70% Bear Market Signals in the US Stock Market, Should You Exit?

70% Bear Market Signals in the US Stock Market, Should You Exit?

TL;DR

U.S. equity investors today face a situation that goes beyond simple bullish or bearish outlooks.

On one side, Bank of America’s U.S. Equity & Quantitative Strategies team, led by Savita Subramanian, released a client report titled “Too many red flags. Take profits.” on June 5. According to Axios reporting on June 9, the report identifies an excessive number of risk signals in U.S. equities and offers a more direct positioning recommendation: take profits.

On the other side, the AI fundamentals remain robust. Microsoft, Google, Amazon, and Meta continue increasing capital expenditures in AI and data centers, while NVIDIA’s data center demand remains the core anchor of the semiconductor cycle. Unlike the dot-com bubble of 2000, this round’s market leaders are now a group of giants with strong cash flows, profitability, cloud revenue, and chip order books.

Thus, the real question has shifted from “Is AI a bubble?” or “Is BofA calling the top?” to a far more complex one: How should investors interpret current U.S. equity risk when historical top signals coexist with genuine AI growth?

The answer may be more uncomfortable than outright bearish: The AI bull market may not yet be over—but it has transitioned from a “buy growth” phase into a “test growth execution speed” phase.

BOA Warns of Deteriorating Odds

The value of BofA’s report lies in placing the current market within a historical risk framework—not in predicting an exact top.

Multiple financial media outlets cited BofA’s research indicating that approximately 70% of its 10 bear market warning indicators have been triggered. This ratio is close to the historical average seen before S&P 500 peaks since 1990. BofA’s framework also shows that 17 out of 20 valuation metrics indicate statistical overvaluation, with 8 exceeding levels seen at the peak of the 2000 dot-com bubble. CAPE (Cyclically Adjusted P/E) or P/E10 is hovering around 40—near the historically extreme range.

Individually, these numbers can be contested. High valuations do not imply immediate downside. Historical signals being valid does not guarantee accuracy every time. Stronger profits among AI firms indeed make today different from 2000. But when valuation, market breadth, style divergence, and momentum all show extreme readings simultaneously, BofA’s core message becomes clearer: markets can still be held, but the odds have deteriorated.

Market breadth is key here. While indices remain high, gains increasingly rely on a narrow set of AI and tech megacaps. Current U.S. equities exhibit the characteristic of a historical top: limited leadership. A small number of stocks drive most index appreciation, the proportion of S&P 500 constituents above key moving averages has declined, and many individual stocks are not near their own highs. Strength at the index level masks declining internal participation.

Style divergence reinforces the same signal. BofA notes that the median return difference between the top quintile and bottom quintile of tech stocks is about 120 percentage points—the highest since 2000, approaching the 130-point gap observed just before the March 2000 peak. This reflects concentrated bets on a few high-conviction narratives rather than broad-based diffusion typical of a normal bull market.

For investors holding SPY, QQQ, NVDA, or SOXX, the danger of this structure lies in shrinking margin for error. Indices may still rise, but as returns become increasingly driven by a handful of stocks, any deviation in earnings, guidance, capital allocation returns, or valuation assumptions from a single leader could be amplified into a portfolio-wide drawdown.

AI Can’t Be Simplistically Compared to 2000

If one only considers BofA’s valuation and breadth signals, it’s easy to directly equate the current market to 2000. But this analogy is only half-right.

The hallmark of the 2000 dot-com bubble was the proliferation of companies lacking mature business models, with investors betting primarily on the narrative that “the internet would change everything.” Today’s AI leaders are different. Microsoft, Google, Amazon, and Meta have already embedded their cloud and AI operations into real revenues, capital expenditure plans, and data center demand. NVIDIA is not just a narrative hub—it is also a highly concentrated provider of profit and cash flow in the semiconductor space.

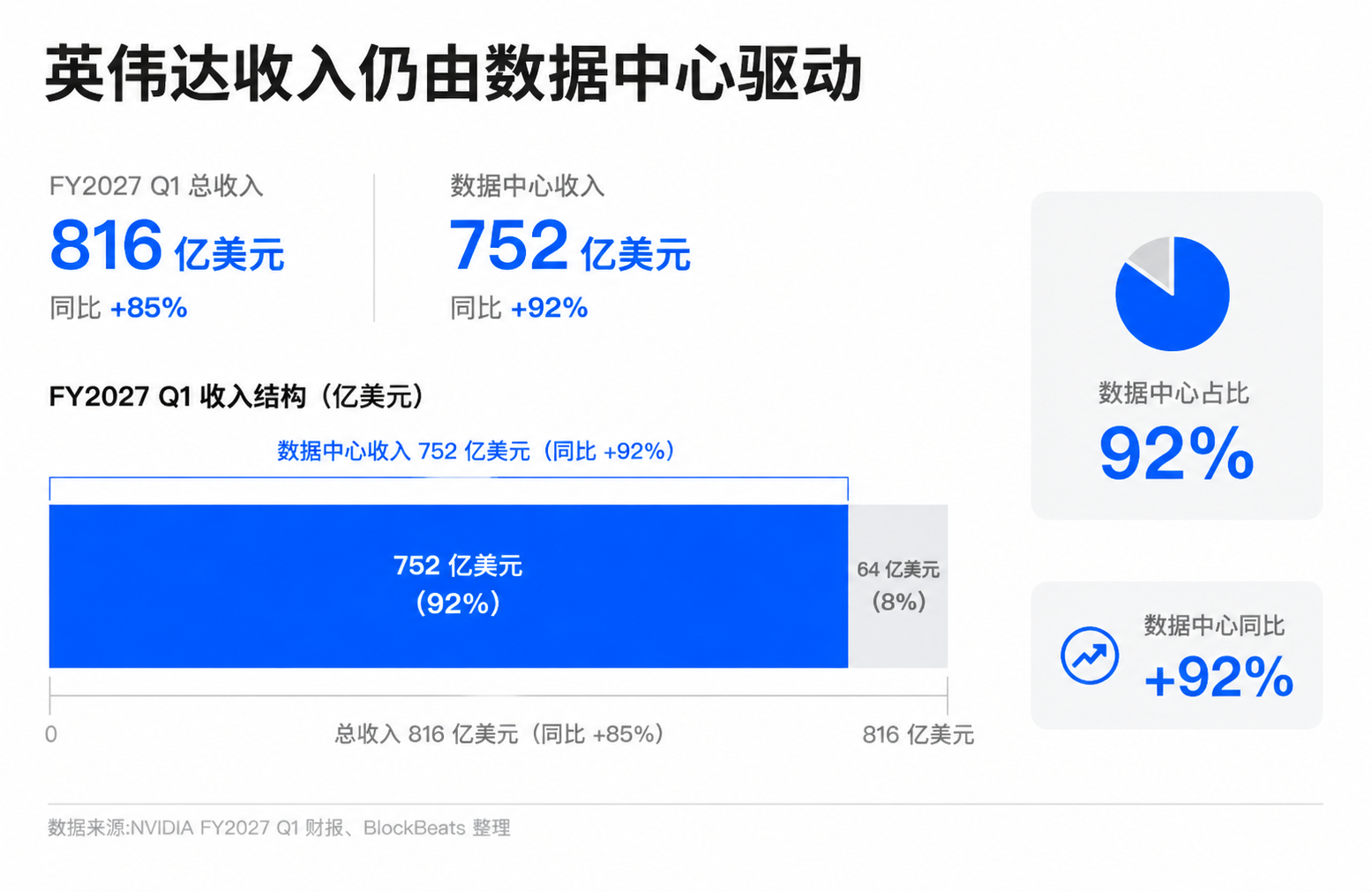

NVIDIA’s latest earnings report provides the strongest support for bulls. The FY2027 Q1 results, scheduled for release in May 2026, showed $81.6 billion in quarterly revenue and $75.2 billion in data center revenue—up 92% year-over-year. Against these figures, labeling the AI rally as a “bubble without fundamentals” lacks credibility.

Optimists on AI—including management teams at major tech firms and growth investors—use precisely this point to rebut the bubble thesis. They argue this rally represents an infrastructure cycle: rising training and inference demand drives GPU, networking, storage, power, and data center construction. Cloud providers increase capex to capture future AI service revenue, while enterprises integrate AI into software, advertising, search, productivity, and development workflows.

This framework has factual grounding. Over recent earnings seasons, major cloud providers have consistently emphasized strong AI demand and sustained growth in cloud segments. NVIDIA’s data center revenue has become a critical pillar in the U.S. earnings growth narrative. Broadcom, AMD, data center infrastructure, and power utilities are now part of the same investment chain. Markets assign higher valuations not merely due to compelling stories—but because orders, revenue, and profits are actually materializing.

That’s why BofA’s signals shouldn’t be bluntly interpreted as “the AI bull market is over.” If underlying fundamentals are still improving, high-valuation dynamics can persist longer than historical experience suggests. Especially in a market where passive funds, index weighting, and institutional allocations collectively reinforce the dominance of leaders, the continued strength of the strong is itself a mechanism of capital flow.

But real AI doesn’t equal safe valuations. A common misconception arises here: if a technological revolution is real, then prices can’t be expensive. History shows many bubbles were built on real technologies being prematurely and excessively priced. The internet truly transformed the world—but investors who bought many internet stocks in 2000 endured prolonged valuation compression.

The core debate in today’s AI rally has shifted from “Does AI work?” to “How much of the future has already been priced in?” That’s precisely why BofA’s historical signals matter—they remind investors: even if fundamentals are real, when prices reflect too many future positives, risk still rises.

Pressure Shifts to Revenue and Cash Flow

The AI bull market entering its most challenging phase isn’t due to sudden demand disappearance. The real shift is that the market now demands more proof.

For the past two years, investors accepted high valuations for AI leaders because the growth path looked clear: cloud providers increased capex, chipmakers sold more high-end GPUs, data center and network equipment firms secured orders, and future enterprise applications would unlock further revenue. Entering 2026, the market needs to see not just continued investment—but whether such investments translate into sufficient revenue, margins, and free cash flow.

Capital expenditure is the focal point. Microsoft, Google, Amazon, and Meta continue increasing AI and data center spending, with directionally clear intent. However, estimates across institutions and media vary significantly in scale. More importantly, investors are beginning to worry about the pressure higher capex places on free cash flow and return on invested capital. It’s not accurate to simply claim “AI investment can’t be recovered,” but as the investment curve steepens, market expectations for the return curve will rise accordingly.

For Microsoft, Google, Amazon, and Meta, continuing to ramp up AI investment is strategically necessary. Those who pause risk falling behind in cloud, search, advertising, productivity, model development, and developer ecosystems. From a shareholder perspective, however, higher capex means future earnings must prove these investments generate revenue upside, stable margins, and resilient cash flow.

For semiconductor players represented by NVIDIA, Broadcom, AMD, and SOXX, the logic differs slightly. They are direct beneficiaries of the AI investment cycle, with orders and profits materializing earlier. But precisely because the market already views them as core winners in the AI infrastructure cycle, any slowdown in cloud providers’ capex, delayed procurement, or renewed emphasis on capital discipline will be reflected first in semiconductor valuations.

This creates a more fragile feedback loop. Cloud giants increase capex, supporting chip company revenues. Chip companies grow rapidly, supporting index appreciation. Index gains and upgraded earnings fuel market confidence in the long-term AI cycle. If any link in this chain slows, the market may not face “the end of AI”—but rather a need to recalibrate valuations to match actual execution speed.

Second-Half Earnings Must Prove Risk Is Covered by Growth

BofA’s 70% bear market signals won’t automatically trigger a top. Nor will strong earnings from AI leaders automatically eliminate valuation risks. What truly needs validation next is whether sustained growth can absorb these valuation and structural risk signals.

The most direct window for observation is the second-half 2026 earnings season. Investors must see continued AI revenue growth from large tech firms, alongside margins that aren’t materially eroded by capex and depreciation pressures. Cloud providers must demonstrate that demand remains robust despite ongoing investment. For semiconductor firms like NVIDIA, Broadcom, and AMD, their order books and guidance will reveal whether downstream investment pace is slowing.

An additional variable is market breadth. If the S&P and Nasdaq keep making new highs while fewer stocks participate in the rally, and high-P/E stocks continue systematically outperforming low-P/E peers, BofA’s historical top structure becomes harder to ignore. Conversely, if earnings spread to more sectors and indices no longer depend solely on a few AI megacaps, risk signals may gradually dissipate over time and performance.

For ordinary investors, the current moment calls for portfolio and concentration checks. A blanket “bullish on AI” or “bearish on U.S. equities” stance won’t solve the problem. AI may remain the most important investment theme for years ahead—but as valuation, breadth, and capex pressure all rise, holding onto it has evolved from early trend discovery into a bet on execution speed.

Original: LawDong BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

U.S. Government Senior Official: Specific Arrangements Reached on the Destruction and Transfer of Enriched Nuclear Materials

2 hours ago

Goldman Sachs and Morgan Stanley are expected to each earn approximately $100 million in underwriting fees from SpaceX's IPO

2 hours agoCitrini Research Adds Long Position in Hyperliquid ETF

2 hours agoOpening with a cold splash, prominent institution CFRA issues a "sell" rating on SPCX

3 hours agoBinance: Binance Wallet SPCX x IPO Event Cancelled, Full Refund and SPCXB Airdrop Compensation Provided

3 hours agoSpaceX (SPCX.O) stock surges to $160, up approximately 18% intraday

3 hours agoElon Musk becomes the world's first trillionaire

3 hours ago