ChainThink

Stay ahead, master crypto insights

ETH New Whale: Why Are We Betting on SBET?

ETH New Whale: Why Are We Betting on SBET?

2025-07-16 09:18

Original source: Primitive Ventures

Written by: Yetta (Investment Partner at Primitive Ventures) & Sean (Liquidity Partner at Primitive Ventures)

We are thrilled to announce our participation in the $425 million PIPE (Private Investment in Public Equity) transaction for SharpLink Gaming, Inc. (Nasdaq: SBET). This investment provides us with a differentiated exposure, both by participating in an enterprise treasury management solution based on the Ethereum protocol and by offering a structure that combines option flexibility with long-term capital appreciation potential. This investment reflects our strong confidence in Ethereum's important role in the U.S. capital market and further supports our core belief that crypto assets will be integrated into the mainstream financial system.

Why We Invested

ETH vs. BTC: The Divide of Productive Value

ETH has the inherent yield capability in staking and DeFi ecosystems, making it a true productive asset, whereas Bitcoin lacks such mechanisms. The BTC model represented by MicroStrategy relies more on debt financing to purchase coins, with no income generated from the underlying asset, resulting in higher leverage risks. SBET, on the other hand, is expected to directly utilize ETH's on-chain mechanisms for compounding growth, delivering real, quantifiable returns to shareholders.

Currently, no ETH staking ETF has been approved by regulators, so traditional markets cannot directly access the yield layer of ETH. We believe that SBET is an innovative way to achieve this path. With Consensys' cooperation, it is expected to operate protocol-based strategies that can generate considerable on-chain returns, potentially surpassing future ETH staking ETFs.

Additionally, ETH's implied volatility (69) is significantly higher than BTC's (43), creating higher option value for convertible arbitrage and structured derivatives, turning volatility into a tradable asset rather than pure risk.

Consensys' Strategic Participation

We are honored to collaborate with Consensys in this $425 million PIPE investment. Consensys is the strongest force driving Ethereum commercialization. Its technical strength, product ecosystem, and operational scale are key drivers for SBET becoming an Ethereum-native enterprise carrier.

Consensys was founded by Ethereum co-founder Joe Lubin in 2014, dedicated to transforming Ethereum's open-source foundation into scalable real-world applications—from the Ethereum Virtual Machine (EVM), zkEVM (Linea), to MetaMask, which helps millions of users access Web3. To date, Consensys has raised over $700 million in funding from top-tier investors like ParaFi and Pantera, and has an excellent track record in strategic acquisitions, making it one of the most deeply embedded operational entities in the Ethereum ecosystem.

Joe Lubin's appointment as chairman is not just symbolic. As one of the architects of Ethereum's core design and one of the key leaders of the most critical infrastructure companies in the ecosystem, Joe has comprehensive insights into Ethereum's product roadmap and asset mechanisms. His early experience on Wall Street also gives him the financial market literacy needed to guide SBET into institutional-level financial frameworks.

On SBET, we see a unique combination of an asset and the most capable investors. This synergy is forming a powerful positive flywheel: protocol-native treasury strategies driven by protocol-native leadership. Under Consensys' leadership, we believe SBET has the potential to become a flagship example of how Ethereum's productive capital can be institutionalized and scaled within the traditional capital market.

Market Valuation Comparison and Analysis

To further understand SBET's opportunities, we attempted an analysis of valuation dynamics from different encrypted treasury strategies.

MicroStrategy: Pioneers of Crypto Asset Strategies

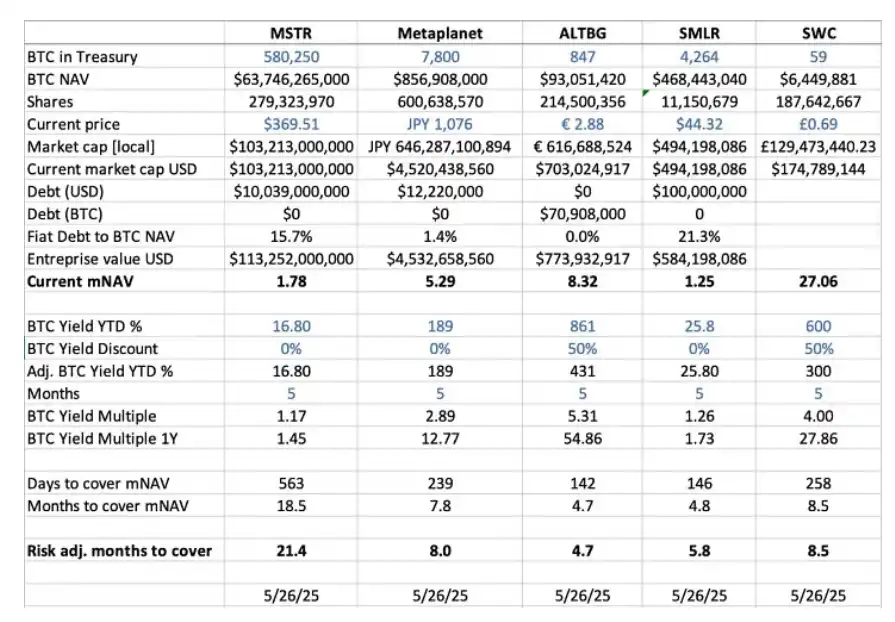

MicroStrategy has set an industry benchmark for encrypted treasury strategies. As of May 2025, it has accumulated 580,250 Bitcoins, with a market value of approximately $63.7 billion. MSTR's strategy involves increasing BTC through low-cost debt and equity financing. This model has inspired many companies to follow, validating the feasibility of encrypted assets as reserve assets.

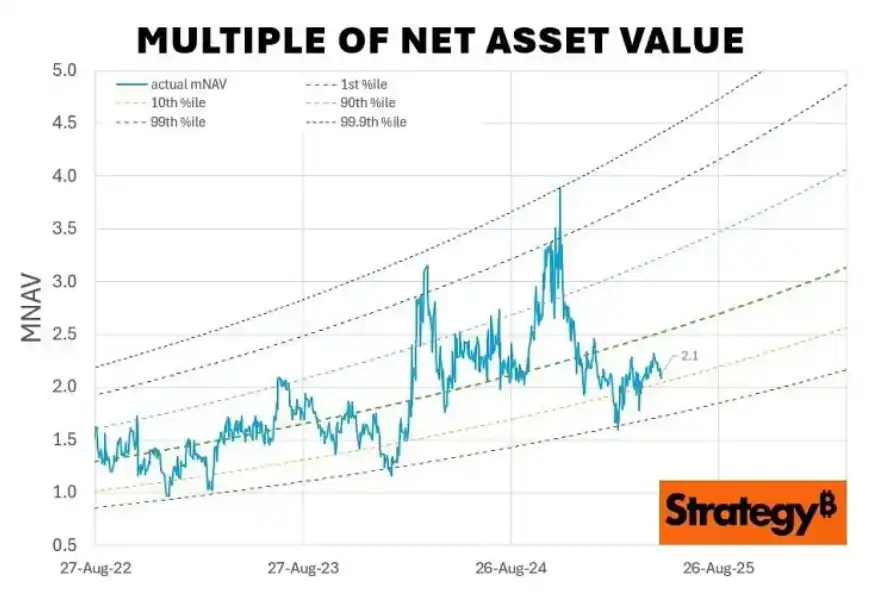

As of May 2025, MSTR's market cap was about 1.78 times its Bitcoin net asset value (mNAV), highlighting the strong demand from investors for leveraged exposure to encrypted assets through listed stocks. This premium comes from the叠加 of three factors: leveraged growth potential, index inclusion eligibility, and a more convenient investment path compared to direct coin holding.

Looking back, MSTR's mNAV multiple fluctuated between 1x and 4.5x between August 2022 and August 2025, reflecting how market sentiment drives valuation. The high points (e.g., 4.5x) typically occurred during Bitcoin bull cycles and large-scale BTC accumulation periods by MSTR, showing strong investor enthusiasm; while the low points at 1x corresponded to market consolidation periods, revealing the cyclical nature of investment confidence.

Comparative Analysis of Peers

We conducted a horizontal comparative analysis of several publicly listed companies that have adopted encrypted treasury strategies:

· BTC Net Asset Value (NAV): the total USD value of the company's held Bitcoin assets. MicroStrategy ranks first with 580,250 BTC (approximately $6.37 billion); followed by Metaplanet (7,800 BTC, $857 million), SMLR (4,264 BTC, $468 million), ALTBG (847 BTC, $93 million), and SWC (59 BTC, $6.4 million).

· mNAV Multiple (Market Cap / BTC NAV): the multiple of the company's market cap to its BTC NAV, reflecting its trading premium. SWC has the highest premium at 27.06 times, mainly driven by limited BTC holdings and market sentiment; ALTBG (8.32 times) and Metaplanet (5.29 times) also maintain a high premium; while MSTR (1.78 times) and SMLR (1.25 times) have relatively moderate premiums due to larger size and higher leverage.

· BTC Year-to-Date Return (YTD%): the rate of return per share of BTC, adjusted for dilution. Small-cap companies often show higher unit output efficiency due to more aggressive BTC accumulation actions, for example, ALTBG reached 431%, and SWC reached 300%. These data provide important clues for investors regarding capital efficiency and compounding ability.

· Time Required for mNAV Convergence (Months): the time required for the company to accumulate enough BTC to reach the NAV level implied by its current market cap, calculated based on the current BTC growth rate. Assuming an annual BTC return, ALTBG and SMLR could theoretically achieve valuation convergence within 5 months, providing arbitrage space for NAV compression trades and relative pricing errors.

Risk Factors: the debt ratio of MSTR and SMLR to NAV is 15.7% and 21.3% respectively. When BTC prices fall, they are more vulnerable to impact. While ALTBG and SWC have no leverage, they have stronger risk resistance.

Case Study of Japanese Metaplanet: An Observation of Valuation from a Macro Market Perspective

Valuation differences often stem from differences in asset reserves and capital allocation structures, but regional capital market dynamics are equally critical, directly affecting asset pricing. Metaplanet's case is highly representative—it is often referred to as the "Japanese version of MicroStrategy."

The high valuation premium of Metaplanet comes not only from its held Bitcoin assets but also from the structural advantages brought by Japan's local market regulations:

NISA System Dividends: Japanese retail investors are buying Metaplanet stock in bulk through NISA (Japan Individual Savings Account). This system allows individuals to enjoy up to approximately $25,000 in capital gains tax-free, significantly enhancing the tax attractiveness of stock allocations compared to directly holding BTC, which requires paying up to 55% in capital gains taxes. According to data from SBI Securities, Metaplanet was the most purchased stock in NISA accounts in the week before May 26, 2025, and its stock price surged by 224% in the past month.

Structural Dislocation in Japan's Debt Market: Japan's debt level is as high as 235% of GDP, and the 30-year Japanese government bond yield has risen to 3.20%, indicating significant structural pressure in the bond market. In this context, investors increasingly view Metaplanet's 7,800 BTC as a hedging tool to hedge against yen depreciation and domestic inflation risks.

SBET: Aiming for Cross-Market Dominance

In the public market, regional capital flows, tax structures, investor psychology, and macroeconomic conditions often hold equal importance to the underlying asset itself. To uncover asymmetric investment opportunities at the intersection of encrypted assets and traditional markets, it is essential to deeply understand the institutional details and market behaviors of different jurisdictions.

As the first listed vehicle built around Ethereum capital, SBET is in a unique position to leverage "jurisdictional arbitrage" strategies to amplify its first-mover advantage. We believe SBET can further consolidate its leadership, for example, by achieving dual listings on the Hong Kong Stock Exchange (HKEX) or the Tokyo Stock Exchange (Nikkei), to unlock regional liquidity in Asia and protect against valuation dilution caused by narrative shifts.

Through this cross-market layout, SBET has the potential to become a truly global Ethereum-native (ETH-native) listed entity, not only symbolically significant but also institutionally compliant and accessible to institutional investors, serving as a representative new type of crypto financial instrument in the global capital market.

Institutionalization of Crypto Capital Structure

The integration of CeFi (Centralized Finance) and DeFi (Decentralized Finance) marks the maturation of the crypto market, and also means that this emerging asset class is rapidly embedding itself into a broader financial system. In a sense, this trend is pushing "crypto finance" towards "institutional finance."

On one hand, protocols like Ethena and Bouncebit represent a new paradigm of CeDeFi: integrating centralized components with on-chain mechanisms to expand the applicability and accessibility of encrypted assets, providing more friendly channels for institutional participants.

On the other hand, the linkage between encrypted and traditional capital markets reflects a deeper evolution of macro financial structures: encrypted assets are gradually evolving from fringe assets into "institutionalizable asset classes." This institutionalization path has gone through three stages, each representing a leap in structure and financial engineering:

· GBTC: Original Institutional Access but Rigid Structure

As one of the earliest compliant exposures for BTC, GBTC provides market access within the regulatory framework, but due to the lack of redemption mechanisms, its price has long deviated from net asset value. This stage reveals the structural limitations of traditional financial instruments in the era of crypto.

· Spot Bitcoin ETF: Liquidity Revolution but Passive

Since its approval by the SEC in January 2024, the spot BTC ETF introduced daily subscription/redemption mechanisms, allowing NAV to be closely anchored, significantly improving institutional participation thresholds and market efficiency. However, its passive management attributes limit its ability to capture on-chain yields and active value creation of encrypted assets, which is its natural return ceiling.

· Corporate Treasury Strategies: Rise of Active Yield Paradigm

MicroStrategy, Metaplanet, and now SharpLink are incorporating encrypted assets into corporate treasury systems, no longer limited to "holding," but through on-chain staking, yield compounding, tokenized financing, and on-chain cash flow design, redefining capital efficiency and shareholder return models. This stage is a key node in institutionalizing and making "encrypted native capital" sustainable.

From the one-way structure of GBTC to the liquidity upgrade of ETFs, and then to the "yield-optimized corporate treasury model" represented by SBET, this evolutionary path demonstrates how encrypted capital structures are gradually being absorbed into the modern financial system, offering higher liquidity, stronger structural design capabilities, and richer value creation paths.

We Maintain a Cautiously Optimistic Stance

Although we are confident in SBET's long-term prospects, we also maintain a clear awareness of potential risks:

Premium Compression Risk: If SBET's stock price remains below its net asset value for a long time, its mechanism of raising funds through new stock issuance may lead to dilution. This situation has already occurred during the prolonged discount phase of GBTC before its transition to ETF.

ETF Cannibalization Risk: If Ethereum spot ETFs gain approval for staking earnings in the future and their management scale continues to grow, investors may prefer them due to their "more straightforward and compliant" path, even if their earning capacity is limited. This "convenience-first" market preference may lead to capital diversion for SBET.

Despite this, we still firmly believe that SBET's ETH-native yield strategy will outperform Ethereum ETFs in the long run, offering investors a configuration opportunity that combines growth and returns.

Final Remarks

Our participation in this $425 million PIPE investment in SharpLink Gaming is based on our deep understanding of Ethereum's transformative potential in the corporate treasury field. With Consensys' technical depth and Joe Lubin's forward-looking leadership, SBET has all the elements to lead the next cycle of "crypto value creation."

As CeFi and DeFi accelerate their integration, encrypted assets will play a more central role in a broader market system. We are proud to participate in and support SBET's vision, and we will continue to resolutely seek out high-potential opportunities that can stand out in this structural transformation.

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

Popular Airdrop Tutorial

Selected potential airdrop opportunities to gain big with small investments

FusnChain

FusnChain