Banks Battle Stablecoins: Where Will Deposits Ultimately Flow?

Banks Battle Stablecoins: Where Will Deposits Ultimately Flow?

Throughout the long evolution of banking, depositors have consistently occupied a disadvantaged position. Individuals deposit funds into banks, which then lend out these funds to generate returns that are several times higher than the interest paid to savers. Savers accept this arrangement not because it is optimal, but because no better alternative exists—holding cash in hand leads to a continuous erosion of value over time.

The current average interest rate on standard U.S. savings accounts stands at only 0.6%, while investments in U.S. Treasury bonds and money market funds yield at least 4%. This traditional model has persisted for decades primarily because depositors lacked convenient alternatives. However, every few decades, new options emerge.

Stablecoins leverage blockchain technology to enable round-the-clock settlement, near-instant transaction confirmations, and transaction costs below one cent. Although regulations prohibit stablecoin issuers from directly paying interest to holders, the composability inherent in decentralized finance allows users to deposit stablecoins into lending protocols and earn annualized returns between 5% and 8%. This offers depositors a novel, high-yield outlet for their capital without sacrificing usability.

In this article, we analyze the measures banks have taken to prevent deposit flight and explore how this transformation will reshape the global banking and capital flows landscape.

Depositor Behavior

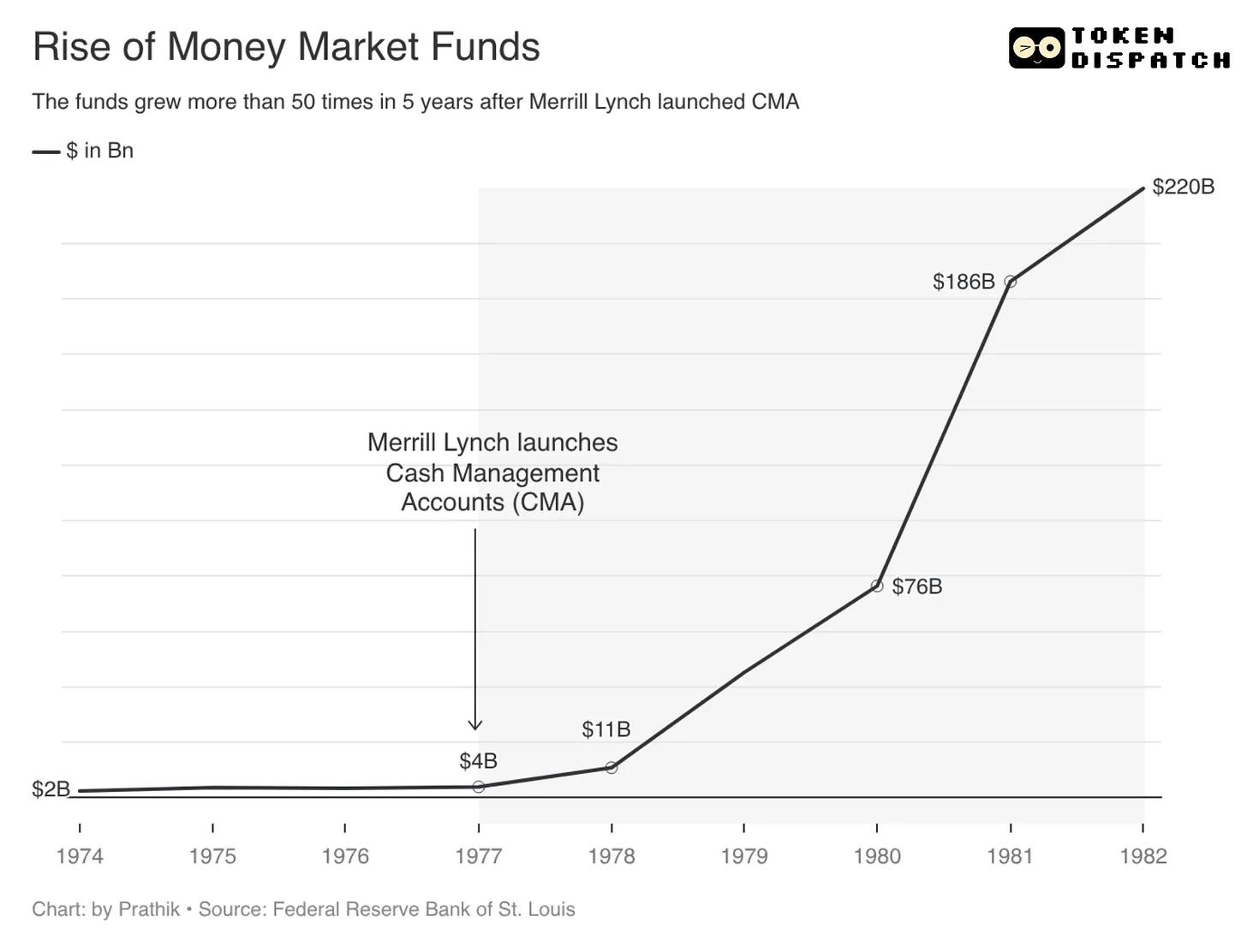

In 1977, financial services firm Merrill Lynch introduced the Cash Management Account (CMA). At the time, the U.S. Regulation Q capped bank deposit interest rates at 5.25%, while concurrent U.S. Treasury yields surpassed 7%. Merrill identified a regulatory loophole: through CMA functionality, it automatically swept idle funds from clients’ brokerage accounts into money market funds on a daily basis. Simultaneously, it offered customers checkable accounts and debit cards.

By combining multiple functions, customers enjoyed market-rate returns while retaining the liquidity and convenience of checking accounts. As a result, money market fund assets surged—from approximately $4 billion in 1977 to $220 billion by 1982, a 55-fold increase—driven largely by the outflow of bank deposits.

The banking industry responded with collective opposition. Ultimately, Congress repealed the interest rate cap under Regulation Q, prompting major banks to launch money market deposit accounts (MMDAs) with higher yields, enabling them to reabsorb deposits. The entire process—from the introduction of CMA to the abolition of rate caps—took nine years.

Today, technological innovation has reduced fund transfers to minutes or less, making prolonged waiting periods unacceptable for depositors.

During the Silicon Valley Bank (SVB) collapse on March 8, 2023, depositors initiated withdrawals totaling $42 billion within fewer than eight hours—an average of about $1.5 million per second. Over 85% of SVB’s deposits were uninsured, explaining the concentrated run on the institution.

Savvy depositors invariably shift funds to safer venues where capital can at least be preserved—and potentially appreciate.

Two Forms of Digital Dollars

Market response to this challenge has produced two competing forms of digital dollars, each following a divergent path: one seeks to remove capital from the banking system entirely, while the other retains capital within the system, merely changing its form.

First: Stablecoins

Taking Circle’s USDC as an example, when users convert USD into USDC, the corresponding fiat funds are used to purchase U.S. Treasury securities. These funds exit the bank’s balance sheet entirely. With less capital available for lending, banks lose their ability to capture interest rate spreads. Meanwhile, such funds no longer qualify for protection under the Federal Deposit Insurance Corporation (FDIC). If a stablecoin issuer ceases operations, holders may face irrecoverable losses.

The upcoming GENIUS Act, effective July 2025, establishes specific regulatory frameworks governing stablecoin issuance and usage. It explicitly prohibits stablecoin issuers from paying interest to users—a regulatory approach mirroring the original intent behind Regulation Q. Yet, just as Merrill circumvented Regulation Q by leveraging money market funds, today’s stablecoin issuers offer rewards in lieu of direct interest payments, a practice currently under debate in the CLARITY Act legislative discussions. Alternatively, users can independently deploy stablecoins into various DeFi lending protocols to earn yield.

For the banking sector, this represents an existential threat. Following SVB’s failure, billions in deposits exited the banking system within hours. Standard Chartered forecasts that by 2028, up to $500 billion in bank deposits could gradually migrate to stablecoins, with regional U.S. banks facing the most severe impact—given their heavy reliance on net interest margin (NIM) revenue.

Even if these projections prove exaggerated, the trend of deposit outflows is unmistakable. Hence, the four largest U.S. banks have, for the first time in decades, joined forces to explore new strategic responses.

Second: Tokenized Deposits

The core advantage of stablecoins lies in ultra-low transaction costs and sub-second settlement. To address this pain point, the banking industry has introduced tokenized deposits.

Banks can convert customer deposits into on-chain tokens, enabling low-cost, high-efficiency movement across blockchain networks. Crucially, the underlying USD deposits remain on the bank’s balance sheet, allowing continued lending activities and interest generation. Furthermore, tokenized deposits retain FDIC insurance coverage.

Currently, two major banking coalitions are driving the adoption of tokenized deposits.

The first is the Clearing House Network, built collaboratively by more than a dozen institutions including JPMorgan Chase, Citigroup, Bank of America, and Wells Fargo. This unified platform aims to launch in the first half of 2027. Targeted primarily at institutional clients, it will enable 24/7 settlement, programmable payment clearing, and cross-border transactions—directly countering competition from stablecoins.

The second is the Cari Network, formed by five regional banks: Huntington National Bank, M&T Bank, KeyCorp, First Horizon, and Old National Bank, collectively managing around $780 billion in assets. Leveraging ZKsync’s Prividium technology stack based on zero-knowledge proof blockchain, this network is building a retail-focused tokenized deposit platform expected to launch in Q4 2026. The early push by regional banks underscores the severity of the deposit leakage risk—these institutions depend heavily on NIM income for survival.

So, which product will ultimately win depositor preference?

Historical precedent suggests depositors do not solely evaluate products based on intrinsic quality—they prioritize solutions that most effortlessly resolve their immediate pain points.

In the late 1970s, depositors sought higher returns. Regulation Q limited bank deposit yields despite rising market interest rates, rendering traditional deposits uncompetitive. Merrill’s innovation lay in decoupling the two core demands of banking: market-competitive returns and daily liquidity. Once regulation was lifted, banks themselves launched money market deposit accounts, integrating these same features.

Today, stablecoins offer similar advantages to Merrill’s original product: they operate outside the traditional banking framework, enable global circulation, interoperate with various crypto platforms, and allow programmable use of idle capital. Yet they share the same weakness as early money market funds: they are not insured bank liabilities, and asset safety depends entirely on the issuer’s solvency, reserve structure, redemption channels, and overall regulatory environment.

In contrast, tokenized deposits replicate the strengths of traditional banks in the 1980s: funds remain within the regulated banking system, preserving banks’ lending and interest-generating models, while maintaining familiar FDIC insurance. But due to adherence to existing banking regulations, tokenized deposits lack the openness, liquidity, and composability of stablecoins. While bank deposits can be accelerated and made programmable, once they achieve full open-access characteristics akin to stablecoins, banks would lose core control over their deposit base.

Thus, the central battleground is increasingly becoming a contest over the right to convert capital.

Against this backdrop, a third path emerges—one that reveals the nascent shape of future banking and monetary systems.

The Bridge of Integration

On May 27, 2024, SoFi Bank officially launched SoFiUSD—the first stablecoin issued by a national U.S. bank. The token is live on Ethereum and Solana blockchains, and SoFi’s 15 million users can exchange and use it via mobile app. SoFiUSD inherits all key attributes of stablecoins: 24/7 liquidity, near-instant cross-border settlements, and transaction fees measured in cents.

At the same time, users can seamlessly convert SoFiUSD into tokenized deposits within the same app. These deposits earn interest and remain FDIC-insured. Users enjoy flexible switching: use stablecoin for fast, frictionless transfers; switch to tokenized deposits for yield and safety. Should the offered interest rate be unsatisfactory, users can revert to stablecoin and deploy funds into DeFi protocols for higher returns.

SoFi may never achieve the decentralization of Circle or match the scale of JPMorgan—but it has forged a unique advantage: integrating bank accounts, stablecoin wallets, and tokenized deposits within a single user interface.

This model echoes Merrill Lynch’s original strategy, distinct from pure stablecoin issuers or traditional banking consortia. SoFi aims to eliminate the binary choice between blockchain convenience and banking yield—no longer forcing users to trade one for the other.

The evolutionary trajectory of these products confirms a fundamental truth: in the domain of capital storage and transfer, the product’s form is secondary; the ability to freely transition between forms is paramount.

Faced with the disruptive force of stablecoins, banks initially responded by lobbying regulators to ban interest payments and incentives from stablecoin issuers. But regulatory pressure alone cannot win this race. The only viable path forward is proactive evolution—matching, and even surpassing, the capabilities of crypto-native products: offering sub-second settlement, programmability, interest earnings, and FDIC insurance. Ironically, the vehicle for achieving this upgrade is blockchain technology itself.

This is the essence of market dynamics: it compels traditional industries to continuously evolve until the entire ecosystem maximally serves participants. Merrill’s CMA forced the repeal of Regulation Q and spurred the creation of money market deposit accounts; now, the rise of stablecoins is pushing banks to develop tokenized deposits and 24/7 settlement systems. In both cases, traditional institutions were not eliminated—they absorbed innovations, iterated, and retained their relevance.

This wave of disruption hits regional banks hardest. They rely more heavily on net interest margins and have far less buffer against deposit outflows than large banks. Optimizing traditional accounts risks losing users seeking high liquidity; chasing crypto-like speed undermines the core advantages of FDIC insurance and lending profitability. The Cari Network represents a defensive strategy by regional banks; the Clearing House Network embodies a fortress defense by large banks. SoFi, however, adopts a bolder approach: proactively building an integrated bridge to avoid being overtaken by external players.

Looking back at financial history, emerging sectors often break through by exploiting inefficiencies in traditional systems. When those pain points become undeniable, established giants absorb new features and upgrade—preserving their market dominance. Merrill highlighted the misalignment between deposit rate caps and market yields; banks responded with MMDAs. Now, stablecoins expose the limitations of traditional banks—restricted to business-day settlement and constrained capital flow—prompting banks to adopt tokenized deposits and 24/7 settlement mechanisms.

Industry leadership is shifting—not from the innovators who first identified problems, but to those who can integrate functionalities, operate compliantly, and scale solutions effectively.

We have been emphasizing recently: the cryptocurrency sector—or more precisely, blockchain technology—is becoming the foundational infrastructure of fintech.

This assessment holds true in this transformation. Blockchain does not aim to replace bank deposits entirely. Instead, it forces the industry to disassemble service value dimensions: yield is one layer, settlement efficiency another, FDIC insurance a third. And perhaps the highest-value layer is the freedom to switch seamlessly between forms.

No matter the final outcome, bank deposits will not vanish—they will be decomposed and reassembled. The ultimate winners will be those institutions capable of enabling frictionless switching among security, yield, and high liquidity.

By: Prathik Desai, Translated by: Chopper, Foresight News

Disclaimer: Contains third-party opinions, does not constitute financial advice

Tiger Research: Tokenized Stock Markets in 2026, the Rise of Perpetual Contracts

06-09

The Battle for U.S. Stock Tokenization: Can Ondo, xStocks, or NYSE Become the Next Generation Asset Gateway?

06-03

CoinGecko Report: RWA Sector Size Reaches $19.3 Billion, with Gold and U.S. Treasuries Leading the Way

04-30

a16z Crypto Operating Partner: Wall Street Undergoing Its Largest Infrastructure Upgrade in 30 Years

03-26

NYSE and Nasdaq Both Enter the Arena—U.S. Stock Tokenization Begins Battle to the Death

03-25

Top V influencers' calls combined with Bittensor subnet to achieve the largest decentralized LLM pre-training in history — TAO's price doubles within a month

03-25Ethereum block builder Eureka Labs completes $6.7M seed round, co-led by Spark Capital and Collider Ventures

03-25