Arthur Hayes on Why He Dumped HYPE: The Triple Pressure of AI Bubble, Oil Prices, and the Election

Arthur Hayes on Why He Dumped HYPE: The Triple Pressure of AI Bubble, Oil Prices, and the Election

BlockBeats Note: Last week, Arthur Hayes posted on social media that he had liquidated all positions in HYPE and NEAR, stating he would elaborate on the rationale in this article—this is precisely that follow-up.

His core arguments are as follows:

· Escalation in Iran's situation combined with corporate inventory restocking cycles could drive further increases in energy prices

· Three major AI projects are expected to go public from now until early Q3

· Trump may pivot to an anti-AI stance before the midterm elections to secure broader Republican voter support

· The current market peak is most likely to occur between now and September

· For risk asset investors, it’s now time to gradually take profits. Below is the original text:

Is all of this my delusion, or has investing in AI today simply become a matter of subscribing to Citrini Research and blindly buying every stock they recommend?

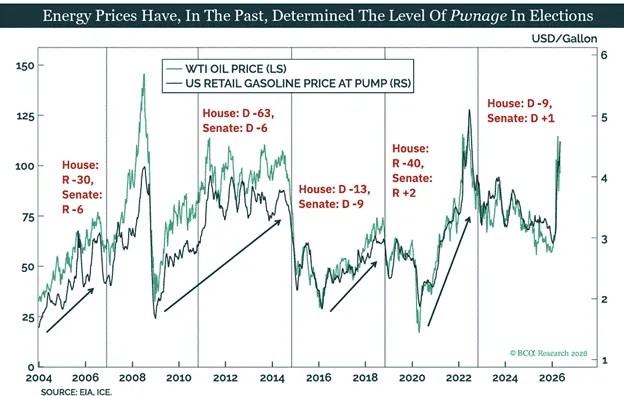

Am I dreaming, or has oil price already lost its influence over economy and politics? That’s why Trump and Iran’s Islamic Revolutionary Guard Corps can engage in online sparring without consequence, while countless vessels remain stranded in the Strait of Hormuz.

Two-year U.S. Treasury yields are 0.5 percentage points above the effective federal funds rate—a clear market signal. Will the Fed really remain passive and refrain from hiking rates at the upcoming FOMC meeting?

Will the entire benefits AI brings to the U.S. truly be captured only by a select few tech professionals?

This chaotic world demands a reality check: am I lucid, or still trapped in a dream? If the test proves everything is illusory, I’ll immediately rebalance my portfolio. This article documents my reality test. Once these words are typed and thoughts sorted, my position will undergo significant change—or remain unchanged.

I’ll state my central conclusion upfront: the current market state resembles a dream. Within the investment system, oil and other hydrocarbon energy prices are the pivotal variables with reverse transmission effects. Human perception of the world fundamentally involves converting energy into biological intelligence—the same logic applies to AI. This law never breaks. Markets may temporarily deviate from this truth, but reality will eventually exact its revenge.

This piece begins with oil prices and ends with the U.S. election. The current situation may trigger a collapse of the AI stock bubble, dragging down the entire crypto market alongside.

Only after the dust settles will Bitcoin have a chance to bottom out and rebound. I previously declared Bitcoin would never touch $60,000 again—my judgment was clearly wrong, which is typical of market forecasting. I’ve always adhered to one principle: opinions can be strong, but not dogmatic.

Now let’s dive into analysis.

Whether Negotiations Happen: The Core Dilemma Today

Politicians always act in self-interest. Trump’s unprovoked military action against Iran remains shrouded in mystery—only he knows the real reasons. With his team constantly releasing contradictory statements, outsiders cannot discern the truth. Now that events have unfolded, debating causality is pointless. The real issue is whether Trump and Iran’s Islamic Revolutionary Guard Corps will choose to cease hostilities—and how.

The conflict is now entirely driven by Trump. For him and the Republican camp, sparking war during an election year is strategically disadvantageous.

In the U.S., prices of essentials like gasoline and food often determine election outcomes. With maritime traffic through the Strait of Hormuz obstructed, energy and food inflation continue rising—entirely due to Trump’s government’s unilateral decision to launch an attack on Iran without public consultation. Some blame Israel, but that’s baseless. Anyone familiar with American history knows domestic forces never bow to external dictates.

Americans generally tolerate foreign wars as long as their daily lives aren’t disrupted and no loved ones are harmed. Trump repeatedly emphasized only thirteen U.S. soldiers died in this special military operation. This explains America’s preference for high-precision remote weapons and “game-like” warfare.

Even if this Middle East conflict lacks a clear winning strategy and contradicts many supporters’ expectations, Trump’s base still stands firmly behind the GOP. Some Republican lawmakers were pressured and defeated within their party due to wavering stances—proof of this loyalty.

Trump’s real vulnerability isn’t that his base won’t vote in November—it’s that soaring prices will push large numbers of swing voters toward Democrats. Cost-of-living issues have become his biggest electoral challenge.

To win back swing voters, Trump must stabilize current oil prices. Supply chains are just beginning to digest the pressure from rising energy and raw material costs—containing inflation altogether is unrealistic. What Trump can do now is only manage market expectations of inflation, not alter inflation itself.

Whether Trump agrees to a deal with Iran depends entirely on oil price trends.

As oil prices keep climbing, his tone becomes more conciliatory; but if markets anticipate negotiations and oil prices fall accordingly, he quickly reverses course. After all, from a geopolitical standpoint, any agreement reached now would likely be more disadvantageous than Obama-era deals with Iran. To many voters, this equals defeat—and the GOP would pay dearly in elections.

Negotiations require mutual concessions. Iran’s Revolutionary Guard also weighs similar calculations. High oil prices pressure Iran’s key trading partners to push for concessions; but once Iran signals willingness to negotiate and oil prices drop, that pressure eases.

At current oil levels, neither side has incentive to retreat. While prices have risen significantly since pre-conflict levels, they haven’t yet triggered full-scale crisis. Commodity markets remain stable globally, no mass famines have occurred, and most nations can source critical industrial inputs elsewhere.

But this delicate balance cannot last. A massive reduction in global core energy supply with persistently calm prices defies market logic.

Once global idle capacity is exhausted, spot prices will inevitably surge—this consensus among commodity analysts. The crisis hasn’t erupted fully yet only because pre-war global energy inventories were substantial.

If the stalemate continues into late Q2, spot prices for hydrocarbons and basic commodities in Q3 will face a massive spike.

As Churchill said: politicians exhaust every option before making the right choice.

Only when the situation spirals completely out of control will Trump and Iran finally sit at the negotiating table. In my view, the blockade of shipping through the Strait of Hormuz will likely persist into early Q3.

Let’s suppose oil prices rise gradually amid volatility. How will this trend interact with Trump’s campaign rhetoric?

November Election Showdown: Republicans vs. Democrats

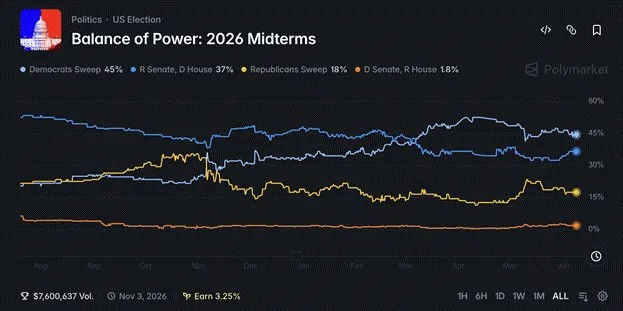

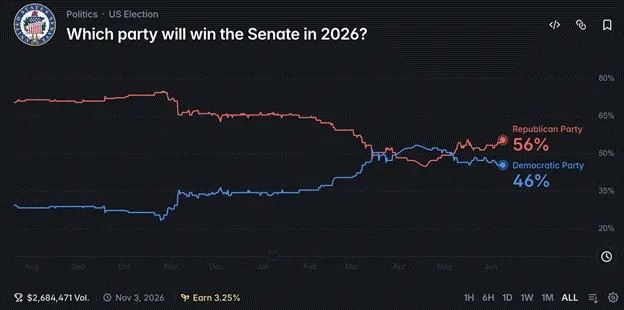

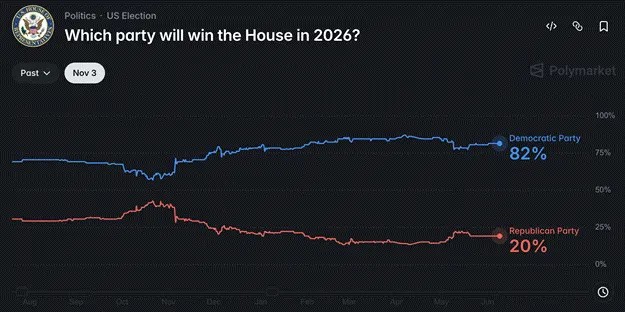

According to prediction markets like Polymarket, Republicans currently hold only a slim edge in retaining Senate control, but will suffer heavy losses in the House.

Most assume Republicans will lose the House—but I disagree. Trump still has a comeback opportunity, and the key lies in shifting public discourse toward data center expansion and regulatory/tax measures targeting the AI industry.

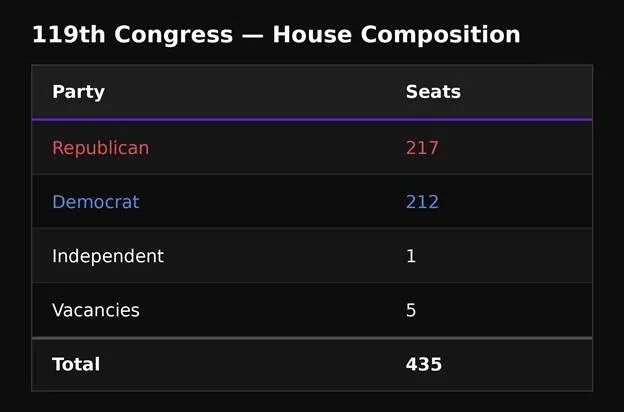

Current party seat distribution (a bill requires 218 votes):

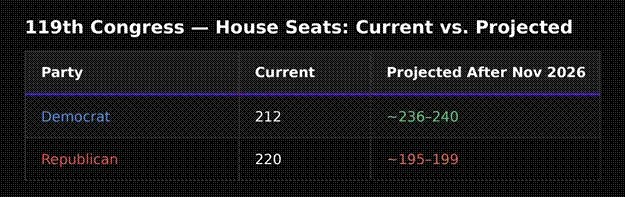

Based on Polymarket’s current odds, here’s the projected post-election party composition:

Republican prospects in both chambers look bleak post-election. But redistricting could shift the outcome. When rules guarantee defeat, changing them becomes inevitable. Assuming Polymarket’s forecast is correct, Republicans need 19 additional seats. Redistricting could reduce that number.

Potential impact of redistricting:

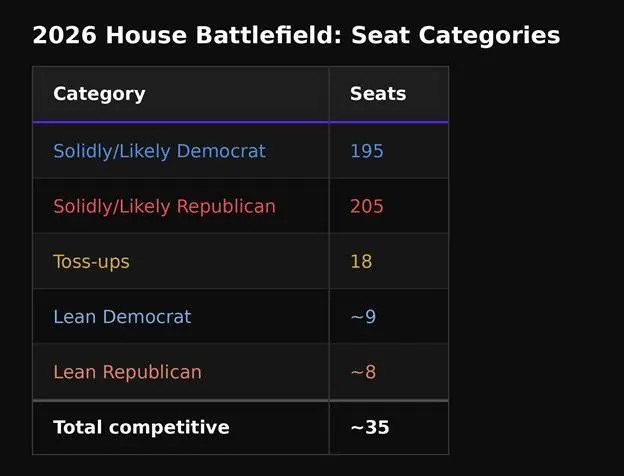

Republicans now need only 11 more seats.

Next, let’s examine battlegrounds. Based on current polling, which districts might slightly favor Republicans within margin of error?

Thirty-five seats remain highly uncertain. As mentioned earlier, elevated inflation and rising living costs are Trump’s persistent negative narratives. Another issue equally resonant across both parties today is data center expansion and AI’s impact on employment.

Aside from ultra-wealthy elites, nearly everyone fears data center construction driving up costs and worries AI will displace jobs. Many regions have paused new data center projects, demanding higher taxes on AI firms and increasing calls for subsidies to ordinary citizens. After all, most people aren’t executives or high-paid workers at AI companies.

For voters in competitive districts, such issues carry immense weight. Trump can win remaining key seats by making public statements about regulating the AI sector. At this stage, mere rhetoric suffices—no concrete legislation needed. He simply needs to promise, if elected, he’ll tackle AI regulation shortly after the election.

As a seasoned politician, Trump excels at making campaign promises rarely fulfilled afterward.

Consider his handling of Epstein-related archives: he loudly vowed a full investigation during the campaign, but after taking office, only released minimal documents. He can repeat this pattern now—campaigning on plans to slow data center expansion, impose windfall taxes on AI firms, and use proceeds to fund new relief payments. Once the election concludes and the GOP secures power, he can gradually retract those statements.

Some may find it odd that Trump adopts tactics reminiscent of progressive Democrats. But remember: he launched the largest universal relief program since the New Deal—even when low-income recipients spent aid on daily consumption, he imposed no restrictions.

To preserve his political standing, temporarily distancing himself from AI giants like Elon Musk and cultivating a populist image poses no difficulty for Trump.

If Trump indeed makes hardline statements against the AI industry, markets won’t dismiss them as mere campaign rhetoric—they’ll interpret it as genuine intent to materially restrict capital expansion in AI and increase industry taxation. Panic will spread instantly, triggering the collapse of the AI stock bubble.

Earlier, Elon Musk and Trump publicly clashed on social media, with Musk’s affiliates questioning Trump, prompting immediate retaliation—Trump announced he’d cancel government contracts with Musk’s companies. Tesla’s stock dropped 18% in a single day, revealing market sensitivity to such turmoil. Politics can boost industries overnight—or destroy them.

That dispute was later revealed to be orchestrated propaganda; the two reconciled quickly, and Musk even attended a recent summit between Trump and China’s national leader in Beijing.

Yet at the time, markets believed it—and triggered massive sell-offs.

This was merely a private feud. Should Trump formally declare, on behalf of the GOP, plans to impose heavy taxes on AI models and intelligent agent operations, the fallout would far exceed previous incidents. When South Korea’s officials floated similar ideas, the local composite index nearly hit a daily limit down, only recovering after official denial.

Current market optimism in AI stocks rests on assumptions that industry revenues will grow exponentially, and that technological advances and wealth concentration won’t spark public backlash. Such thinking is detached from reality—more akin to a dream.

Trump’s statements will serve as the reality check that punctures the illusion. Whether he actually acts depends ultimately on oil prices.

Continued Iranian tensions pushing oil prices up intensify inflation, reducing Trump’s available campaign talking points. Ultimately, he’ll have no choice but to target data centers and the AI industry.

Trump’s intense aversion to a Democratic-controlled House is clear. If Democrats gain control, they can exercise subpoena power, summoning Trump, his family, and inner circle for testimony, asking sharp questions. If Democrats retake the White House in 2028, a Justice Department armed with evidence could initiate a reckoning, launching investigations into Trump’s business entities.

Let’s trace the logic chain: prolonged failure to resolve U.S.-Iran tensions will drive oil prices up; rising prices fuel voter discontent, forcing Trump to leverage AI regulation and taxation to win votes.

Even if AI-related stocks halve in value from now until November, Trump may accept it as a cost to escape endless Democratic investigations. Post-election, he can easily retract prior statements on data centers and AI, allowing the industry to return to normal—S&P 500 could even surge toward 10,000.

But for investors, market dynamics are interlinked. A crash in the AI sector will permanently alter expectations for future returns. After enduring regulatory crackdowns and heavy taxation, investors can no longer blindly favor this space.

California Dream: Where Is Liquidity Flowing?

Before analyzing the impact of SpaceX, Anthropic, and OpenAI’s planned IPOs on global financial markets, let me address a question: since late Q3 last year, U.S. dollar liquidity has remained loose, yet Bitcoin didn’t rally in tandem—why?

On November 30, 2022, ChatGPT launched to the public, marking the start of the AI superbubble. Almost simultaneously, the FTX founder SBF’s scandal over misappropriating user funds was exposed. Bitcoin, which touched around $15,000 that year, climbed to $125,000 by October 2025—a gain exceeding sixfold.

Meanwhile, Nvidia’s stock surged elevenfold. Numerous mid-cap tech stocks reliant on compute power and electricity-to-intelligence conversion also exploded. AI’s performance vastly outpaced crypto, and the gap has widened since late 2024.

Following my traditional logic based on fiat liquidity, Bitcoin should have seen even greater gains under current conditions—yet reality is the opposite. Where did I go wrong?

I used to focus solely on total fiat money creation, overlooking where the funds actually flowed. I assumed liquidity would eventually flood into Bitcoin, pushing prices up—this time, my assessment was flawed.

My conclusion: newly created U.S. dollar liquidity has been almost entirely absorbed by the AI sector. AI is a capital-intensive industry. Building massive data centers capable of running AI requires enormous energy consumption. Hydrocarbons, nuclear, and renewable sources convert into electricity, delivered to data centers where specialized chips train and infer models.

Since 2024, global data center CAPEX has surged, accelerating further in 2025. Financing demand has skyrocketed. Combining disclosed data, total debt financing in AI-related fields reached $1.5 trillion from November 2022 to present—coincidentally matching the increase in U.S. broad money supply M2.

The answer is clear: all new dollars flowed into AI. Bitcoin naturally received none of the incremental funding.

Bitcoin’s strong rebound from FTX’s collapse in 2022 occurred because large-scale AI debt expansion primarily began after 2025. Of the $1.5 trillion in debt, $1.3 trillion was issued in 2025 alone.

Coincidentally, Bitcoin’s peak price coincided with October 2025—when AI CAPEX reached unprecedented levels.

This correlation is crucial. Once the AI stock bubble bursts, there will be no excess capital left to deploy in Bitcoin.

Banks will tighten lending. Many institutions will realize loans based on inflated revenue data pose huge risks. When top tech stocks plunge over 50%, bank credit officers will worry about default risks, leading to credit contraction and tighter overall market liquidity. Combined with growing political hostility toward AI, the industry will struggle to attract rescue funding in the short term.

Even if governments step in to rescue financial institutions, such measures are likely to come only after the November election.

The link between Bitcoin and AI stock prices forces us to decide: does the AI stock bubble exist? When will it burst? And what triggers it?

AI Bubble: Three Deadly Strikes

Three factors will pop the current AI bubble: rising energy costs, market inability to absorb the massive fundraising from SpaceX, Anthropic, and OpenAI, and Trump’s potential anti-AI policy announcements.

The core logic of AI is maximizing efficiency in “energy-to-intelligence” conversion. Humans derive intelligence from consuming food; AI relies on electricity. Currently, most new data center power comes from natural gas and other hydrocarbons.

Rising energy prices mean higher operating and compute output costs for AI—directly squeezing profit margins at Google, Anthropic, OpenAI, and others.

Higher costs lead companies to raise service prices, slowing user adoption of compute and models. Ongoing geopolitical tension between the U.S. and Iran keeps oil prices rising, steadily eroding AI firms’ profitability. When skepticism grows about the rationality of continued data center expansion, the industry turn arrives—expectations for forward P/E ratios shrink dramatically, and bear markets begin.

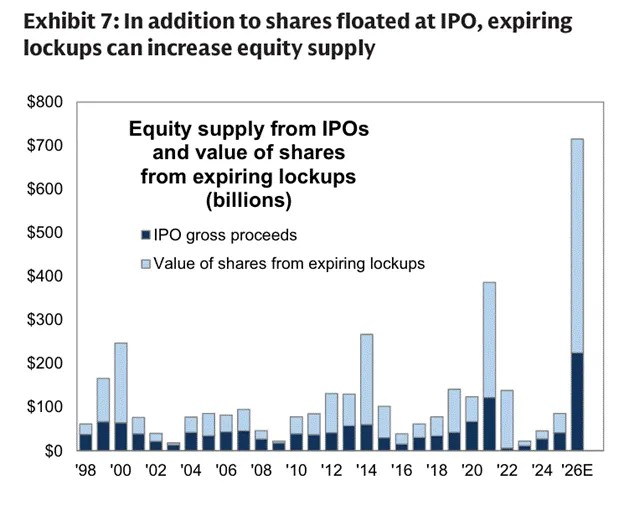

Moreover, restricted shares from SpaceX, Anthropic, OpenAI, and other tech firms are gradually unlocking, compounded by massive IPOs. Total fundraising could surpass the cumulative total of all new issues during the dot-com bubble—unprecedented scale. Can the market absorb such massive selling pressure? Highly doubtful.

Recent AI sector gains rely on investor belief in sustained accelerated growth. Once doubts emerge, investors lower future earnings valuations. These giants’ IPO performances will become sentiment barometers. If underperforming, investors will conclude the sector has peaked, triggering collective sell-offs.

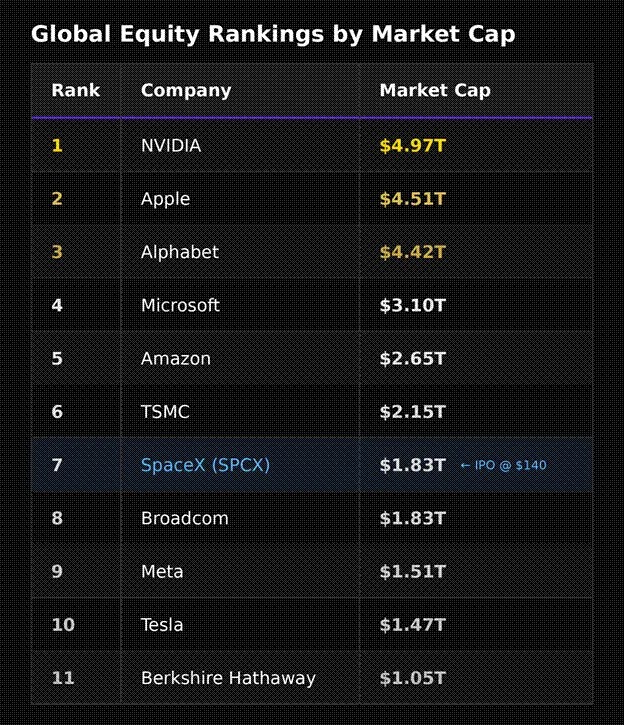

Taking SpaceX as an example—information disclosure is relatively complete. Capital markets follow the rule: “first movers win.” Elon Musk understands marketing well; going public first allows maximum cash-out for the company and early shareholders. Crypto participants understand this model intuitively: extremely low circulating supply, fully diluted valuation remains sky-high—similar to some meme coins.

According to SpaceX’s SEC filing, the IPO valuation reaches nearly 100 times revenue. More critically, the company initially releases only 4% to 5% of shares. Given current AI hype, the stock will likely surge on Day One—but such high expectations mean subsequent performance struggles to meet investor imagination.

Post-IPO, SpaceX’s market cap will reach $1.8 trillion, ranking seventh globally. If shares rise another 50%, it would surpass Amazon to become fifth—yet its profitability can’t justify such a tier.

Nvidia sustains high valuation through solid gross margins and revenue scale. SpaceX focuses on space-based data centers—analysts note construction and operational costs are four times higher than ground-based facilities, with cost parity expected only in a decade.

If initial valuation were more rational, subsequent price movement would be steadier. Crypto veterans know the logic: if secondary market investors can’t profit, unlocked insider shares will find no buyers—prices will only decline.

Looking at share unlock timelines: from now to early September, SpaceX’s free float will expand fivefold—massive share supply flooding the market, creating immense upward pressure. Worse, Anthropic and OpenAI plan to go public in September—both targeting trillion-dollar valuations.

Between June and September, SpaceX might see brief upside, but when three hyper-valued companies list simultaneously with massive new supply, disappointment will spread. Investors expect explosive rallies—not modest upticks.

Overall, rising energy costs, concentrated mega-IPOs, and Trump’s regulatory rhetoric create three adverse shocks. These companies’ IPO performances will likely fall short of expectations. Once investors no longer believe AI firms can maintain exponential profit growth, sector valuations will be reset downward—stocks collectively weaken.

Currently, AI stocks are heavily leveraged via margin loans. Banks have provided massive credit for industry expansion. After a sector crash, banks will face massive bad debts.

In a global AI bubble burst and broad risk asset selloff, Bitcoin will struggle to decouple in the short term. Only after full market clearing will Bitcoin bottom out first. Then, to rescue the economy, we’ll see another round of massive monetary easing—Bitcoin will rebound. But for now, preserving capital is paramount.

Before sharing Maelstrom Fund’s equity and crypto holdings strategy, let’s analyze the Fed’s monetary policy trajectory.

Fed Chair’s Dilemma

New Fed Chair Kevin Warsh now faces a delicate situation. Public evaluations of his style vary widely—depending entirely on how he handles the Fed’s current contradictions.

Trump nominated Warsh to chair the Fed hoping he’d push rate cuts. Warsh previously signaled that inflation from geopolitics is temporary, while AI-driven productivity gains are long-term—justifying rate reductions.

But the market sent the opposite signal. Two-year Treasury yields exceed the effective federal funds rate by 0.5 percentage points—indicating markets believe, given sustained inflation, the Fed should hike at the June 16–17 FOMC meeting, not cut.

At present, holding rates steady is the most probable outcome. But markets will scrutinize the post-meeting press conference and adjustments to reserve management. Even inaction will be parsed as hawkish or dovish.

Hawkish rate stability equates to tightening. On one hand, unresolved U.S.-Iran conflict drives oil prices up; on the other, three AI giants concentrate IPOs, pressuring supply. Multiple headwinds converge—every risk asset faces correction.

The worst case: Trump instructs Warsh to hike immediately per market demand, trying to suppress prices for voter appeal. But unless the Fed hikes sharply while actively selling bonds to shrink balance sheets, it still can’t keep pace with inflation. This mirrors the 1970s: aggressive Fed hikes failed to curb inflation.

Under current conditions, Fed rate cuts are virtually impossible. Whether the Fed hikes or holds steady, markets will interpret it as tightening liquidity—further undermining AI sector bulls.

Combining all elements, rising oil prices will eventually become a broad risk asset headwind. Now let’s discuss Maelstrom Fund’s specific portfolio positioning.

Portfolio Positioning

All worldly systems run on energy. Given our expectation of rising energy prices, allocating to energy assets is inevitable.

Currently, U.S.-Iran deadlock persists. Shipping through the Strait of Hormuz remains blocked—daily crude and natural gas supply losses accumulate. Market sentiment remains calm, but if this standoff continues, rising energy prices become unavoidable.

Industry data from multiple sectors point to the same conclusion: geoeconomic conflict has driven global energy inventories to multi-year lows, continuing to decline. Once below critical thresholds, the entire energy supply system falters—prices spiral uncontrollably.

Even under the best-case scenario—immediate ceasefire, normal shipping resumed—countries will still increase procurement for restocking and strategic reserves, pushing oil prices higher.

Assessing both scenarios, oil and gas prices will trend upward over the next three to six months. Regardless of temporary pullbacks after short-term peace agreements, the medium-to-long-term uptrend is confirmed. Thus, we’ve aggressively positioned in U.S.-listed energy producers.

Energy exposure offers upside potential across all scenarios, and current valuations are more favorable compared to energy-dependent tech sectors. Conversely, assets relying on cheap energy to sustain high valuations now face grim prospects.

With oil reaching $150/barrel, AI’s past strength will be unsustainable. Therefore, we’ve liquidated all AI-related equities.

Previously, capital flooded into AI stocks. Once this sector crashes rapidly, even crypto’s relative resilience won’t attract inflows. Thus, we reduced all non-core cryptos—sold HYPE, NEAR, WLD last week—and cleared ZEC due to Orchard Pool vulnerabilities. Preserving principal outweighs chasing gains now.

Our current holdings retain only Bitcoin and Ethereum. Ethereum has no urgent need for large-scale monetization, so we continue holding. I firmly believe the AI bubble burst will trigger another financial crisis—global monetary easing will resume, Bitcoin will dip first then rally.

Amid market turbulence, we’ll maintain core positions long-term while using derivatives for short-term bearish trades—capturing tactical opportunities. After all, I don’t want to give up the thrill of trading.

If reality turns out completely different from my judgment—proving it was all a false alarm—no harm done. Taking profits before heading to the Mediterranean is a prudent choice. I’ll reassess market trends and prior judgments by early September, then opportunistically re-enter positions.

Differing from institutions requiring fixed annual payouts, Maelstrom Fund prioritizes long-term compound growth—giving us ample room to navigate the blurred lines between reality and illusion in the market.

Original: BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

5-Second Breakthrough with Just 1 Interaction: Has the "Strongest Security Mechanism" of Claude Fable 5 Been Cracked by a Chinese Team?

20 hours ago

Why Is the "AI Service Subscription Model" Inevitably Headed for Extinction?

23 hours ago

Managing a company valued at nearly a trillion dollars, Anthropic's CEO has only one direct report.

1 day ago

ERC-8126: A New Ethereum Standard for Issuing "Security Health Reports" to AI Agents

1 day ago

AI New Stars, $5,000/Hour Companionship Chatbots, Silicon Valley 2026 vs. Night City 2077

2 days ago

Interview with Instagram's Founder: Anthropic's Fable 5 Launches, Marking the End of the Era of Hand-Coded Development

2 days ago

After AI devours everything, what remains untrainable?

2 days ago