Japan's Central Bank on the Brink of Rate Hike—Can the AI Bull Run Withstand?

Japan's Central Bank on the Brink of Rate Hike—Can the AI Bull Run Withstand?

TL;DR

If you closely follow price movements of Nvidia, Microsoft, Bitcoin, or Ethereum, you typically focus on core variables such as U.S. inflation data, Federal Reserve interest rate policy trajectories, AI-related revenue realization, and on-chain capital flows. Yet this week, market attention has been diverted toward a seemingly more distant variable: the direction of Bank of Japan (BOJ) interest rates.

The reason is straightforward. For many years, the Japanese yen has been one of the cheapest funding currencies globally. Investors could borrow low-yield yen, convert it into dollars or other currencies, and then invest in higher-yielding, faster-appreciating assets. This is known as the yen carry trade—basically borrowing low-rate yen to buy high-return assets.

While it doesn’t directly appear in any single AI stock or Bitcoin address, it profoundly influences global risk appetite and leverage costs. Now, with the BOJ exiting its prolonged ultra-low-interest environment, markets are recalibrating how long this “low-cost credit card” can still be used.

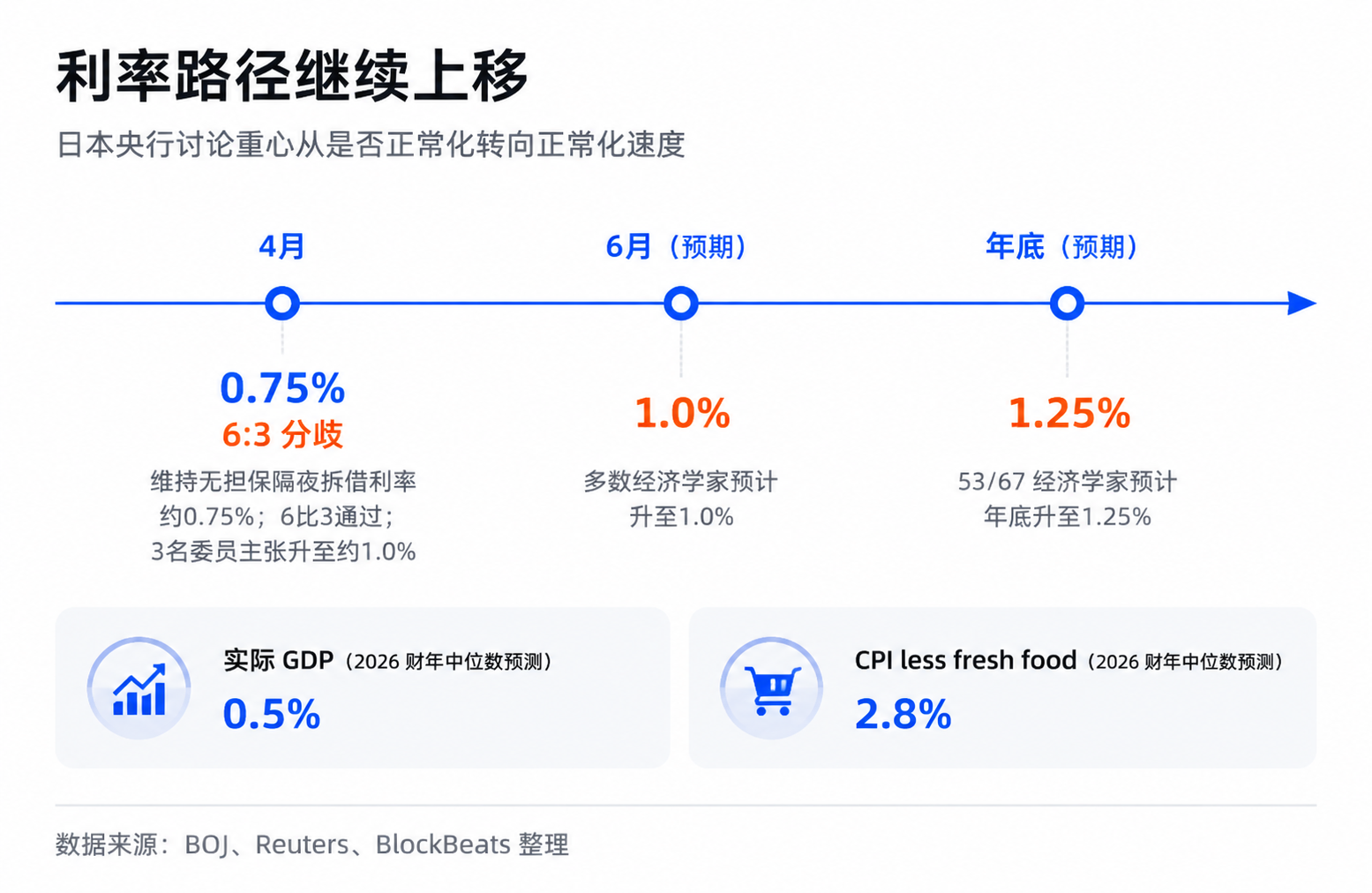

According to Reuters on June 10, 66 out of 70 economists surveyed expected the BOJ to raise its policy rate from 0.75% to 1.0% at its June meeting. In another survey, 53 out of 67 economists anticipated rates reaching 1.25% by year-end. The meeting concludes on June 16, and as of June 15, 1.0% remains the consensus forecast—not an announced result.

A 25-basis-point move may seem small. What markets fear isn’t the number “1%” itself, but the broader implications when cheap money begins to become expensive—specifically, whether assets that have relied on low-cost financing, crowded positions, and elevated risk appetite will now face re-pricing. AI mega-cap stocks and crypto sit at the most sensitive end of this chain.

The BOJ Moves Global Funding Foundations

You can conceptualize the yen carry trade as a low-interest credit card. As long as borrowing costs remain low, exchange rates stable, and target assets appreciating rapidly, investors are willing to leverage via this card. For decades, the yen has functioned as the world’s de facto credit card.

Its importance lies not just in serving the Japanese market. Low-yield yen can be converted into dollars, flowing into U.S. equities, bonds, emerging markets, commodities—and indirectly affecting crypto risk sentiment. During periods of global asset appreciation, carry trades amplify liquidity. When the yen strengthens or Japanese rates rise, the chain reverses, forcing some funds to deleverage, repay debt, and reduce exposure.

Thus, investors cannot assess the BOJ’s impact solely through Japan’s economic scale. The central bank isn’t altering expectations for a domestic industry—it’s shifting a foundational, long-standing source of low-cost capital across the global financial map.

The signal was already evident in April’s meeting. While the BOJ maintained its unsecured overnight interbank rate near 0.75%, the voting split was 6–3, with three members advocating an immediate hike to approximately 1.0%. In the same month’s outlook report, the BOJ revised its 2026 fiscal year real GDP forecast downward to 0.5% and raised its core CPI forecast to 2.8%. The policy debate had shifted from “whether” to normalize, to “how fast.”

Market consensus remains cautious: gradual BOJ hikes with ample forward guidance, and some carry positions already unwound in prior volatility cycles. But from a risk framework perspective, what matters is something else: as long as residual leverage persists, the trigger for volatility is rarely the absolute level of interest rates, but rather the speed of change in yield differentials and exchange rate expectations.

This speed is critical for AI stocks and crypto. Both are high-beta assets—those with greater price elasticity. They surge aggressively during liquidity abundance but drop sharply when risk appetite declines. While AI leaders have real revenue and industrial momentum, Bitcoin also has ETF inflows, halving cycles, and on-chain structural tailwinds—but their marginal pricing remains highly dependent on global risk sentiment.

When cheap money diminishes, markets may not immediately reject the AI or crypto narratives, but they may lower the valuation multiples investors are willing to pay for future growth.

25bps Gets Amplified by Leverage and FX

Looking at 25 basis points alone, a BOJ rate hike shouldn’t disrupt global assets. The issue lies in the nature of carry trades—not simple deposit-loan comparisons, but a system layered with leverage, currency exchange, and crowded positions.

A typical yen carry trade has three sources of return: low cost of borrowing yen, high yield on purchased assets, and either no appreciation or depreciation of the yen. As long as all three hold, the trade is comfortable. Once Japanese rates rise, the first leg is compressed. If markets begin pricing in yen appreciation, the third leg turns into risk. Investors don’t just earn less—they may even lose on currency moves.

This explains why 1% isn’t inherently scary. But moving from 0.75% to 1.0%, and having the market anticipate 1.25% by year-end, changes the calculus. The worst fear isn’t gradual cost increases, but the simultaneous realization across traders that the same trade is no longer profitable—prompting a rush to unwind.

Unwinding translates local policy into global risk asset pressure. Investors must repurchase yen to repay debt, potentially selling dollar-denominated assets, tech stocks, crypto, commodities, or emerging market positions. When many players act similarly, price declines trigger additional margin calls, risk controls, and volatility model adjustments—creating second-order amplification.

The IMF’s April 2026 Global Financial Stability Report warned that carry trade unwinding can amplify market volatility through capital flows, bond yield swings, leveraged ETFs, and non-bank deleveraging channels. The key point isn’t that every dip is caused solely by the BOJ, but that this mechanism exists and intensifies shocks during periods of liquidity stress.

Over the past two years, markets have repeatedly seen similar dynamics: momentum stocks, AI tech stocks, and Bitcoin have synchronized downturns—even in the absence of new Fed announcements or sudden firm-specific fundamentals. Institutional analyses often cite yen carry unwinding as one explanation. Strictly speaking, this only proves temporal coincidence and plausible mechanism—not unique causality. But for traders, correlation and transmission channels are sufficient to constitute a risk variable.

Markets Trade Rising Funding Thresholds

More accurately, markets aren’t trading “Japan raising rates destroys AI,” but rather “global risk assets face rising funding thresholds.” These are two distinct phenomena.

AI trends still have their own drivers: cloud vendors’ capex, GPU demand, model deployment, enterprise software revenue—these are the long-term fundamentals underpinning companies like Nvidia and Microsoft. Bitcoin also has its own narrative: ETF inflows, regulatory frameworks, macro hedging stories, and on-chain supply structures. The BOJ does not replace these variables.

But in high-valuation regimes, fundamentals answer whether value exists over time, while liquidity determines how much multiple investors are willing to pay for that future. When low-cost global financing is abundant, investors are willing to pay high premiums for future growth. When funding costs rise and risk appetite falls, the same growth story may be discounted more heavily.

This is the essence of implicit financing cost: it doesn’t necessarily show up as a company’s loan rate increase or a fund’s direct yen borrowing. Instead, it reflects the market’s overall leverage temperature—cheap money encourages risk-seeking behavior. As capital becomes pricier, tolerance for losses, deferred profits, and valuation bubbles drops.

Therefore, the market significance of this BOJ meeting isn’t whether 1% is a high rate. In U.S. or many emerging markets, 1% would be unremarkable. But in the historical context of the yen as a global funding currency, it signals a directional shift—a long-standing pipeline of cheap leverage is transitioning from deeply subsidized levels toward normalcy.

“The carry trade is mostly unwound” doesn’t mean risk vanishes. Some positions have indeed been reduced in prior volatility cycles, and the June hike expectation has been priced in. But as long as residual exposures remain in banking systems, offshore yen lending, and non-bank leverage, prices will stay sensitive to the pace of normalization.

Even more crucially, the yen is just one visible anchor. Global risk assets over recent years haven’t relied solely on the Fed—they’ve also been influenced by multiple low-cost funding currencies, offshore liquidity, and cross-market leverage. When these sources simultaneously become less accessible, even if the Fed pivots to easing, it may not fully offset the marginal tightening elsewhere.

After the Decision: Watch Yen, JGBs, and High-Beta Asset Correlation

The validation point is clear: post-June 16 BOJ decision, will the market simply “buy the rumor, sell the fact,” or begin repricing a faster normalization path?

If the BOJ raises rates to 1.0% as forecasted, but with a dovish tone, USD/JPY reacts calmly, and U.S. tech and crypto don’t show synchronous pressure, this suggests a pre-priced policy event. Markets will refocus on AI revenue, Fed trajectory, and U.S. earnings cycles, treating Japan as a short-term noise factor.

If the decision or post-meeting commentary leads the market to price in a year-end rate of 1.25% or higher, triggering rapid yen appreciation, rising JGB yields, and synchronized weakness in Nvidia, other momentum tech stocks, BTC, and ETH—this indicates traders are no longer pricing just 25 bps, but rather the contraction of the yen-based leverage chain.

Next, monitor the linkage between prices: Does yen strength coincide with weakness in high-beta assets? Does volatility rise without new U.S. negative catalysts? Do leveraged ETFs and crowded momentum stocks lead the downside? As soon as these signals align, the BOJ ceases to be just Japan’s central bank—it becomes a reminder that the map of global cheap money is becoming increasingly expensive.

Original: BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

Pharos Network Unlocks AI Model Payment Channels, Introduces New Use Cases for $PROS and USDC as Platform Payment Instruments

28 days ago

NVIDIA Has Plenty of Cash—Why Is It Borrowing $20 Billion?

28 days ago

Will Claude Ban Accounts and Verify ID Cards? Face Recognition Was Old News from Two Months Ago, and "Handing Over Data to Police" Is a Misinterpretation

28 days ago

5-Second Breakthrough with Just 1 Interaction: Has the "Strongest Security Mechanism" of Claude Fable 5 Been Cracked by a Chinese Team?

06-13

Why Is the "AI Service Subscription Model" Inevitably Headed for Extinction?

06-13

Managing a company valued at nearly a trillion dollars, Anthropic's CEO has only one direct report.

06-13

ERC-8126: A New Ethereum Standard for Issuing "Security Health Reports" to AI Agents

06-12