a16z: 7 Diagrams to Understand How Tokenization Transforms the Nature of Assets

a16z: 7 Diagrams to Understand How Tokenization Transforms the Nature of Assets

Originally from: a16z crypto

Tokenized assets, commonly referred to as Real World Assets (RWA), are reshaping the form, liquidity, and foundational architecture of financial systems.

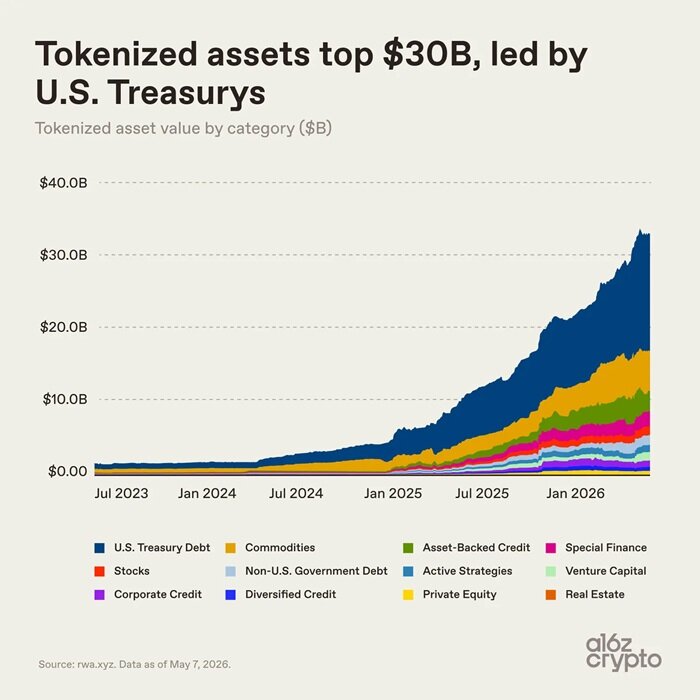

Last month, the tokenized assets market surpassed $30 billion in value and is now stabilizing around $34 billion (excluding stablecoins). This scale is roughly equivalent to that of a regional bank or a top-tier university endowment fund. Though still minuscule compared to the global financial system, it has already generated tangible impact.

Just two years ago, the market was under $3 billion. Since then, transformative changes have unfolded: the U.S. GENIUS Act introduced clearer regulatory frameworks for stablecoins, institutional-grade on-chain infrastructure matured, and numerous financial institutions began deploying blockchain technology nearly simultaneously—driving a tenfold increase in the tokenized assets market within less than two years. (Note: Although stablecoins are excluded from this figure, they have substantially accelerated on-chain payments and settlement, materially fueling overall market growth.)

This article analyzes the rise of tokenized assets through seven charts, exploring their drivers and future trajectory.

The Takeoff of Tokenized Assets: U.S. Treasuries as the Primary Growth Engine

U.S. Treasury securities have emerged as the primary catalyst behind recent growth in the tokenized assets market.

The advantages of tokenized U.S. Treasuries are clear and direct: investors can hold secure, interest-bearing digital assets with enhanced transactional efficiency and flexibility; financial institutions benefit from improved settlement speed, collateral management, and seamless integration into digital financial markets.

Crypto investors can also leverage tokenized government bonds to unlock idle stablecoins, capturing traditional money market returns. Asset managers like BlackRock and Franklin Templeton have strategically entered this space, catalyzing a market worth hundreds of billions of dollars.

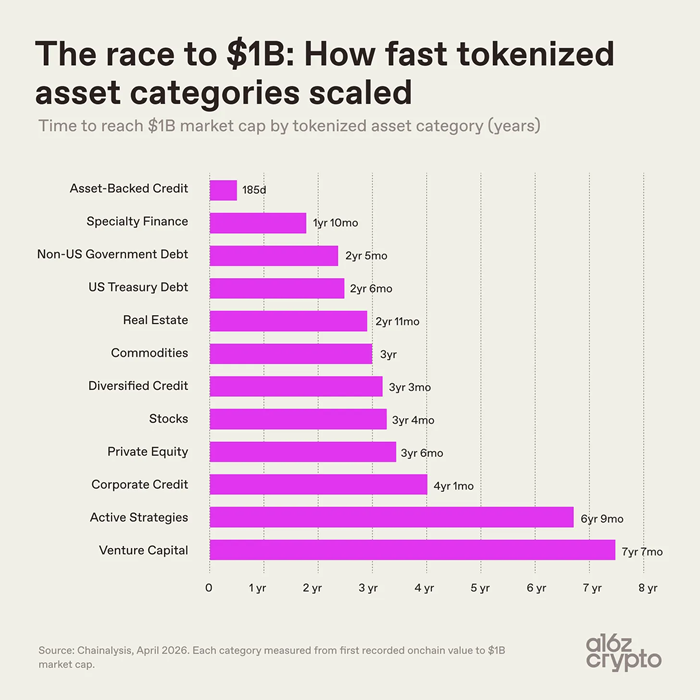

It’s important to note that growth rates across different tokenized asset classes vary significantly—reflecting differences in technical and compliance challenges of onboarding various assets, as well as post-launch market adoption.

Asset-backed credit instruments lead in growth, primarily including home equity line of credit tokens, lending vault tokens, reinsurance contracts, and Bitcoin mining notes. Specialty financial assets such as these reached $1 billion in market cap within two years.

Venture capital assets took over seven years to break the $10 billion mark, while actively managed strategies followed a similar timeline. These assets feature complex structures, long investment horizons, and higher operational and regulatory barriers.

Treasury and commodity tokenization have progressed at a moderate pace—achieving $1 billion in market cap within 2–3 years—and are now mainstream categories.

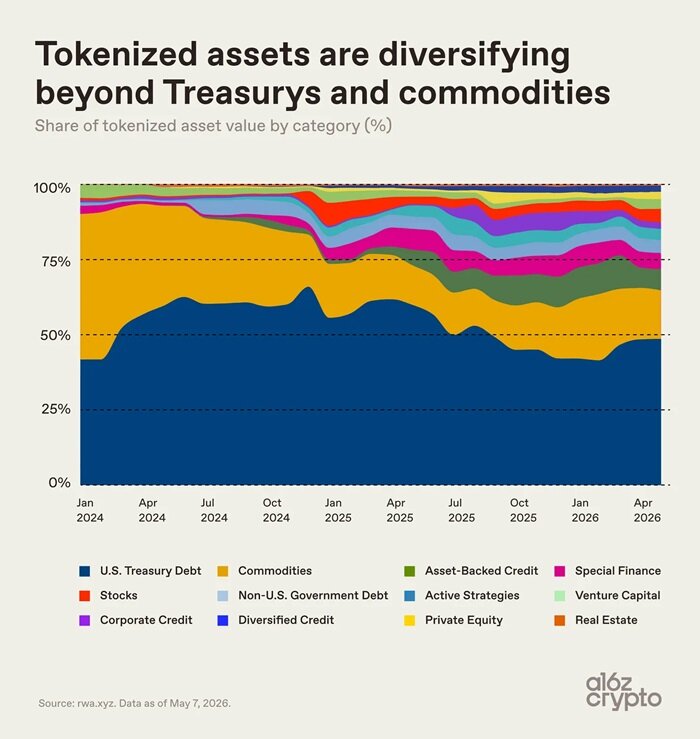

At the beginning of 2024, treasuries and commodities accounted for nearly all tokenized asset market share. Post-2024, credit, specialty finance, and equities have seen steady gains in share, though market concentration remains high. Currently, U.S. tokenized treasuries and commodities together hold about two-thirds of the market.

Market Segmentation of Tokenized Assets

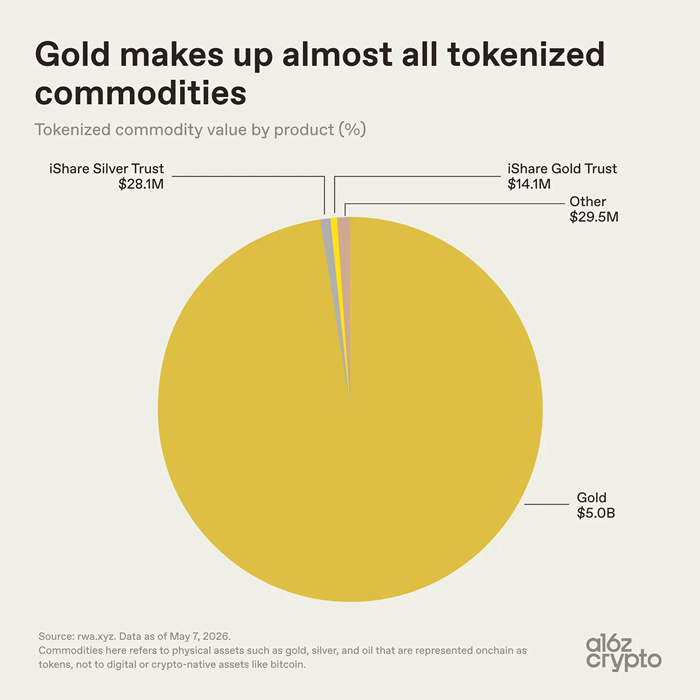

The tokenized commodities segment is highly concentrated: gold tokens dominate almost entirely, with a total market size of approximately $5.1 billion, of which gold tokens account for $5 billion. Silver and other commodity tokens total just $57.6 million, representing less than 0.01%.

Gold is inherently suited to tokenization. The current commodity token market is largely gold-driven because gold has a globally standardized benchmark, is easy to store, resists degradation, and has long been traded via ownership certificates.

Moreover, crypto investors have historically favored gold assets—Bitcoin was early dubbed “digital gold.” Products like Tether’s XAUT and Paxos’ PAXG map physical gold ownership in vaults onto the blockchain, transforming real-world gold rights into digital tokens held in on-chain wallets.

Tokenized oil, agricultural products, and emerging sectors such as energy and compute power remain negligible in market share—indicating they are still in early developmental stages.

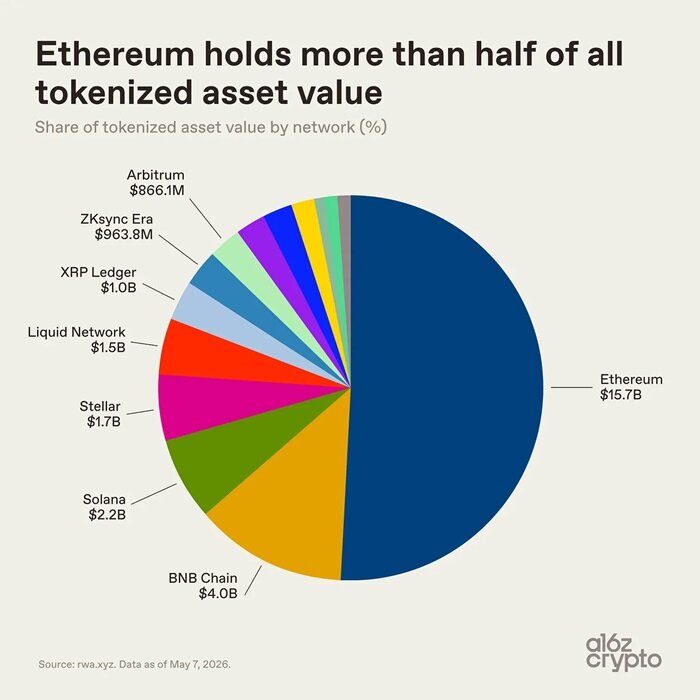

From the underlying public chain perspective, the ecosystem distribution is more diverse. Ethereum maintains its leadership position due to its first-mover advantage in decentralized finance and established institutional adoption, hosting $15.7 billion in assets—accounting for over half the market.

The remainder of the tokenized asset market is distributed across multiple chains: BNB Chain hosts ~$4 billion, Solana ~$2.2 billion, Stellar ~$1.7 billion, Bitcoin sidechain Liquid Network ~$1.5 billion, while XRP Ledger, ZKsync Era, and Arbitrum each have tokenized asset volumes close to $1 billion.

The tokenized asset industry has not consolidated on a single public chain. Assets are distributed across blockchains based on transaction costs, liquidity, compliance requirements, and commercial partnerships. However, the most telling data point isn’t market size—it’s how these assets are actually being used.

Let’s dive deeper:

Most Tokenized Assets Lack Composability Today

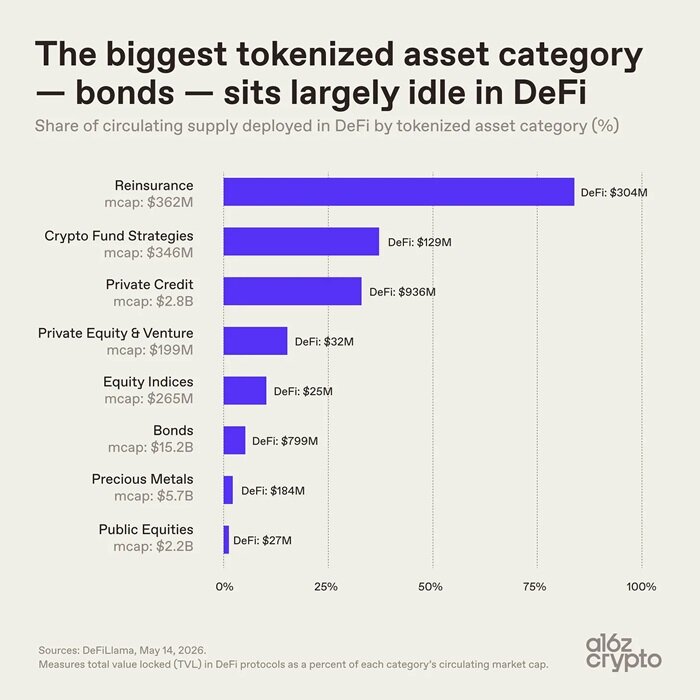

Market size is not the sole key metric—the actual utility and application value of assets offer far greater insight.

Bonds represent the largest class of tokenized assets, with a market cap of $15.2 billion. Yet only 5% of circulating supply is actively used in DeFi protocols—amounting to roughly $800 million. Similarly, precious metal tokenized assets show low utilization: most are used merely for on-chain storage and have not yet become modular building blocks for composability and cross-application reuse.

In contrast, niche tokenized asset classes perform markedly better: reinsurance tokens valued at $362 million achieve an on-chain protocol usage rate of 84%; private credit tokens reach 33% usage. These assets were designed from the outset for on-chain composability. Conversely, dominant assets like treasuries and gold remain primarily focused on simplifying on-chain holding and transfer—not altering their core operational logic. This divergence underscores a fundamental divide in the industry: varying degrees of on-chain native integration among tokenized assets.

Some assets enable cross-chain movement and use, while others treat blockchain merely as a ledger—limiting transfer and composability. Most tokenized assets today are essentially digitized representations of physical assets, migrating records to the blockchain without unlocking true compositional potential. Composability is the core value proposition of on-chain finance and a critical driver for upgrading financial infrastructure.

Pantera Capital’s token-native index reveals that over 70% of tokenized assets currently operate at the lowest level of on-chain native integration. Many tokens are simply digital representations of off-chain assets, with actual control still relying on offline ledgers and intermediaries.

The tokenized asset industry remains in its early stage: one category consists of assets merely digitized on-chain; the other comprises deeply native on-chain assets aligned with blockchain principles.

On-chain composability infrastructure is now robust, and asset variety is growing steadily—but deep integration and application are just beginning.

Future Trends in Tokenized Assets

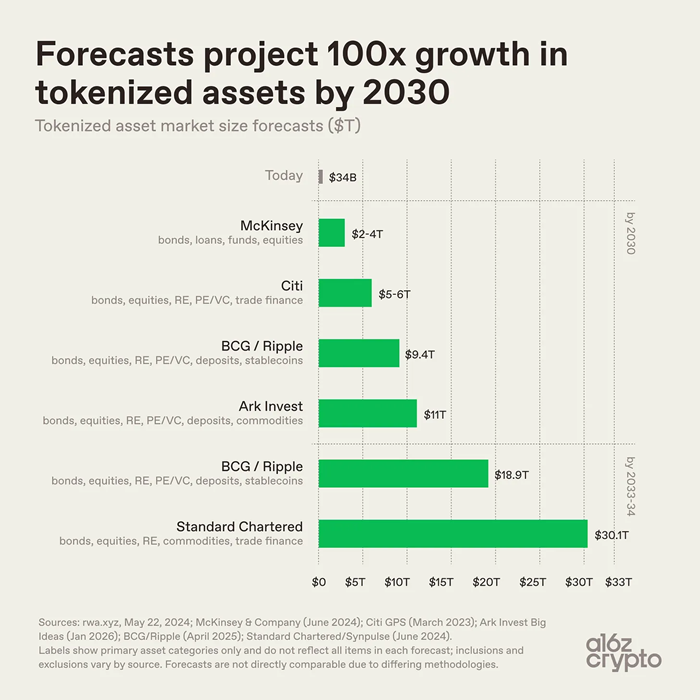

Industry forecasts for the long-term scale of tokenized assets vary widely, but all agree on continued expansion.

McKinsey projects the market will reach $2–4 trillion by 2030;

Ark Invest estimates a $11 trillion market;

Boston Consulting Group, in collaboration with Ripple, forecasts $9.4 trillion by 2030 and $18.9 trillion by 2033;

Standard Chartered predicts the market will exceed $30 trillion by 2034.

Based on these estimates, compared to today’s $34 billion market size, the long-term growth potential for tokenized assets could be over 100x. Of course, discrepancies in numbers stem not from differing views on adoption speed, but from divergent definitions and measurement standards. Each firm defines scope differently—covering different asset classes, whether stablecoins and deposits are included, and what constitutes “tokenization.” For example: McKinsey focuses on bonds, credit, funds, and equities; Standard Chartered includes commodities and trade finance; Boston Consulting and Ripple additionally incorporate deposits and stablecoins. Despite methodological differences, consensus exists across the industry: tokenized assets will undergo explosive scaling.

When viewed against the global financial landscape, tokenized assets remain negligible in scale.

Global bond issuance exceeds $140 trillion—tokenized bonds amount to $15.2 billion, representing just 0.01%;

Global physical gold market value runs into trillions—tokenized gold totals $5 billion, accounting for under 0.02%;

Global equity market value surpasses $100 trillion—tokenized stocks stand at $1.5 billion, or just 0.001%.

Today, emerging segments are maturing steadily. Assets with clear pricing, stable demand, and simple ownership structures—such as U.S. Treasuries, gold, and private credit—have led the way in on-chain deployment. At present, tokenization has not altered the fundamental nature of assets but rather optimized settlement and transfer mechanisms. Deep integration between assets and digital financial infrastructure remains exploratory.

Currently, most tokenized assets reside at the digitization layer—unable to achieve programmable, composable applications. The next phase presents a hard-core challenge: moving more complex components of the financial system onto-chain and embedding tokenized assets deeper into composable, internet-native financial infrastructure.

Author: Moni

Original: Odaily Planet Daily

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

06-16

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

06-16Amazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

06-16Binance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

06-16Binance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

06-16

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

06-16SlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

06-15