Will the U.S. and Japanese rate hikes trigger a stock market drop this week?

Will the U.S. and Japanese rate hikes trigger a stock market drop this week?

This week’s global market narrative centers on Japan’s rate hike and the Federal Reserve meeting. For risk assets, this week is destined to be far from tranquil.

Three months ago, Wall Street was debating when rate cuts would begin. With Powell newly appointed, markets were willing to grant the new chairman some goodwill— inflation was easing, employment was cooling, and a rate cut seemed merely a matter of time. But as financial markets often demonstrate, the script everyone anticipated never materialized.

May’s CPI rose 4.2% year-on-year and 0.5% month-on-month, with energy prices surging 3.9% MoM; core CPI remains near 2.9% YoY. Employment has not yet provided the Fed with an immediate reason to pivot dovish: nonfarm payrolls added 172,000 in May, while unemployment held steady at 4.3%. This presents the Fed with a delicate balancing act: inflation is reaccelerating, labor markets remain resilient, AI-driven investment continues to underpin economic durability, making the case for rate cuts weaker, while conditions for tightening are gradually accumulating.

Meanwhile, the Bank of Japan’s policy meeting on June 15–16 has already priced in a 25 bps hike as the baseline scenario. Polymarket’s “Bank of Japan Decision in June” market shows a 98.3% probability of a 25 bps increase, no change at just 1.45%, and hikes of 50 bps or more at around 0.55%.

Many still recall how prior BoJ rate hikes significantly impacted global financial markets. This week faces the dual pressure of Tuesday’s Japanese rate hike and Thursday’s FOMC meeting—will markets decline?

Let’s first examine the Fed side.

The likelihood of a rate cut appears to have been nearly closed. On Polymarket, “No rate cuts in 2026” stands at 70.35%, “Rate cut before July” at 2.35%, and “Rate cut before December” only 23%. A majority—70%—are betting on no cuts this year. By year-end, the median rate range forecasts: 3.75% upper bound at 37%, 4.00% at 32.5%, 4.25% at 11.25%, and 4.50% or higher at 3.35%, totaling 47% above 4.00%.

Market consensus on Powell’s stance is clear: he is unlikely to initiate a hike during his debut FOMC meeting this week. The primary risk lies beyond Q3. Several Polymarket contracts illustrate this consensus:

“Fed rate hike in 2026?” — 34.5% chance of a hike anytime in 2026;

“Fed rate hike by...?” — 0.65% before June, 6.15% before July, 24.5% before September, 32% before October;

“Fed Decision in July” — 3.15% chance of a 25 bps hike, 0.3% for 50 bps+, 93.5% unchanged;

“What will the Fed rate be at the end of 2026?” — 37% probability of ending at 3.75%, 32.5% at 4.00%, 11.25% at 4.25%, 3.35% at 4.50% or higher.

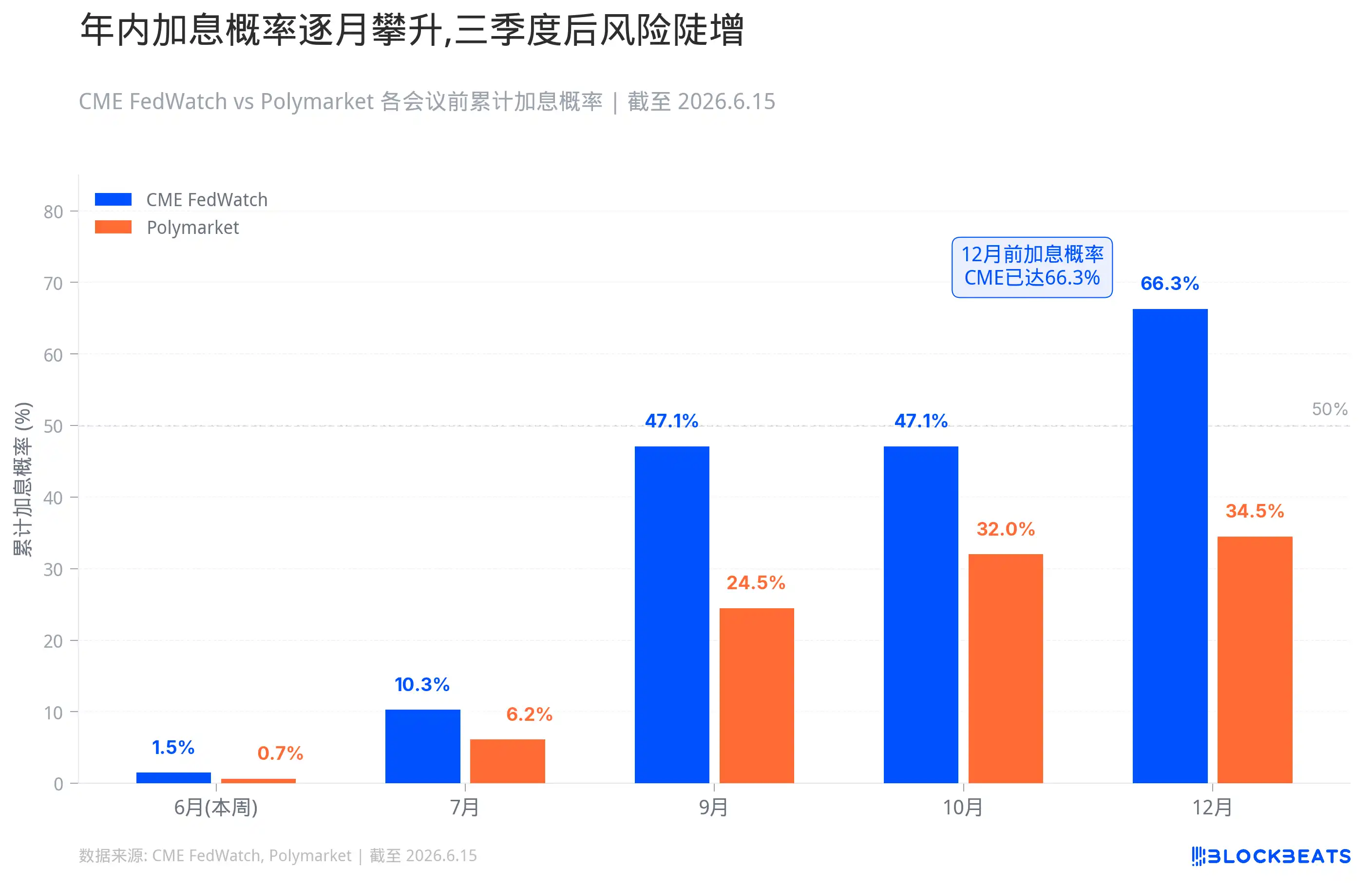

More granular data: probability of a hike before July 29th is ~10.3%, before October 28th ~47.1%, before December 9th ~66.3%. Polymarket takes a more conservative stance: 34.5% for “Fed rate hike in 2026?”, 24.5% before September, 32% before October. Current month probabilities: CME FedWatch assigns 98.5% for no change, Polymarket gives 99.55%.

It is highly likely the US will hold steady this week—but “no action” is not the same as “no tightening.”

If Powell acknowledges that inflation risks now outweigh growth concerns in his press conference, if the dot plot shifts 2026 terminal rate from a cut trajectory to flat or upward revision, or if the statement removes language signaling “dovish bias,” the market itself will complete the tightening process.

The first reaction will come from short-dated US Treasuries. 2-year and 1-year yields move directly with Fed path expectations. Once the market shifts from “rate cuts later” to “possible hikes later,” short-end yields will spike. USD will also gain support—the strong dollar itself constitutes a global tightening signal.

In equities, high-valuation growth stocks and long-duration AI assets are most sensitive. Higher rates reduce the present value of future cash flows, increase funding costs, and diminish appetite for unproven narratives. Small-cap, micro-cap, and unprofitable tech stocks are even more vulnerable—these companies thrive on cheap capital, and once borrowing becomes expensive, their valuations collapse first.

If a true tail-risk scenario materializes—Fed hikes despite a 98.5% “no change” pricing—the shock could be severe. Short-term yields surge, USD spikes, leveraged positions face forced deleveraging. It’s not inevitable, but the existence of such a probability means there may be no time to react if it occurs.

Moreover, Powell’s “debut” carries outsized market significance—not just because of his leadership role, but due to potential changes in Fed communication style. Timiraos, a veteran Fed tracker, has made it clear: symbolic adjustments like dot plots, statement phrasing, and press conference rhythm can be implemented quickly, but transforming the Fed’s communication framework requires sustained persuasion and internal alignment. This week’s meeting may mark the first step.

Now consider Japan. The BoJ’s June 15–16 policy meeting has seen a 98.3% implied probability of a 25 bps hike on Polymarket. If executed, the policy rate will rise from 0.75% to 1.00%, the highest since 1995.

The logic behind Japan’s forced tightening is straightforward. Middle East tensions have driven oil prices up—Japan, a net energy importer, sees its import costs amplified by a weak yen. Wages are rising, service prices are increasing, and inflation expectations are loosening. Persistently low rates risk undermining market confidence in the BoJ’s commitment to price stability.

A rate hike itself is not in doubt. Yet a critical concern remains: over the past few years, vast amounts of global capital have borrowed cheap JPY to invest in higher-yielding assets—US Treasuries, equities, credit, and some indirectly into high-volatility risk assets. This structure relies on one assumption: Japanese rates stay ultra-low, JPY financing remains cheap, and the central bank moves slowly. Should markets perceive Japan’s rate normalization as continuous, carry trades become fragile, JPY shorts get squeezed, and global leverage begins to contract.

Market fear of a Japanese rate hike is not unfounded. Over the past two decades, every time the BoJ attempted to raise rates from near zero, global markets suffered.

The first instance was August 2000: the BoJ raised rates from 0% to 0.25%, precisely coinciding with the peak of the US internet bubble. Within three months, Nasdaq fell 35%. Japan’s economy couldn’t withstand the shock either, quickly slipping back into recession—prompting the BoJ to cut rates back to zero in 2001.

The second came between 2006 and 2007: the BoJ raised rates in two steps to 0.5%—first in July 2006, then February 2007. The timeline closely mirrored the buildup of the US subprime crisis. Subprime defaults began erupting in summer 2007, Lehman collapsed in 2008, triggering the global financial crisis. The BoJ was again forced to return rates to zero.

The third occurred on July 31, 2024: the BoJ raised rates from 0% to 0.25%, a modest move, yet market reaction was extreme. On August 5, Nikkei 225 plunged 12.4% in a single day—the worst drop since Black Monday 1987. Korea’s KOSPI hit circuit breakers, Nasdaq and S&P 500 dropped 3.4% and 3% respectively. VIX volatility index surged past 65. The mechanism was clear: BoJ hike triggered a sharp JPY appreciation, forcing unwinding of JPY-denominated carry trades—selling foreign assets and buying back JPY—leading to cascading sell-offs. To cover margin calls, fund managers sold even “safe-haven” assets like gold and BTC. In the liquidity crunch, all asset correlations converged toward 1. The market’s agony from that day remains vivid in memory.

Thus, more important than the hike itself is what the Japanese government signals in tomorrow’s press conference: how high will rates go?

As previously noted, each of Japan’s three recent hiking cycles has led to global market declines.

Yet, in reality, the BoJ’s rate hikes themselves don’t always trigger crashes—crashes typically occur when other vulnerabilities exist. In 2000 and 2007, they coincided with larger bubbles elsewhere. In August 2024, the hike was unexpected, and market positioning was too heavy to react. But subsequent hikes—when markets were prepared—did not cause systemic issues.

This 25 bps hike is now priced at 98.3%, leaving little room for surprise. Based on experiences in December 2024 and January 2025, the hike itself is likely to be absorbed smoothly. But two additional variables stand out.

First, Governor Haruhiko Kuroda is hospitalized due to infectious hepatic cysts and expected to miss both the meeting and post-meeting press conference. According to public reports, Vice Governor Ryōzō Higashino will serve as acting chair during the meeting, while Vice Governor Shinichi Uchida will lead the press conference. This arrangement is unlikely to alter the rate hike direction. However, market participants are less familiar with Uchida’s communication style compared to Kuroda. Interpretation of subtle phrasing will amplify volatility: a statement like “future decisions will depend on data” versus “there remains room for rate normalization” may seem similar, but traders see them as entirely different signals.

Second, the US Fed meets the same week. The BoJ meeting and FOMC are separated by just one day. If the BoJ hike causes only mild market reaction, but Powell delivers hawkish rhetoric the next day, the combined pressure will intensify. Conversely, if markets are already jittery after the BoJ hike, Powell adding fuel could provoke excessive short-term reactions. The back-to-back announcements inherently amplify volatility.

Let’s analyze individual asset classes:

US Treasuries are likely to be the first to react this week. Short-end yields follow the Fed path directly—2-year and 1-year maturities are most sensitive. If Powell’s press conference leans hawkish or the dot plot is revised upward, short-end yields will rise, reflecting market reassessment of “later cuts” or even “potential hikes this year.” Long-end yields are more complex: 10-year yields may not rally in tandem. If concerns grow about high rates damaging the economy, the yield curve could flatten further or deepen into inversion. In Japan, if Uchida hints at further hikes, Japanese sovereign yields will rise. Any marginal loosening in Japan’s $1.13 trillion US Treasury holdings could reverse supply-demand dynamics in the US bond market.

USD is likely to be supported. A hawkish Fed shift raises expected returns on dollar assets, strengthening DXY. While a BoJ hike theoretically benefits JPY and burdens USD, actual direction depends on messaging: if the BoJ signals dovishness after hiking, JPY might fall instead, reinforcing USD strength. With both central banks meeting in the same week, relative movements between USD and JPY will be highly sensitive, lifting FX volatility. Asian and emerging market currencies will face pressure—strong USD represents global monetary tightening, draining offshore dollar liquidity.

In equities, divergence will be stark. High-valuation growth stocks, long-duration AI assets, small-caps, micro-caps, and unprofitable tech stocks are most vulnerable. Higher rates reduce the present value of future cash flows, increase funding costs, and erode willingness to pay premiums for unproven stories. Russell 2000 and companies reliant on cheap capital will suffer first. Banking stocks will react more complexly—short-term net interest margins may benefit, but if the yield curve continues to invert and credit risks rise, outcomes may be negative. Defensive stocks offer relative resilience, but utility and REITs—“bond-like” assets—are also pressured by high rates. S&P 500 closed Friday near 7382, Nikkei 225 at 66078. If both central banks lean hawkish this week, both US and Japanese equities will face headwinds, especially tech-heavy indices.

Japanese equities face a unique situation. BoJ hikes harm export-oriented firms via JPY appreciation, eroding overseas profits. But if the hike size and pace align with expectations, the Nikkei may not crash—December 2024 and January 2025 experience confirms this. The real risk lies in post-meeting communication: if Uchida suggests further normalization, the Nikkei may initially drop before stabilizing.

Gold will face opposing forces. Rising real rates and stronger USD typically weigh on gold, but if hikes stem from energy shocks, geopolitical risks, or runaway inflation, safe-haven demand could support prices. This week, gold is likely to trade sideways at highs, with direction determined by which fear dominates: fear of rising rates or fear of uncontrolled inflation. Crude oil hinges more on supply-demand fundamentals and geopolitics—Iran conflict remains active. If rate hikes are driven by oil-fueled inflation, crude may not immediately fall. But if the market starts pricing in weakening demand, industrial metals and crude will face downward pressure.

Credit and real estate are slower-moving variables, but trends are clear. High-yield corporate spreads will widen, financing costs rise, commercial real estate, REITs, and mortgage-sensitive assets face stress. Emerging markets with high USD debt exposure will suffer more, facing intensified capital outflows.

The crypto market is similarly under pressure amid this macro backdrop. BTC hovers near $65,000—down from $72,000 in early June, falling to ~$61,500 after CPI data, rebounding only recently. At this level, the position is unstable. On June 5, when BTC dipped below $62,000, chain-based long liquidations exceeded $1.5 billion, and Bitcoin spot ETFs saw a weekly net outflow of $2.7 billion. Prices have recovered somewhat, but positioning remains unhealthy. BTC exhibits partial macro asset characteristics—it doesn’t necessarily crash with rate hikes, but it struggles to perform independently. ETH, SOL, altcoins, memes, and small-cap tokens are even more fragile—these assets rely on liquidity spillovers and elevated risk appetite. Once markets start comparing the yield attractiveness of cash, short-term bonds, and money market funds, high-beta assets will be the first to be trimmed. Futures market funding rates have declined, on-chain risk appetite cooled—this occurred earlier in June.

Original: BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

06-16

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

06-16Amazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

06-16Binance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

06-16Binance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

06-16

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

06-16SlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

06-15