ChainThink

Stay ahead, master crypto insights

CRLCLE Launches, the Fed Understood 3 Years Ago

CRLCLE Launches, the Fed Understood 3 Years Ago

2025-06-05 10:26

On June 5, the stablecoin giant Circle will officially go public on the New York Stock Exchange with the stock code CRCL, which is the most anticipated IPO in the cryptocurrency sector since Coinbase (stock code COIN) went public on Nasdaq in 2021.

According to Bloomberg, Circle plans to issue 24 million shares in this IPO, raising $624 million, with a target valuation of $6.7 billion. However, according to the latest market data, this target has been raised to $7.2 billion, and it has been oversubscribed by more than 25 times, indicating that the market had previously underestimated the enthusiasm for the stablecoin concept.

This enthusiasm is not only from retail investors; many institutional investors, such as Cathie Wood from Ark Invest and Larry Fink from BlackRock, have publicly stated that they will make large subscriptions, accounting for about 30% of the financing. Just a few weeks before the official IPO date, Circle was also involved in "acquisition rumors" with Coinbase and Ripple.

Related reading: While rushing for an IPO, talking about selling, what is Circle trying to do?

In recent years, stablecoins have emerged as one of the few concepts that can bet on the growth of the cryptocurrency market and the popularization of blockchain technology in institutional investment reports, making Circle the first stock in the stablecoin concept.

Last month, the Hong Kong Legislative Council passed the "Stablecoin Ordinance Bill" in a third reading, and the Hong Kong and A-share markets saw a surge in stablecoin-related stocks and digital currency sectors, with many companies hitting a 20% limit. According to Caixin, Guolong Holding also saw its stock price surge by 26.6% on June 3 due to its joint investment in Circle with IDG Capital in 2016.

Under the hype, the traditional financial circle's topic of "What is a stablecoin?" has quickly gained popularity. In fact, for stablecoin technology, especially CBDC (Central Bank Digital Currency), it has long been a strategic plan for many countries. In the United States, due to the executive ban on CBDC by the Trump administration, the development of the "private stablecoin" field has advanced rapidly in a few months, passing the "GENIUS" Stablecoin Act on May 20.

Regarding the stablecoin technology itself, the US government has done extensive research. On January 31, 2022, the Federal Reserve released a report titled "Stablecoins: Potential and Impact on the Banking System." In the report, the Federal Reserve focused on the potential impact of stablecoins on the banking system and credit intermediation. For readers who are not familiar with the concept and knowledge of stablecoins, it may be a good "Stablecoin 101 textbook."

The following is a translation of the original content of the Federal Reserve's "Stablecoins: Growth Potential and Impact on Banking":

TL;DR

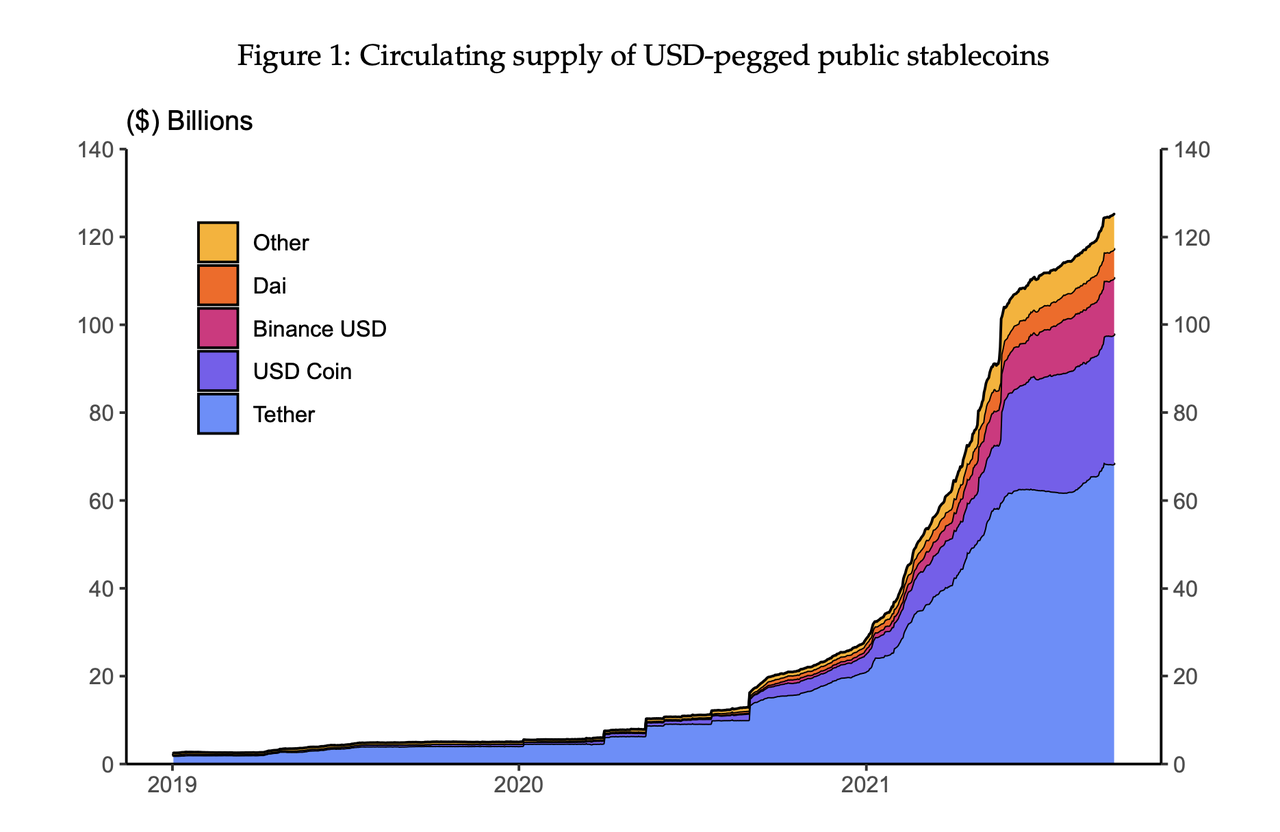

Stablecoins are digital currencies that peg their value to an external reference, usually the US dollar (USD). They play a key role in the digital market, and their growth could stimulate innovation in the broader economy. In the past year, the supply of USD-backed stablecoins on public blockchains has exploded, reaching nearly $130 billion by September 2021, an increase of over 500% compared to the previous year.

As stablecoins receive more attention, a series of questions have been raised, including the stability of their peg, consumer protection, KYC and compliance, and the scalability and efficiency of settlement. We will focus on the potential impact of stablecoins on the banking system and credit intermediation. Although a range of issues related to stablecoins can be addressed through appropriate institutional safeguards, regulations, and technological advancements, the continued growth and circulation of stablecoins will ultimately affect the traditional banking system in significant ways.

In this note, we first discuss the basics of stablecoins, their current use cases, and their growth potential. Second, we examine the historical behavior of stablecoins during periods of cryptocurrency and broader financial market distress. We found that USD-backed stablecoins exhibit safe asset quality because their prices temporarily exceed the pegged price in secondary markets during extreme market conditions, thereby incentivizing more stablecoin issuance. We also highlight the "run" risk of certain stablecoins backed by non-cash equivalent risk assets.

Finally, we outline possible scenarios for bank reserves, credit intermediation, and central bank balance sheets if stablecoins gain broader attention. Our research shows that the widespread adoption of asset-backed stablecoins can be supported within a two-tier fractional reserve banking system without negatively affecting credit intermediation. In such a framework, stablecoin reserves are held as commercial bank deposits, and commercial banks conduct fractional reserve lending and maturity transformation similar to traditional bank deposits. We also found that replacing physical cash (paper money) with stablecoins can lead to more credit intermediation. In contrast, a "narrow banking" framework that requires stablecoin issuers to back their stablecoins with central bank reserves would minimize the risk of a "run" on stablecoins but may reduce credit intermediation.

The Basics of Stablecoins

Stablecoins are digital currencies recorded on distributed ledger technology (DLT), typically a blockchain, and are pegged to a reference value. Most circulating stablecoins are pegged to the US dollar, but stablecoins can also be pegged to other fiat currencies, a basket of currencies, other cryptocurrencies, or commodities like gold. As a store of value and medium of exchange on DLT, stablecoins enable them to be exchanged or integrated with other digital assets.

Stablecoins differ from traditional digital currencies, such as bank deposit accounts, in two main aspects. First, stablecoins are cryptographically secured. This allows users to settle transactions almost instantly, without double-spending or intermediaries facilitating settlements. On public blockchains, this also allows 24/7/365 trading. Second, stablecoins are typically built on programmable DLT standards and allow for composability. In this context, "composability" means that stablecoins can act as independent building blocks, interoperable with smart contracts (self-executing programmable contracts) to create payment and other financial services. These two key features support the current use cases of stablecoins and drive innovation in both financial and non-financial fields.

Since 2020, the usage of stablecoins on public blockchains such as Ethereum, Binance Smart Chain, or Polygon has surged. By September 2021, the circulating supply of the largest USD-pegged public stablecoin approached $130 billion. The chart shows that the circulating supply of public stablecoins grew particularly strongly at the beginning of 2021, with an average monthly growth of about 30% in the first five months of this year.

Current Types of Stablecoins

Stablecoins are a new and broadly defined technology that can take various forms. This technology is currently implemented in specific forms, which we will describe below and summarize in Table 1. However, please note that stablecoin technology is still in its early stages and has high potential for innovation. The current implementations discussed below, along with their current status in the regulatory environment, do not reflect all potential deployments of stablecoin technology.

The circulating supply of the top ten public stablecoins pegged to the US dollar by market capitalization. Data from January 2019 to September 2021. Other categories include Fei, TerraUSD, TrueUSD, Paxos Dollar, Neutrino USD, and HUSD.

Public Reserves Supported Stablecoins

Most existing stablecoins circulate on public blockchains, such as Ethereum, Binance Smart Chain, or Polygon. Among these public stablecoins, most are supported by cash equivalents such as bank deposits, treasury bills, and commercial paper. These reserves-supported stablecoins are also known as custodial stablecoins, as they are issued by intermediaries acting as custodians of cash equivalents and provide 1-to-1 stablecoin liability redemption in USD or other fiat currencies.

Some public reserves-supported stablecoins have come under scrutiny regarding their full backing and robustness. In particular, Tether, the stablecoin with the largest circulating supply, agreed to pay $41 million to resolve a dispute with the U.S. Commodity Futures Trading Commission, which accused Tether of misrepresenting the adequacy of its USD reserves. Other widely used reserves-supported stablecoins with different levels of financial audits include USD Coin, Binance USD, TrueUSD, and Paxos Dollar.

Public Algorithmic Stablecoins

Some stablecoins use other mechanisms to stabilize their price rather than relying on the robustness of underlying reserves. These stablecoins are often referred to as algorithmic stablecoins. While reserves-supported stablecoins are issued as liabilities on the balance sheets of legally registered companies, algorithmic stablecoins are maintained by smart contract systems that operate exclusively on public blockchains. The ability to control these smart contracts is typically granted through holding governance tokens, which are specialized tokens used for voting on protocol or governance parameter changes. These governance tokens can also represent direct or indirect claims on future cash flows from using the stablecoin protocol.

The public algorithmic stablecoin space is highly innovative and difficult to classify. However, these stablecoins are generally designed based on two mechanisms: (1) collateral mechanisms and (2) algorithmic peg mechanisms. When users deposit unstable cryptocurrencies (such as Ethereum) into the Dai smart contract protocol, they can mint collateralized public stablecoins like Dai. Users then receive a loan of Dai (pegged to the USD) with a collateral ratio exceeding 100%. If the value of the Ethereum deposit falls below a certain threshold, the loan will be automatically liquidated.

By contrast, algorithmic peg mechanisms use automated smart contracts to protect the peg by buying and selling stablecoins and related governance tokens. However, these pegs may encounter instability or design flaws, leading to "instability," as exemplified by the algorithmic stablecoin Fei, which briefly broke its peg after its launch in April 2021.

Institutional or Private Stablecoins

In addition to reserves-supported stablecoins circulating on public blockchains, traditional financial institutions have also developed reserves-supported stablecoins, also known as "tokenized deposits." These institutional stablecoins are implemented on permissioned (private) DLT and are used by financial institutions and their customers for efficient wholesale transactions. The most well-known institutional stablecoin is JPM Coin. JPMorgan and its customers can use JPM Coin for same-day repurchase settlements and manage internal liquidity.

These private, reserves-supported stablecoins are functionally and economically comparable to products offered by certain money transmitters. For example, PayPal and Venmo (a subsidiary of PayPal) allow users to make near-instant transfers and payments within their network, and the balances held by these companies resemble reserves-supported stablecoins. The key difference lies in the use of centralized databases instead of permissioned DLT.

Use Cases and Growth Potential of Stablecoins

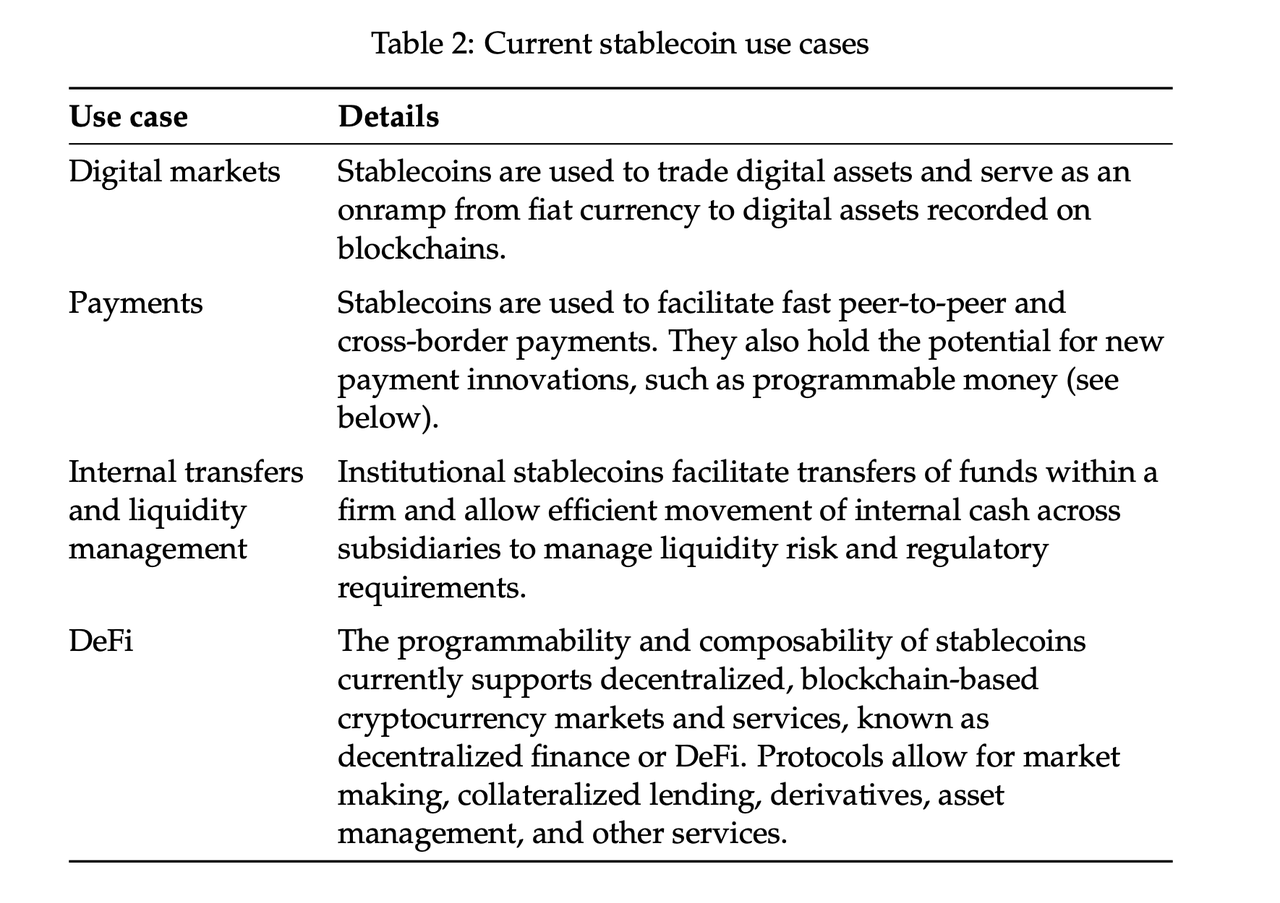

Strong use cases are driving the growth of various forms of stablecoins. We summarize these use cases. The most important current use case for stablecoins is their role in cryptocurrency trading on public blockchains. Investors often prefer using public stablecoins for cryptocurrency trading because this allows near-instant 24/7/365 trading without relying on non-DLT payment systems or the custody of fiat currency balances.

Aside from being used for cryptocurrency trading, public and institutional stablecoins are currently used for near-instant, 24/7, non-intermediated payments with potentially low fees. This is especially relevant for cross-border transfers, which often require multiple days and high fees. Companies also use institutional stablecoins to transfer cash almost instantly between subsidiaries to manage internal liquidity and facilitate existing financial market wholesale transactions, such as same-day repurchase transactions. Finally, since public stablecoins are programmable and composable, they are widely used in decentralized, blockchain-based markets and services, known as decentralized finance or DeFi. DeFi protocol systems allow users to directly participate in various cryptocurrency-related markets and services, such as market making, margin lending, derivatives, and asset management, without traditional intermediaries. As of September 2021, approximately $60 billion in digital assets were locked (staked) in DeFi protocols.

Future Growth Potential

The defining characteristics of stablecoins, cryptographic security, and programmability support powerful use cases that are currently driving the usage of public and institutional stablecoins. However, these features have the potential to drive innovation beyond the current use cases, which mainly focus on the cryptocurrency market, certain peer-to-peer payments, and institutional liquidity management by large banks. Looking ahead, stablecoin technology may see diverse implementations and drive innovation in multiple growth areas: more inclusive payment and financial systems, tokenized financial markets, and microtransactions that promote technologies like Web 3.

More Inclusive Payment and Financial Systems

Stablecoins have the potential to stimulate growth and innovation in payment systems, enabling faster and cheaper payments. Since stablecoins can be used to transfer funds almost instantly between digital wallets at potentially low fees, they may reduce payment barriers and pressure existing payment systems to offer better services. This is particularly important for cross-border transfers, which may take several days to settle and incur high fees. These fees and delays are a burden for low- and middle-income countries.

Stablecoins may also support a more inclusive financial system through the growth of DeFi, which may require stablecoins as essential components. It should be noted that DeFi faces significant challenges, including complex user experiences, lack of consumer protection, frequent hacking attacks, protocol functional failures, and market manipulation. Furthermore, almost all DeFi protocols only support trading or lending of cryptocurrencies or non-fungible tokens (NFTs). If DeFi protocols mature beyond their current state and integrate with more extensive financial markets to support real-world economic activities, they could encourage a more inclusive financial system, allowing investors to directly participate in the market without intermediaries. This growth of DeFi may drive an increase in stablecoin usage.

Tokenized Financial Markets

Additionally, stablecoins may play a key role in the tokenization of financial markets. This would involve converting securities into digital tokens on DLT and using stablecoins for trading and servicing. For delivery versus payment (DvP) transactions, such as the purchase of securities, tokenized markets would allow for real-time settlement at very low costs. This could enhance liquidity, transaction speed, and transparency while reducing counterparty risk, transaction costs, and other market participation barriers. This may be particularly beneficial for certain asset classes, such as real estate, by enabling partial ownership of tokenized assets and more transparent price discovery. For payment versus payment (PvP) transactions, such as currency swaps, tokenization would also allow for near-instant execution, unlike the current traditional T+2 framework, where the payment of swaps occurs after the business day's settlement. Additionally, for both types of transactions, tokenized financial markets would benefit from the programmability of DLT, which can automate security services and regulatory requirements, such as required holding periods. If financial markets are partially or fully tokenized, this may further drive the growth of stablecoin usage.

Next-Generation Innovation

Finally, stablecoins have the potential to support next-generation innovation. One example of this innovation is Web 3, which may shift from centralized network platforms and data centers to decentralized networks. In this paradigm, the revenue of internet services and social media platforms will shift from advertising to micropayments, driven by the emergence of efficient, integrated online payment systems. For example, one can imagine a search engine or video streaming platform supported by near-instant small payments in stablecoins, rather than advertising revenue and the sale of user data. If this shift in network services were to materialize, it could drive further growth in stablecoins.

In summary, the current use of stablecoins is mainly driven by cryptocurrency trading, limited peer-to-peer payments, and DeFi. Looking ahead, stablecoins may achieve further growth by promoting more inclusive payment and financial systems, the tokenization of financial markets, and potential next-generation innovations such as Web 3.

Peg Stability

Stablecoin peg stability is a core issue. This is not the focus of our paper, but we briefly discuss this important issue here. In this section, we will first outline the sources of peg instability in currently public reserves-supported stablecoins and discuss how to address these sources. Then, we will review how stablecoins have acted as potential safe assets in digital markets and provide evidence that currently public reserves-supported stablecoins may have already played this role in the cryptocurrency market.

Currently, there are two forms of peg instability in public reserves-supported stablecoins: investor redemption risk by the issuer and price dislocation in the secondary market. The former relates to the safety and robustness of stablecoin reserves. If stablecoin holders lose confidence in the robustness of stablecoin support, a panic may occur. A run on stablecoins may pose spillover risks to other asset classes, as stablecoin reserves are sold or offloaded to meet redemption demands. Moreover, a run on stablecoins may disrupt markets and services that rely on stablecoins through interoperability, causing further complications. We believe that this type of instability can be addressed through appropriate institutional and/or regulatory safeguards, such as transparent financial audits and sufficient requirements for the liquidity and quality of stablecoin reserves. Concerns about redemption risk and the extent to which it can be resolved were recently mentioned in Quarles (2021).

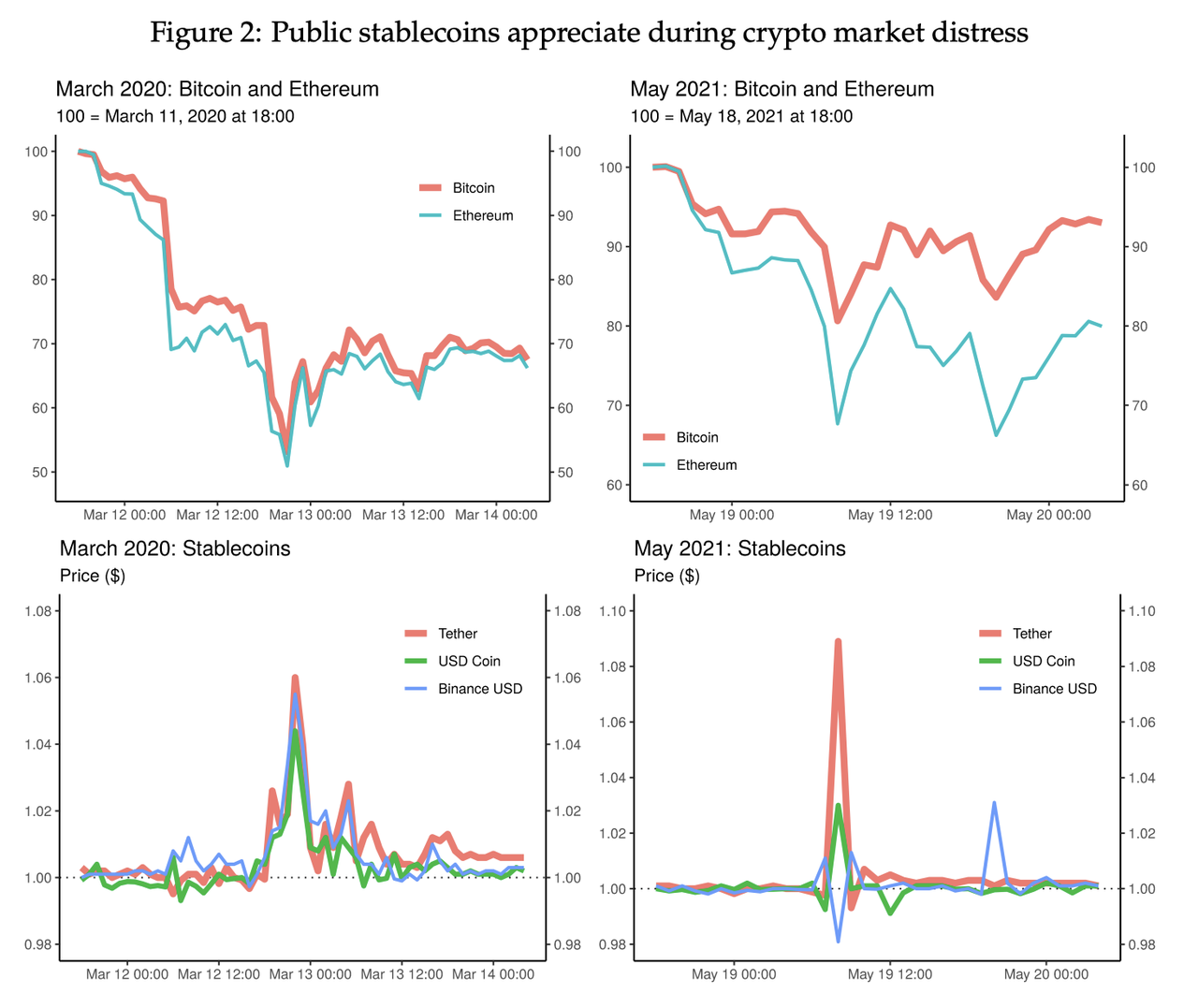

The second form of peg instability in public reserves-supported stablecoins stems from imbalances in supply and demand in the secondary market. Since these stablecoins are traded on both centralized and decentralized exchanges, they are susceptible to demand shocks, which may temporarily cause them to break their peg until the stablecoin issuer adjusts the supply. In particular, since public stablecoins serve as a store of value in public blockchain-based markets, these stablecoins experienced high demand during periods of cryptocurrency market turmoil, as investors rushed to liquidate their speculative positions into stablecoins. During these events, the prices of major public reserves-supported stablecoins tend to rise temporarily until the issuer adjusts the supply. For example, the figure shows the cryptocurrency market crash on March 12, 2020, and May 19, 2021. The first event occurred during a general market turbulence around the spread of COVID-19. The second event occurred during a period of crypto market downturn related to significant deleveraging. During these two periods, the prices of speculative cryptocurrencies like Bitcoin and Ethereum fell by 30% to 50%, while the prices of major public reserves-supported stablecoins rose significantly.

For these extreme cryptocurrency market distress events, stablecoins appreciated as digital safe assets, while more speculative cryptocurrencies temporarily plummeted until stablecoin issuers could increase their supply and purchase reserves and/or stablecoins experience price pressure from arbitrageurs. The behavior of these public stablecoins is unique, unlike high-quality money market funds, which experienced significant outflows during the 2008 global financial crisis and the worst periods of the COVID-19 pandemic.

These events demonstrate the potential of stablecoins as a digital safe haven during market distress. While discussions about financial stability risks of public reserves-supported stablecoins have primarily focused on redemption risks specific to individual stablecoin reserve forms, our analysis suggests that countercyclical secondary market demand for stablecoins can reduce redemption risks during market downturns. With appropriate safeguards and regulations, stablecoins have the potential to provide stability comparable to traditional forms of safe value.

Potential Impact of Stablecoins on Credit Intermediation

If stablecoins are widely adopted throughout the financial system, they could have significant impacts on the balance sheets of financial institutions. Regulators, market participants, and scholars have particularly focused on the potential of stablecoins to disrupt bank-dominated credit intermediation. In this section, we analyze several possible scenarios in which reserves-supported stablecoins are widely adopted in the financial system. We focus on reserves-supported stablecoins rather than algorithmic stablecoins because reserves-supported stablecoins are currently the largest and have the closest connection to the existing banking system. Using these scenarios, we emphasize that the impact of stablecoin adoption on credit provision hinges on two factors: the source of inflows into stablecoins and the composition of stablecoin reserves.

We summarize our findings. We found that in most of the scenarios we considered, credit provisioning may not be negatively affected. In fact, replacing physical currency (cash) with stablecoins may allow for more bank-dominated credit supply. An exception worth noting is that large-scale credit disintermediation could occur if stablecoins are fully backed by central bank reserves, which we refer to as the narrow banking framework. In this framework, redemption risk is minimized at the cost of greater credit disintermediation (deintermediation).

Sources of Inflows

If stablecoins are widely adopted, the main inflows may come from three sources: physical currency (cash), commercial bank deposits, and cash equivalents (or money market funds). First, as a form of digital currency, stablecoins will replace part of the cash in circulation, especially as the economy becomes more digitized. In some of our scenarios, we observe an increase in credit supply as users substitute cash for reserves-supported stablecoins. This is because cash is a direct liability of the central bank, replaced by reserves-supported stablecoins, which can create credit through loans or security purchases depending on the reserve framework.

Second, if households and businesses are more willing to hold stablecoins instead of traditional balances at commercial banks, stablecoins may see inflows from commercial bank deposits. Policymakers are very interested in this source of inflow because there is a general concern that a large substitution of deposits could disrupt commercial bank credit supply. We show that the impact of deposit substitution on credit supply can be positive, negative, or neutral, depending on the reserve framework. Finally, stablecoins may see inflows from cash equivalents (or money market funds). This may have no impact on credit supply because it requires recycling funds back into the banking system, which we will discuss in later sections.

Reserve Composition

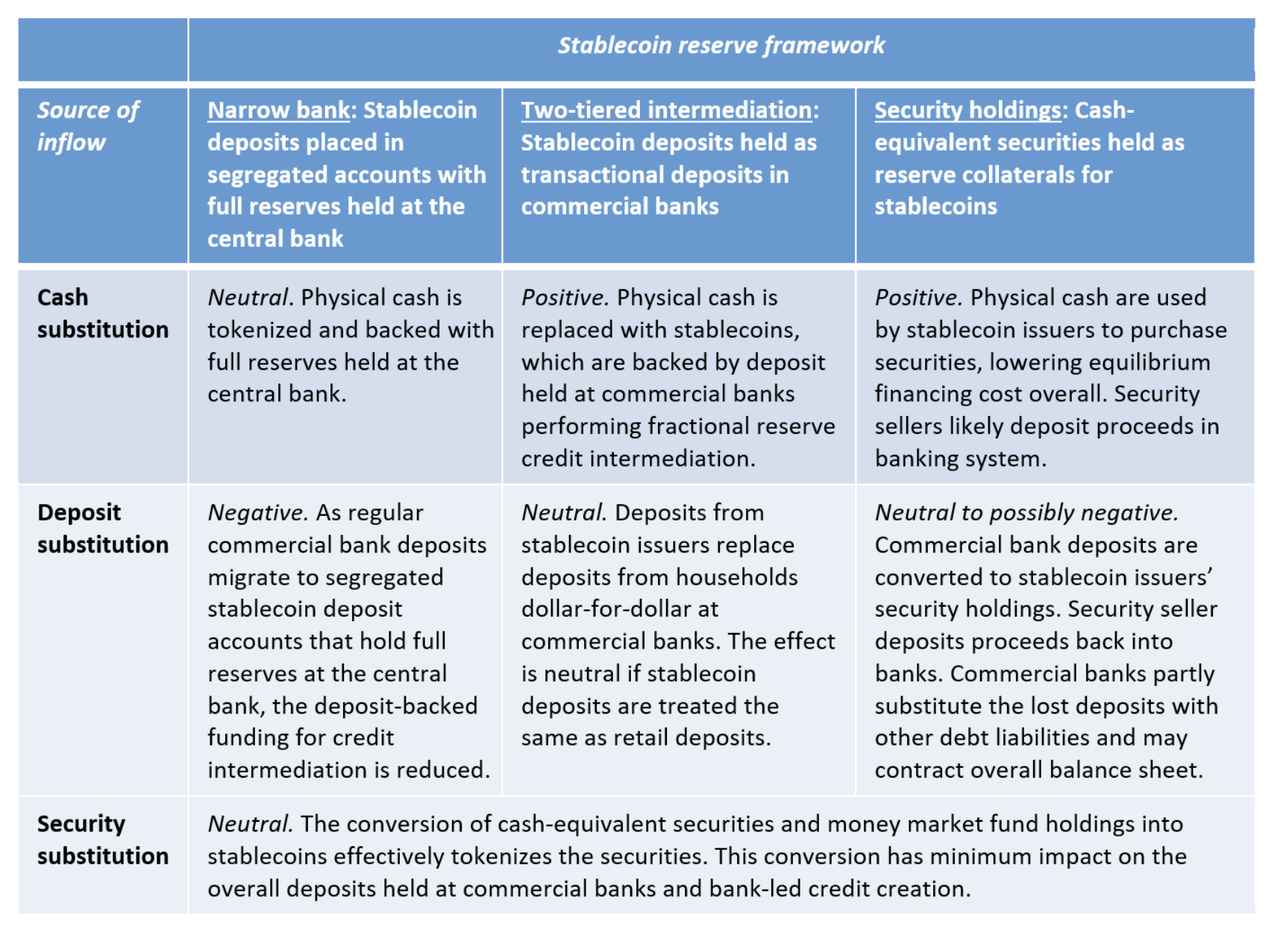

The impact of widely adopting reserves-supported stablecoins on credit provision also depends on the composition of stablecoin reserves. We present three reasonable stablecoin reserve frameworks: narrow banking, two-tier intermediation, and security holding. As shown in the figure above.

In the narrow banking framework, stablecoins need to be supported by commercial bank deposits, which are fully backed by central bank reserves. Equivalently, commercial banks could issue fully backed stablecoins (or tokenized deposits) backed by central bank reserves. The narrow banking approach is roughly equivalent to a retail central bank digital currency, where the digital currency is a liability of the central bank, but households and companies can use it through intermediaries such as commercial banks or fintech companies. The People's Bank of China has adopted this framework in its national-supported digital currency (called digital currency and electronic payment), digital yuan, or e-yuan. This possibility was also mentioned in the proposed STABLE bill in the United States, which requires stablecoins to maintain reserves at the central bank.

Although the narrow banking framework ensures the peg stability of stablecoins, as it is essentially a pass-through of central bank digital currency (CBDC), this reserve framework constitutes the greatest risk of credit disintermediation. Financial stress or panic could lead to a large transfer of conventional commercial bank deposits to narrow banking stablecoins, which could disrupt credit supply. Although this credit disruption effect can be mitigated by limiting stablecoin holdings and differential reserve interest rates, the overall structure of the narrow banking approach for stablecoin reserves could undermine the stability of the banking system. Additionally, the narrow banking approach could lead to an expansion of the central bank's balance sheet to accommodate the demand for reserve balances from stablecoin issuers.

These concerns about narrow banking stablecoins reflect broader concerns about narrow banking, which the Federal Reserve has already noted. In a recent regulation that would affect narrow banking (officially called straight-through investment entities or PTIEs), the Federal Reserve stated, "We are concerned [narrow banking] could disrupt financial intermediation in unforeseen ways and may also have negative effects on financial stability" (Regulation D: Reserve Requirements for Depository Institutions, 2019). Additionally, the Federal Reserve outlined serious concerns about the demand for reserve balances, stating, "[narrow banking] could result in a very large demand for reserve balances. To maintain an ideal monetary policy stance, the Federal Reserve may need to expand its balance sheet and reserve supply to meet this demand."

Compared to the narrow banking framework, in the two-tier intermediary framework, stablecoins will be supported by commercial bank deposits used for fractional reserve banking operations. Similarly, commercial banks could also issue stablecoins or provide tokenized deposits for fractional reserve banking operations. It is important to clarify that this does not mean stablecoins are not fully backed. Instead, stablecoin issuers rely on commercial bank deposits as assets, and commercial banks use stablecoins and/or stablecoin deposits to conduct fractional reserve banking operations, meaning that stablecoins are ultimately supported by a combination of loans, assets, and central bank reserves. It affects the effective reclassification of conventional deposits into stablecoin deposits. It is important that the treatment of stablecoin deposits must be the same as non-stablecoin deposits in terms of statutory reserve requirements, liquidity coverage ratios, and other regulatory and self-imposed risk limits to maintain banking intermediation unchanged.

Finally, stablecoin issuers can hold cash equivalents, such as Treasury bills and high-quality commercial paper, instead of keeping funds in commercial banks. These securities can be purchased directly or indirectly through money market funds. This is the primary framework adopted by current public reserves-supported stablecoin issuers, such as Tether, which the Federal Reserve Chair Jerome Powell recently described as "like a money market fund."

Scenario Building

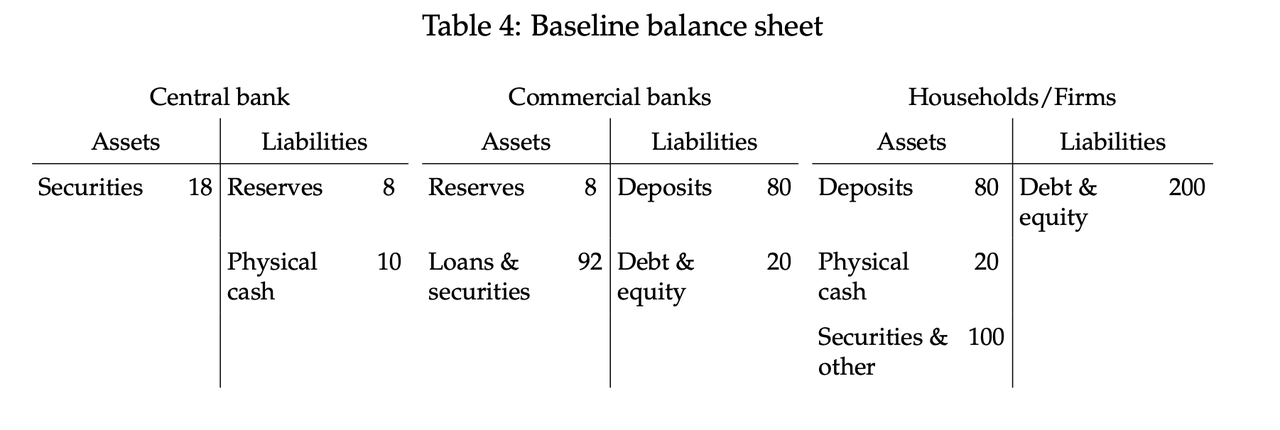

In our scenarios, we consider the impact of one or more statutory reserve-supported stablecoins being widely adopted in a stylized version of the banking system. The baseline balance sheet of the banking system is shown in the figure. Specifically, we consider households and businesses substituting $10 for cash, commercial bank deposits, or securities, and then we perform accounting work to determine how the adoption of stablecoins affects the balance sheets of the central bank, commercial banks, and households and businesses. We analyze how this impact varies depending on the stablecoin reserve framework and the source of the inflows.

It is important to note that in constructing these scenarios, we made several key assumptions. First, we do not know the specific form of the adopted stablecoin. Our scenarios are not intended to analyze the specific impacts of widely adopting existing stablecoins, such as Tether. We do not differentiate between the adopted stablecoins being institutional tokenized deposits, stablecoins circulating on public blockchains, or other forms. Second, we only show illustrative advantage cases. In reality, stablecoins can see multiple sources of inflows and hold multiple assets as reserves. Third, these scenarios do not capture secondary chain reactions or feedback loops, nor do they address heterogeneous impacts within the industry. Finally, we assume a 10% statutory reserve requirement for traditional commercial bank deposits.

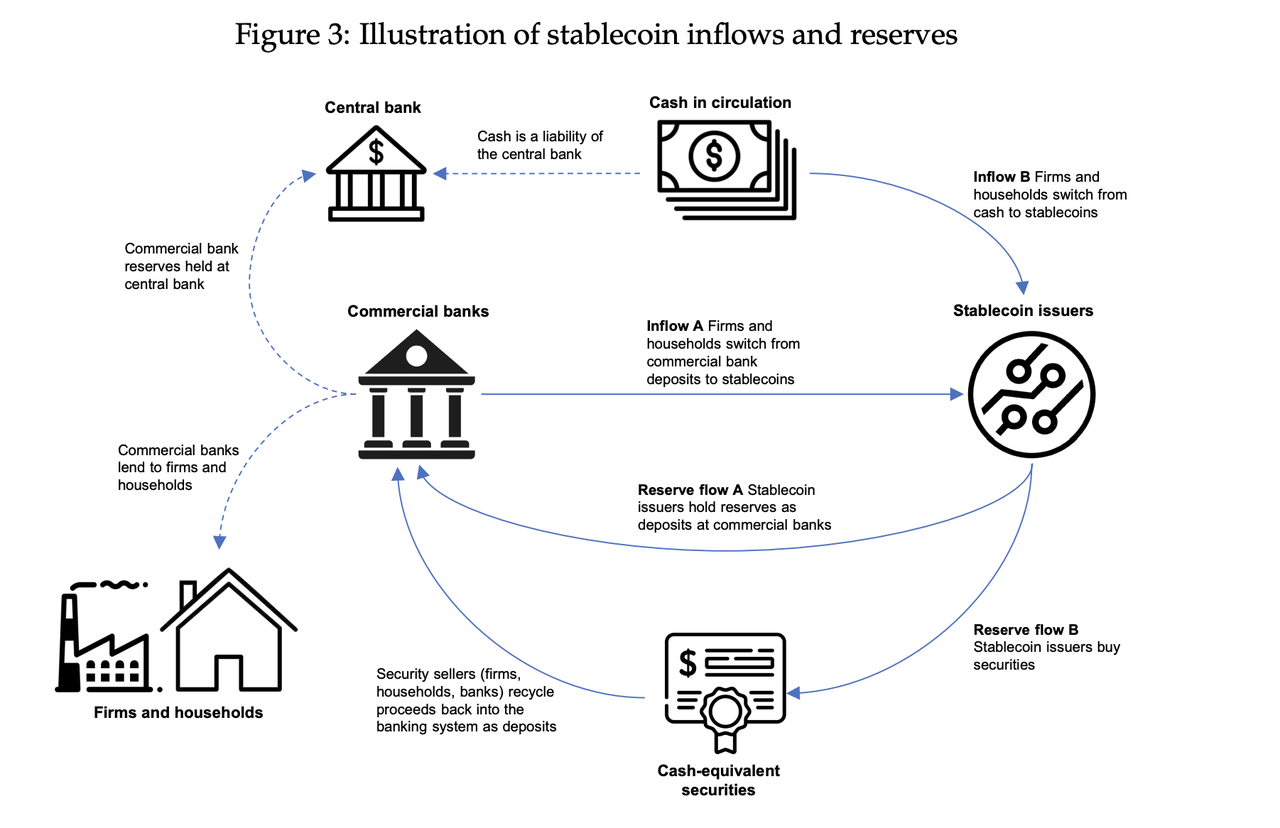

To illustrate the complex flows between the parts of the banking system in our edge-case scenarios, we visualize a subset of the stablecoin inflows and reserve allocations we discussed in the figure. Specifically, we use the chart to show how commercial bank deposits (inflow A) and cash (inflow B) flow into stablecoins, as well as how these funds are allocated as commercial bank deposits (reserve flow A) and securities (reserve flow B).

In the figure, we see how stablecoin inflows and reserve flows are interconnected. Companies and households substitute stablecoins for deposits (inflow A) and cash (inflow B). Stablecoin issuers hold part of the funds as commercial bank deposits, as reserves (reserve flow A), and use these funds to purchase securities as reserves (reserve flow B). These security purchases will also cycle funds back into the banking system, as the sellers of the securities eventually receive the proceeds from the sale of the securities and deposit them back into the banking system. As shown in the figure, these flows affect the central bank, which maintains cash and central bank reserves as liabilities, as well as companies and households that obtain loans from commercial banks. Although this figure does not capture all the flows between these entities, it symbolizes how the widespread adoption of stablecoins reshuffles complex financial relationships within the banking system.

Scenario Analysis

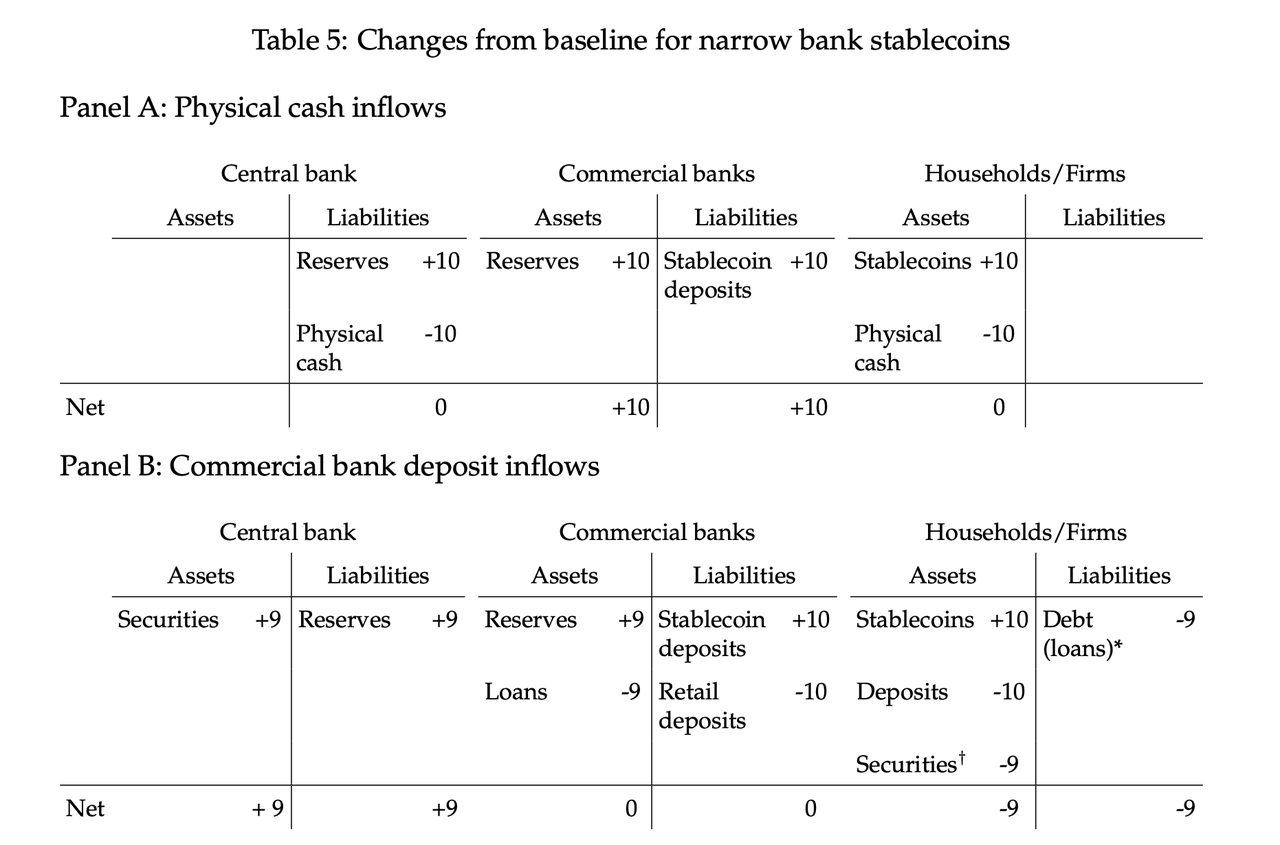

Narrow Banking Framework:

As discussed earlier, the narrow banking framework poses the greatest risk to credit provisioning, depending on the source of the inflows. In our narrow banking scenario, as shown in the table, we found that the inflow of physical cash into narrow banking stablecoins would have a neutral impact on credit provisioning, while commercial bank deposits would disrupt credit provisioning.

In Panel A (cash inflow scenario), we see that stablecoins have replaced cash on the balance sheets of households and companies. The inflow of cash leads to an indirect increase in the balance sheets of commercial banks and their reserves. The central bank's balance sheet is restructured, with reserve liabilities replacing cash liabilities. The net effect is an expansion of the commercial bank's balance sheet, but there is no change in credit provisioning. This scenario assumes that banks are not constrained by the size of their balance sheets. That is, narrow banking deposits and the associated reserve holdings are exempt from leverage ratio calculations. This leverage ratio exemption for central bank reserves has been adopted by regulators in different jurisdictions.

Panel B shows the narrow banking scenario where deposits migrate to stablecoins. Since stablecoin deposits are completely retained on the balance sheets of commercial banks, banks must reduce their asset holdings to accommodate the decline in non-stablecoin deposit funding. The central bank's balance sheet then expands to accommodate the increased demand for reserve balances, without offsetting the decline in cash liabilities. In this case, we assume that the central bank will meet the increased reserve demand by purchasing securities. This assumption of central bank easing was proposed by the Federal Reserve in previous rulings on narrow banking, as mentioned above, related to Regulation D: Reserve Requirements for Depository Institutions (2019). However, if the central bank determines its balance sheet size, we present two alternatives in Appendix Table A1. In the first alternative, commercial banks significantly contract their balance sheets to compensate for the shortage of deposit funding. In the second case, commercial banks compensate for the loss of deposit funding by issuing debt securities. The result is a further reduction in bank-dominated credit creation.

We did not imagine scenarios where narrow banking stablecoins see large inflows from securities holdings. In such cases, the impact on credit provisioning could be neutral. Under the same assumptions as above, the central bank meets the increased reserve demand by purchasing securities from households. The net impact on credit supply should be minimal. Unlike direct security holdings, the migration to stablecoins would allow households to own stablecoins backed by central bank reserves, which in turn are backed by securities. This scenario also assumes that the increased narrow banking reserves are not subject to leverage ratios, as mentioned above.

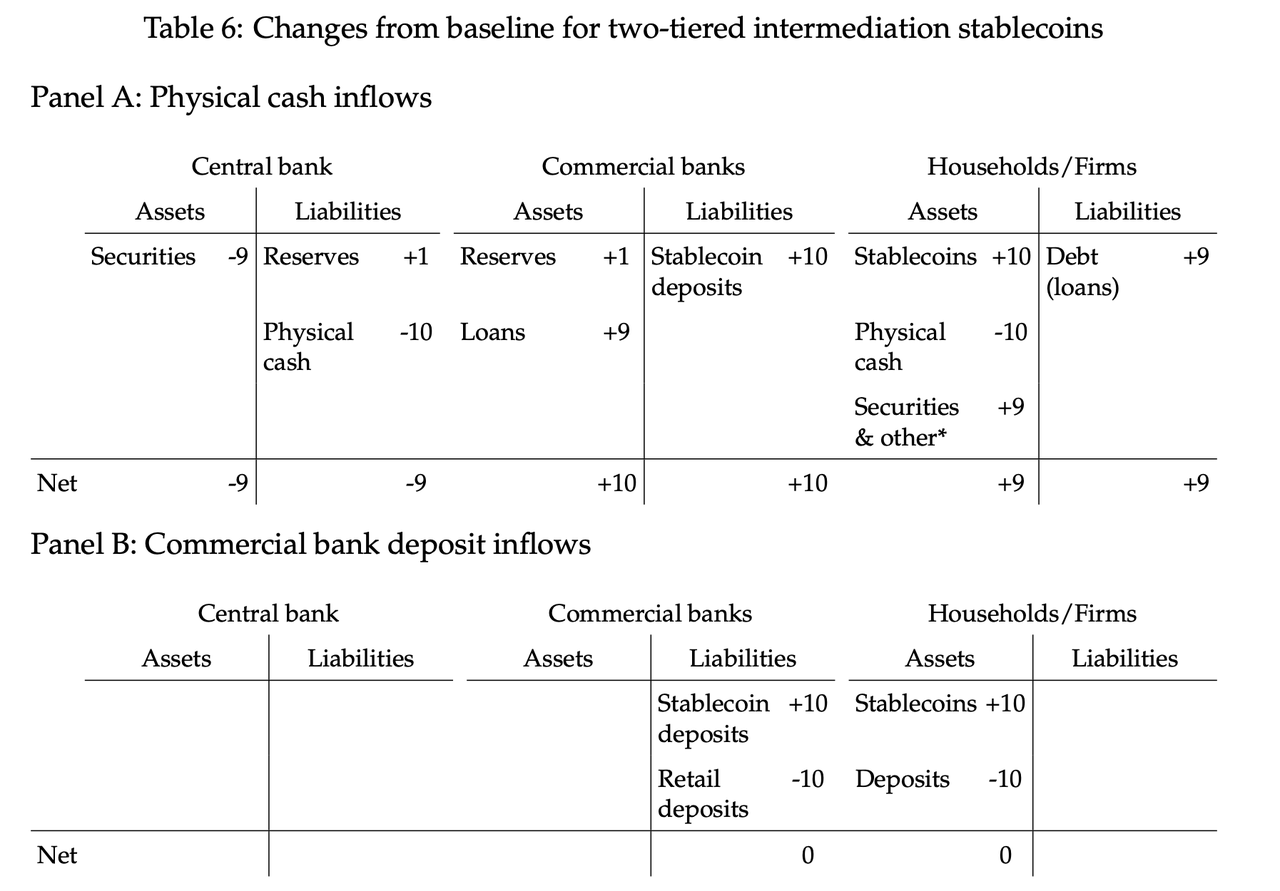

Two-Tier Intermediation Framework:

For the two-tier intermediary framework shown in the following table, we found that a large inflow into stablecoins would have a neutral to positive impact on credit provisioning. Panel A shows the scenario where cash is converted into stablecoins. As commercial banks engage in fractional reserve banking with stablecoin deposits, their balance sheets expand as they increase credit and security holdings, which accounts for most of the expansion. The central bank's balance sheet contracts on a net basis, with a slight increase in reserves and a significant decrease in cash liabilities. Households accumulate more assets, expanding the funding provided by bank loans. The impact on credit provisioning is positive. Panel B shows the two-tier intermediary scenario with deposit substitution. The total balance sheets and asset holdings of commercial banks and the central bank do not change. The only change is the composition of commercial bank liabilities, as time deposits are converted into stablecoin deposits. As mentioned earlier, this scenario assumes that the treatment of stablecoin deposits is the same as non-stablecoin deposits in terms of statutory reserve requirements, liquidity coverage ratios, and other regulatory and self-imposed risk limits.

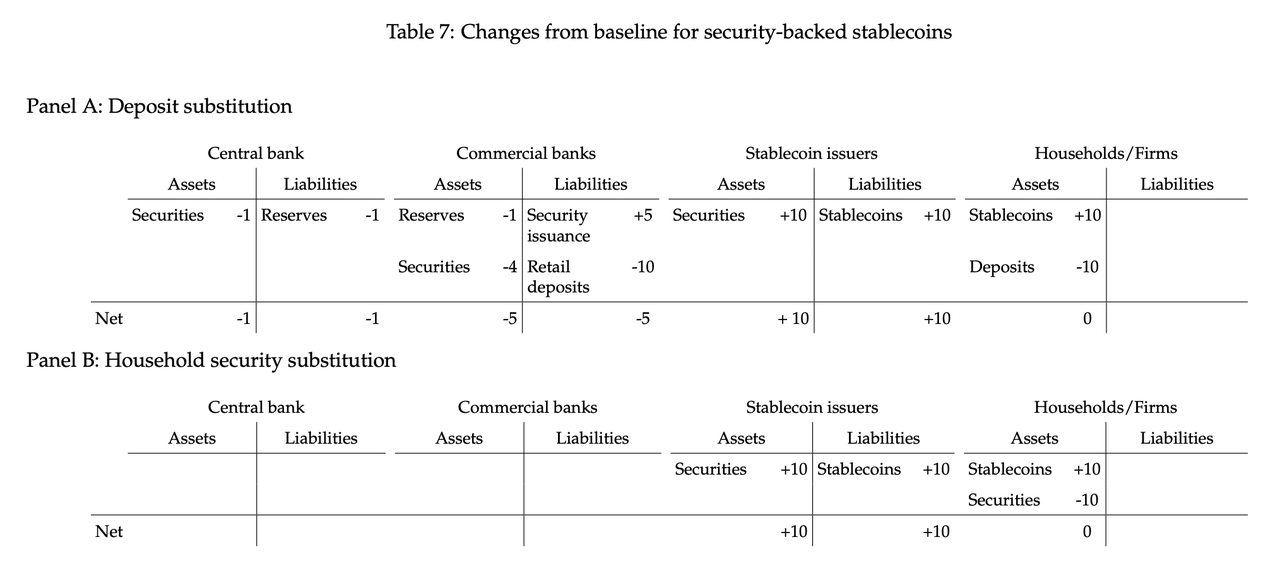

Security Holding Framework:

As shown in the following table, the impact of widespread adoption of security-backed stablecoins is the most unpredictable. Many scenarios are possible. In Panel A, we present a scenario where security-backed stablecoins see inflows from commercial bank deposits. We assume that stablecoin issuers purchase securities from commercial banks rather than from households and corporate sectors. In this case, as households convert deposits into stablecoins, commercial banks compensate for the loss of deposit funding by issuing their own securities. Additionally, commercial banks can reduce their securities portfolios to compensate for the loss of deposit funding. If banks adjust the asset side of their balance sheets primarily by changing their securities holdings, the size of their loan portfolios may remain unchanged. In this case, the central bank's balance sheet also slightly contracts due to the loss of bank reserves.

Panel B shows the scenario where households convert their cash equivalents into stablecoins. This will result in the effective tokenization of near-cash securities without directly affecting the credit supply in the banking system. We also consider another scenario (not shown) where security-backed stablecoins experience inflows from household and corporate sectors' deposits while selling securities to commercial banks. The sellers of the securities are households and corporate sectors, not commercial banks as described in Panel A of Table 7. The net impact on credit supply is neutral, as the commercial bank deposit balances held by households and corporations who purchase stablecoins are ultimately recycled back into the banking system by transferring them to other households and corporations that sell securities to stablecoin issuers. This restructuring of securities holdings is illustrated in Figure 3 through inflow A and reserve flow B. The final result is balance sheet changes, identical to those in Panel B.

Finally, we did not describe scenarios where security-backed stablecoins see inflows from physical cash. However, this could have a neutral or positive impact on credit creation. If stablecoin issuers use physical cash to purchase existing securities, and these physical cash are not deposited into the banking system, this will not affect credit supply, as it constitutes a direct exchange of cash for securities. However, if the physical cash used to purchase existing securities is deposited into the banking system, or if these physical cash are used to fund the issuance of new securities, this could increase credit supply by increasing commercial bank loans and securities purchases, or by lowering the equilibrium cost of issuing securities. In summary, the potential impact is a moderate increase in credit supply.

Summary

As digital assets gain broader adoption and the use cases of programmable digital currencies become clearer, stablecoins have grown significantly over the past year. This rapid growth has raised concerns about potential negative impacts on banking activities and the traditional financial system. In this report, we discuss the current use cases and potential growth of stablecoins, analyze historical events of peg instability, and illustrate different scenarios of the impact of stablecoins on the banking system. As mentioned in the introduction, this paper does not consider all potential impacts of stablecoins on financial stability, monetary policy, consumer protection, and other important unexplored issues. We focus on balance sheet effects and credit intermediation under a series of reasonable assumptions.

We studied reserves-supported stablecoins and found that the impact of stablecoin adoption on traditional banks and credit provision may vary depending on the source of inflows and the composition of stablecoin reserves. In various scenarios, the two-tier banking system can support the issuance of stablecoins while maintaining traditional forms of credit creation. In contrast, the narrow banking stablecoin framework can provide the greatest stability but may carry potential costs of credit disintermediation. Finally, if USD-pegged stablecoins have sufficient collateral, they can serve as a safe haven during market distress compared to other cryptocurrencies.

Original Title: "Stablecoins: Growth Potential and Impact on Banking"

Original Author: Gordon Y. Liao and John Caramichael

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

Popular Airdrop Tutorial

Selected potential airdrop opportunities to gain big with small investments

FusnChain

FusnChain