Will the AI Giants' IPO Rush Be Wall Street's Last Hurrah?

Will the AI Giants' IPO Rush Be Wall Street's Last Hurrah?

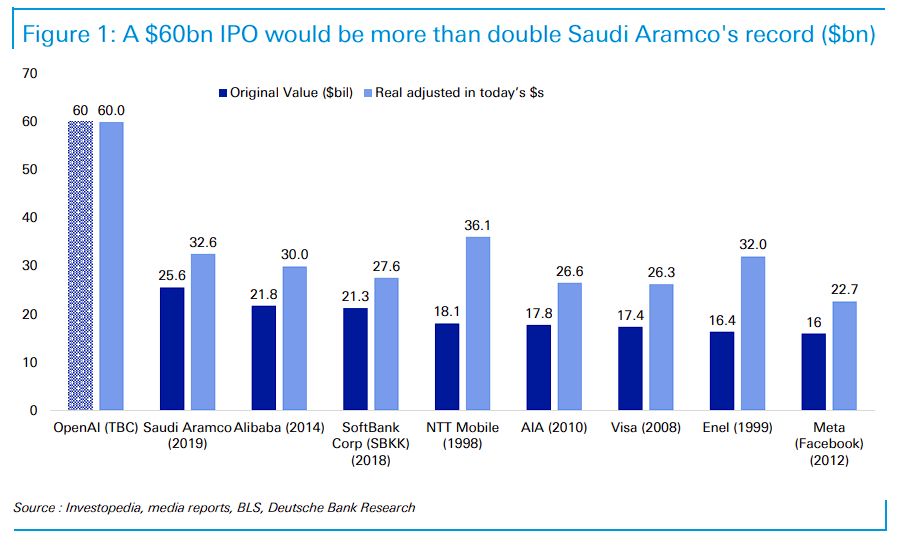

On May 22, according to a report by Wall Street Eyes, OpenAI has prepared to secretly file for an IPO with regulators, potentially going public as early as September this year, targeting a valuation exceeding $1 trillion and raising approximately $60 billion—more than double the previous record of $25.6 billion set by Saudi Aramco’s 2019 IPO.

Meanwhile, its competitor Anthropic is also advancing its own IPO plans and disclosed that second-quarter revenue is expected to more than double to $10.9 billion, positioning it to achieve quarterly operational profitability for the first time. Deutsche Bank’s research notes that the execution of these two IPOs “is likely to become a major swing factor in risk assets this year,” representing a macro-level theme that must be closely monitored.

Yet beneath the dazzling valuations, the financial fundamentals of the two companies are starkly different. OpenAI generated $5.7 billion in revenue in Q1, but its adjusted operating profit margin was -122%, meaning it loses $1.22 for every dollar of revenue. It is projected to only achieve positive cash flow as early as 2029–2030. In contrast, Anthropic reported $4.8 billion in revenue during the same period, with second-quarter projections rising to $10.9 billion and anticipated operational profits of around $559 million—making it the first to cross the profitability threshold.

Analysts point out that despite competing on the same stage, the two firms exhibit fundamentally different business models, presenting public market investors with a rare decision-making dilemma.

The Largest IPO in History: How Shocking Are the Numbers?

Deutsche Bank’s research states that either OpenAI or Anthropic will surpass the IPO fundraising amount of Saudi Aramco’s 2019 offering by over two times. Even after inflation adjustment, both would easily become the largest IPOs in history.

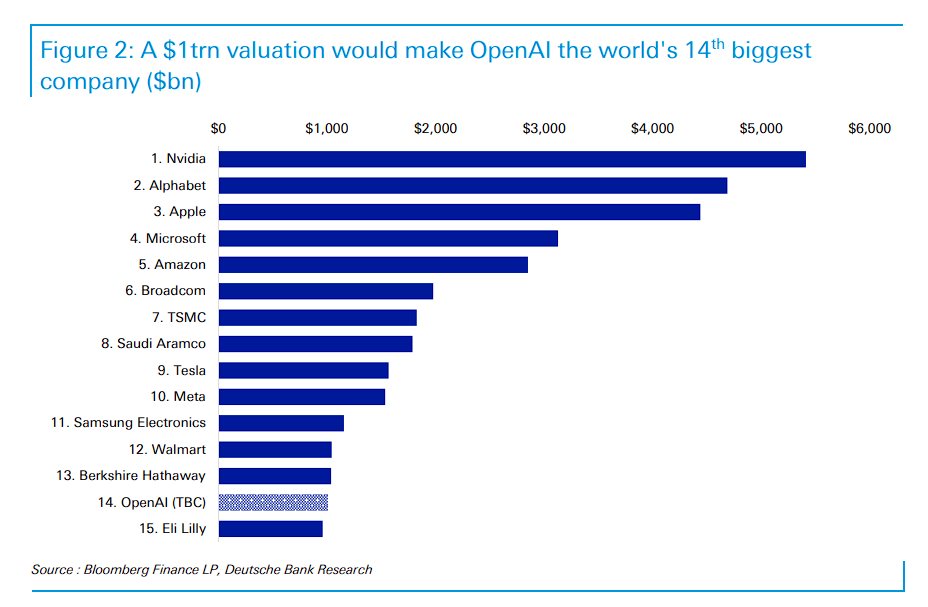

In another research note, Deutsche Bank observes that if OpenAI achieves a target valuation above $1 trillion, it would rank as the world’s 14th largest company by market cap, surpassing Eli Lilly while falling just behind Berkshire Hathaway.

By comparison, Berkshire Hathaway posted revenues exceeding $370 billion last year with net income of $67 billion; Eli Lilly recorded sales over $65 billion and profits of $21 billion. Meanwhile, OpenAI remains unprofitable, with annualized revenue around $30 billion and only a few thousand employees.

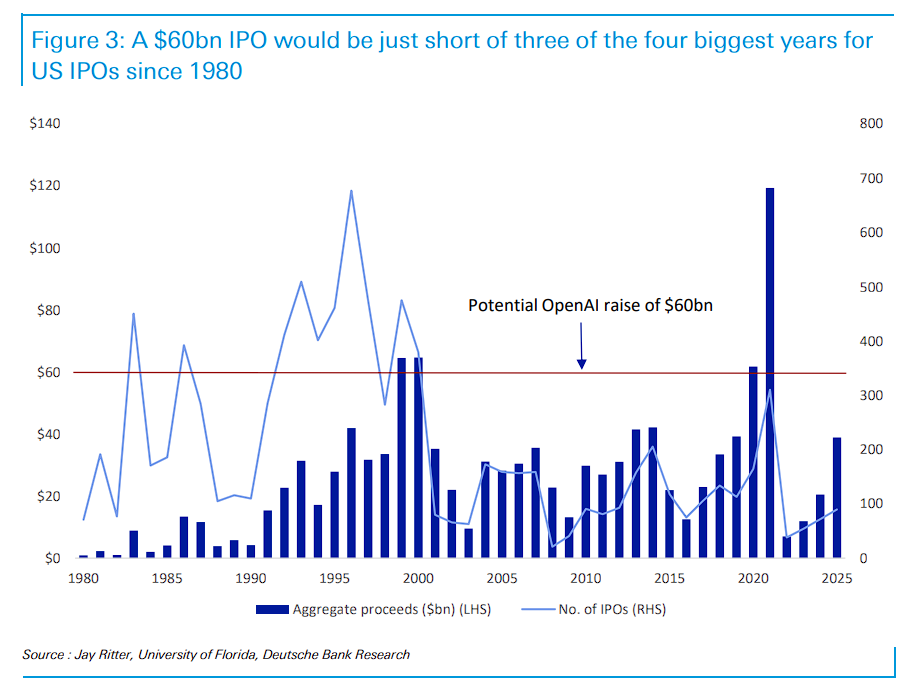

From a market capacity perspective, Deutsche Bank believes the current U.S. equity market capitalization of about $70 trillion is five times that of the peak of the dot-com bubble, indicating significantly stronger absorption capacity than at the end of the 1990s.

Back then, nearly 500 companies went public annually on average, whereas in this decade, the average is only about 120, and today’s public companies are generally much more mature.

Furthermore, a single IPO of $60 billion is only slightly below the total U.S. IPO proceeds in 1999 and 2000 (both around $65 billion), equivalent to half of the record $119 billion raised in 2021.

The "Siphon Effect" of the Giant & Passive Fund Rebalancing

As these tech giants enter public markets, their impact on U.S. equity liquidity has triggered heightened caution across Wall Street.

The clustering of SpaceX, OpenAI, and Anthropic’s IPOs, combined with Nasdaq’s newly introduced “fast-track inclusion” mechanism, is brewing unprecedented passive fund reallocation—the siphon effect of AI giants.

As cited by Wall Street Eyes, JPMorgan estimates that if SpaceX reaches a $2 trillion valuation and 50% of its shares become publicly tradable, passive funds would be forced to liquidate approximately $95 billion worth of holdings in the existing eight major tech stocks (NVIDIA, Apple, Microsoft, Amazon, Google, Broadcom, Meta, Tesla) to free up space for new allocations.

Todd Sohn, Chief ETF Strategist at Strategas, notes that since initial public float typically accounts for only 5% of shares, while ETFs track trillions in assets, this extreme supply-demand imbalance will make index inclusion processes “slightly chaotic,” leaving passive investors no choice but to buy at elevated prices.

Valérie Noël, Trading Director at Syz Group, says the market has already begun pricing in downward pressure on existing large-cap stocks.

According to information disclosed on March 28 this year, OpenAI’s public listing represents a substantive referendum on the entire AI investment thesis. The data shows OpenAI’s revenue reached $13.1 billion in 2025, but a projected net loss of $14 billion in 2026.

At the same time, OpenAI has committed to investing approximately $140 billion in infrastructure by 2033. If S&P Global, FTSE Russell, and Nasdaq adopt fast-track inclusion rules, it could immediately force passive funds managing $24–48 billion to purchase shares post-IPO.

With such massive capital restructuring underway, ordinary investors—whether active or passive—will have their portfolios passively reshaped by rule changes.

Deutsche Bank’s research emphasizes that the execution of these IPOs will be a pivotal swing factor in the direction of risk assets this year. PitchBook’s analysis is even more direct:

Private markets have experienced a “systemic quality inversion”—the companies with the highest valuations score the lowest on actual business quality metrics when priced in public markets.

For the average investor holding index funds or ETFs, this game cannot be avoided: regardless of intent, their portfolios will be passively restructured as index rules evolve.

For active investors, once the S-1 filing is made and all financial secrets are exposed under sunlight, the market faces a clear choice: Will you trust a company that has already found a path to profitability, or a giant requesting several more years and tens of billions in capital to explore profitability?

The answer will determine whether this frenzy marks the dawn of a new cycle—or the final dance before the feast ends.

Two Extremes: Anthropic’s Profitability vs. OpenAI’s Massive Losses

Despite soaring valuations, the financial realities of these two AI leaders present dramatically different pictures. Anthropic has already turned profitable, breaking the conventional wisdom that AI companies’ massive spending inevitably erodes near-term profitability.

As reported by Wall Street Eyes, citing The Wall Street Journal on Wednesday, Anthropic’s second-quarter revenue is expected to more than double to $10.9 billion, achieving operational profits of approximately $559 million.

Anthropic’s gross margin has surged from 38% to over 70%. Its CEO Dario Amodei joked that revenue growth has become “too difficult to handle.”

The company’s success stems largely from explosive demand from enterprise clients for its programming tools, with roughly 85% of revenue coming from businesses and developers—a model characterized by clear payment willingness and low service costs.

In contrast, OpenAI remains unprofitable.

As cited by Wall Street Eyes, data shows OpenAI generated $5.7 billion in Q1 revenue but posted an adjusted operating profit margin of -122%, meaning it loses $1.22 for every dollar earned.

Approximately 85% of OpenAI’s revenue comes from ChatGPT consumer subscriptions. Despite having 55 million paying users, it serves over 900 million weekly active users, creating a massive cost black hole driven by inference expenses from the vast free user base.

OpenAI expects to achieve positive cash flow by 2029 or 2030. CEO Sam Altman and Application Business CEO Fidji Simo are actively shifting focus toward commercial clients capable of generating direct revenue.

On the IPO narrative front, the two companies tell entirely different stories. Anthropic holds verifiable quarterly profitability data, allowing its story to be compared to Salesforce or ServiceNow—an enterprise software logic.

OpenAI, however, must convince the market that AI agents, image generation, and advertising will eventually convert massive consumer traffic into profits.

In Sam Altman’s vision, ChatGPT’s ad business could generate around $10.2 billion in revenue by 2030—but that requires time, and time is precisely the scarcest resource OpenAI is trading for growth through losses.

AI Giants Rushing IPO: Is This Just Passing the Hot Potato to Retail Investors?

As reported by Wall Street Eyes, Joachim Klement, Director General at Panmure Liberum, views this wave of AI giant IPOs as essentially a “risk transfer” — a mass shift of early-stage investment risks onto retail investors, pension funds, and other institutions through exit strategies.

He argues that companies like OpenAI and Anthropic are accelerating their IPOs during periods of high investor sentiment, aiming to capture high valuations before speculative hype fades. Early institutional investors can exit safely into the public market, while retail investors and pension funds inherit the full risk of financial logic eventually returning to reality.

He directly characterizes this process as “a large-scale transfer of investment risk from current holders to those willing to pay for the story.”

Klement draws a parallel to Greenspan’s 1996 “irrational exuberance” warning—three years before the bubble burst. He forecasts that AI speculation may continue through 2026, with little likelihood of major cloud providers cutting back on investments. But “impossible math” will eventually return to reality: “It may not happen in 2026, but perhaps in 2027 or 2028.”

Welcome to join our community for discussion:

Written by Dong Jing, Source: Wall Street Eyes

Disclaimer: Contains third-party opinions, does not constitute financial advice

Iranian state media denies the existence of a memorandum of understanding between Iran and the U.S.

10 mins ago

Binance Alpha Citrea (CTR) Airdrop Threshold: 211 Points

14 mins agoChina accounts for over 80% of the global humanoid robotics market

26 mins agoGlassnode: Approximately 7.75 million BTC are currently in a loss position

43 mins ago

Bytedance has issued equity incentives for a specific business unit for the first time, opening up "DouBao Shares" subscription rights to Seed employees this month

43 mins agoData: NEAR Intents has generated over $33 million in fees since launch

49 mins ago

Data: 21Shares and Bitwise ETF collectively purchased $68 million worth of HYPE last week

51 mins ago