NVIDIA Has Plenty of Cash—Why Is It Borrowing $20 Billion?

NVIDIA Has Plenty of Cash—Why Is It Borrowing $20 Billion?

TL;DR

NVIDIA’s recent bond issuance is most easily misunderstood as a simple question: with so much cash on hand, why borrow?

Based on the company’s most recent fiscal quarter data, ending April 26, 2026, for FY2027 Q1, NVIDIA generated $81.6 billion in revenue and approximately $48.6 billion in free cash flow (FCF). Meanwhile, the company also increased its stock buyback authorization by $80 billion and raised its quarterly dividend from $0.01 to $0.25 per share. In other words, this is not a cash-strapped firm relying on bond markets for survival.

Yet precisely because of this strength, the market has shown heightened sensitivity toward its proposed issuance of at least $20 billion in senior notes. The bonds span maturities from 2 to 30 years, with proceeds earmarked for general corporate purposes, refinancing, AI data centers and infrastructure, R&D, supply chain prepayments, and strategic investments. For investors, the real question isn’t “Does NVIDIA have money?” but rather: when AI—the biggest cash cow in the current cycle—begins systematically leveraging long-term debt, has the capital expenditure narrative around AI entered a new phase?

The core insight isn’t that NVIDIA suddenly needs capital, but that it is transforming its strong cash position and credit rating into an expanded capacity for growth.

Cash Strength Enables Long-Term Borrowing

Ordinary investors see “issuing bonds” and immediately assume financial distress. But for mature, large-cap companies, borrowing is often not a reactive measure—it’s a proactive choice to access cheaper, shareholder-friendly financing.

NVIDIA’s proposed issuance consists of senior notes—corporate IOUs—effectively borrowing from bond investors with scheduled interest payments and principal repayment at maturity. The key distinction from equity issuance is that bond issuance does not dilute ownership. As long as future returns exceed the cost of debt, existing shareholders retain a larger share of value.

This is the crux of the paradox: NVIDIA’s most recent quarter generated roughly $48.6 billion in FCF—significantly higher than the scale of the proposed financing. Combined with massive buybacks and dividend hikes, the issuance cannot be simply interpreted as a sign of insufficient cash.

A more plausible explanation is that NVIDIA is locking in long-term capital during a period of peak credit strength, when the market is most willing to lend. For a company in the midst of an AI infrastructure expansion cycle, projects like data centers, supply chain prepayments, ecosystem investments, and R&D are inherently long-term endeavors with return horizons spanning multiple years—or even decades. Matching 30-year debt with long-duration assets aligns closer to sophisticated capital management than relying solely on short-term operating cash flows.

This is what “capital structure optimization” means in plain terms: companies don’t just use on-balance-sheet cash—they strategically combine low-cost debt. As long as the long-term returns from borrowed capital exceed interest costs, debt becomes not a liability, but a lever to enhance capital efficiency.

AA Rating Turns Bonds into AI Munitions

NVIDIA can execute this strategy only if the bond market is willing to lend at sufficiently low costs—and the key variable enabling this is credit rating.

S&P Global Ratings recently upgraded NVIDIA’s credit rating to AA, citing competitive advantages driven by AI demand, robust cash generation, and a sound balance sheet. An AA rating functions as a high-credit label in the bond market: investors perceive minimal default risk and thus accept lower spreads and longer maturities.

This point is critical. Bond issuance carries more than just “raising capital”—its true value hinges on “at what cost, for how long, and under what market conditions.” When a company is in an upward credit trajectory, experiencing rapid cash flow expansion, and benefiting from sustained institutional interest in the AI theme, its bargaining power for long-term funding increases significantly.

This explains why NVIDIA is acting now—not waiting until cash flow weakens or expansion pressures mount, but instead locking in favorable financing terms while its credit quality is most widely recognized. For shareholders, this preemptive action is far more attractive than being forced to raise capital under worse conditions later.

The intended uses of bond proceeds—refinancing, AI data centers and infrastructure, R&D, supply chain prepayments, strategic investments—also merit collective analysis. Refinancing relates to financial management; infrastructure and supply chain support expansion resilience; strategic investment targets ecosystem positioning. Together, they signal a fundamental shift: NVIDIA’s capital needs are no longer just about “producing more chips,” but about maintaining dominance across the entire AI ecosystem.

NVIDIA sells the most essential compute tools of the AI era—but it must also ensure its customers, supply chain, infrastructure, and ecosystem partners can keep pace. The more central its role becomes, the more its capital allocation resembles that of a platform company, not merely a hardware vendor.

Borrowing Is More Shareholder-Friendly Than Equity Issuance

For NVDA shareholders, this bond issuance carries a direct implication: the company is preserving shareholder returns while reserving ammunition for long-term expansion.

NVIDIA’s most recent quarter delivered not only strong cash flow but also an additional $80 billion buyback authorization and a dividend hike. Buybacks and dividends represent direct cash returns to shareholders; bond issuance represents external, long-term funding supporting future investments. Together, they signal not a trade-off, but a dual-track strategy: rewarding existing shareholders while sustaining momentum in AI expansion.

If NVIDIA had opted for equity issuance, existing shareholders would face dilution. Even if the company continues growing, each share’s earnings and book value would be diluted. In contrast, debt financing entails clearer, fixed costs—interest and principal repayments. For a company with exceptional FCF and top-tier credit ratings, these costs are far more manageable.

Naturally, this doesn’t mean bond issuance is always positive. Debt adds fixed obligations and raises scrutiny on capital allocation efficiency. NVIDIA’s ability to gain investor acceptance today rests on confidence that its future cash flows will comfortably cover interest payments—and that AI infrastructure investments will ultimately translate into revenue and profit. Should either assumption falter, debt shifts from an efficiency tool to a valuation headwind.

Thus, the real change brought by this issuance is how investors view NVIDIA. Previously, the focus was on GPU demand, gross margins, and revenue growth; now, attention turns to cash allocation: how much goes to buybacks and dividends, how much funds supply chain and infrastructure, how much fuels ecosystem investment, and how much is locked in via debt ahead of time.

This complicates NVDA’s valuation anchor. It is no longer just a “profit growth story”—it increasingly exhibits traits of a “credit asset” and a “long-term capital allocation platform.”

An AI Financing Template for Big Tech Is Taking Shape

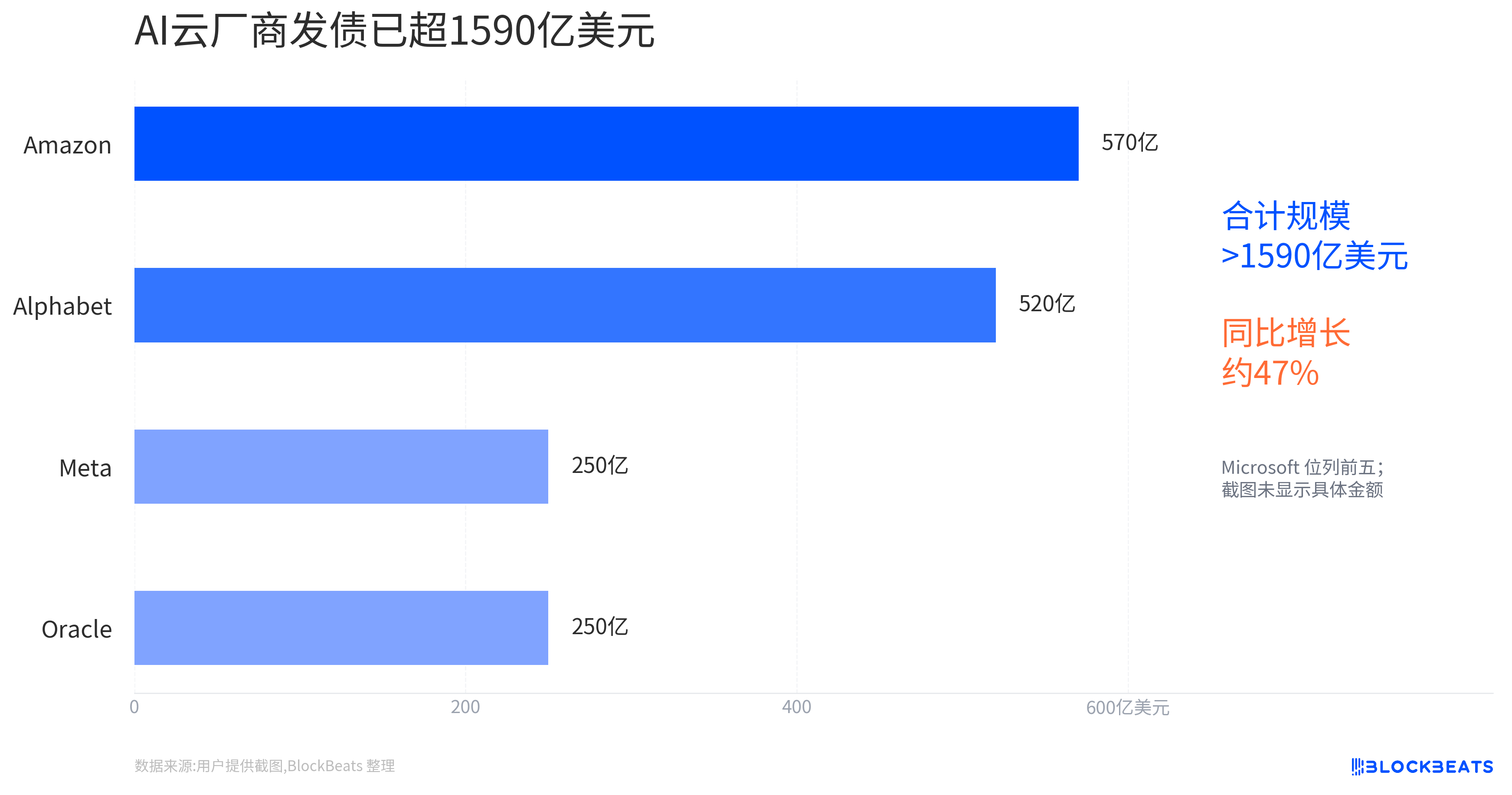

NVIDIA is not alone in this approach. Alphabet completed a $20 billion bond offering in February 2026, with maturities spanning multiple tranches, reportedly attracting orders exceeding $100 billion. Meta, Amazon, and other major tech firms are also using debt financing to support infrastructure spending amid their AI investment cycles.

These cases cannot be reduced to “tech giants are running out of money.” A more accurate interpretation is that AI infrastructure has evolved from a light-asset software growth story into a capital-intensive cycle involving data centers, power grids, semiconductors, networks, and supply chains. Companies that secure funding at lower costs and longer tenors will gain greater flexibility in this expansion race.

This has two implications for market pricing.

First, debt financing extends the sustainability of AI capex. As long as bond markets remain willing to participate, large tech firms need not rely entirely on current operating cash flows to fund long-term construction. This supports demand expectations across data centers, power, optical communications, and semiconductor supply chains.

Second, debt financing sharpens investor focus on return timelines. Previously, markets accepted high valuations for AI investments due to explosive growth rates. But as capital intensity rises and financing terms lengthen, the central question shifts: when will these infrastructures generate sufficient returns? If AI application-side revenue lags expectations or unit compute economics deteriorate, markets will reevaluate whether such debt-financed expansion is overly aggressive.

NVIDIA’s distinctiveness lies in its upstream position within the AI capex chain. The more clients invest, the more NVIDIA benefits. Yet if the industry-wide investment return comes under scrutiny, NVIDIA cannot fully insulate itself. Thus, this bond issuance both reinforces market confidence in NVIDIA’s credit and cash flow—and embeds it deeper into the long-cycle AI capital expenditure narrative.

The True Test Lies in Pricing and Returns Coexisting

One crucial caveat remains: this is still a proposal to issue at least $20 billion. Final size, coupon rates, spread levels, and order book strength are pending confirmation. Only after execution can the market accurately assess how low a cost and how long a tenure bond investors are willing to offer NVIDIA.

If final pricing reflects strong demand and persistently low long-term spreads, it will further validate NVIDIA’s ability to convert its AA credit into a growth lever. It will not only profit from customer AI spend, but also finance its own long-term positioning at a lower cost in capital markets.

But the more important validation comes not from the bonds themselves, but from subsequent earnings reports and capital expenditure data. Investors must see whether NVIDIA can sustain strong free cash flow while advancing AI infrastructure, supply chain prepayments, ecosystem investment, and shareholder returns. If all these elements can coexist, bond issuance acts as a capital efficiency amplifier.

Conversely, if future AI infrastructure ROI timelines lengthen—or if the company increasingly relies on external financing to maintain expansion—the market’s perception of such debt will shift. Then the question will no longer be “Does NVIDIA have enough cash?” but “Are the returns from long-cycle AI investments sufficient to justify the high expectations already priced in via low-cost capital?”

Original: BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

Pharos Network Unlocks AI Model Payment Channels, Introduces New Use Cases for $PROS and USDC as Platform Payment Instruments

6 days ago

Will Claude Ban Accounts and Verify ID Cards? Face Recognition Was Old News from Two Months Ago, and "Handing Over Data to Police" Is a Misinterpretation

6 days ago

Japan's Central Bank on the Brink of Rate Hike—Can the AI Bull Run Withstand?

6 days ago

5-Second Breakthrough with Just 1 Interaction: Has the "Strongest Security Mechanism" of Claude Fable 5 Been Cracked by a Chinese Team?

8 days ago

Why Is the "AI Service Subscription Model" Inevitably Headed for Extinction?

8 days ago

Managing a company valued at nearly a trillion dollars, Anthropic's CEO has only one direct report.

9 days ago

ERC-8126: A New Ethereum Standard for Issuing "Security Health Reports" to AI Agents

9 days ago