swaps, having settled over $5 billion in notional volume, serving top-tier prime brokers and institutional borrowers across the full stack.

NDF FX is a domain we are deeply excited about, as we believe it will unlock the next stage of on-chain transaction volume and global stablecoin adoption.

Just as centralized exchanges shaped today’s stablecoin landscape, digital banks will drive the next wave—pushing adoption into the trillions.

In five years, compared to the tens of trillions potentially enabled by stablecoin digital banks and global on-chain financial accounts, today’s ~$350 billion stablecoin market may seem negligible.

FX will be central to this expansion, and our goal is to build the infrastructure layer capable of fully capturing this growth.

Author: Nico

Translated by: Jiahuan, ChainCatcher

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

06-16

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

06-16Amazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

06-16Binance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

06-16Binance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

06-16

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

06-16SlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

06-15