ChainThink

Stay ahead, master crypto insights

The Hidden Gold Mine of Stablecoins: How to Profit from U.S. Treasuries and Interest Rates?

The Hidden Gold Mine of Stablecoins: How to Profit from U.S. Treasuries and Interest Rates?

2025-04-18 23:40

Original Title: How Stablecoins Profit From U.S. Debt & Interest Rates

Original Author: Three Sigma

Original Translation: zhouzhou, BlockBeats

Editor's Note: This article explores how stablecoins like USDT and USDC generate billions in revenue by investing reserves in U.S. Treasury securities, with their profitability closely tied to Federal Reserve interest rates. Should rates drop to zero, their earnings potential could collapse. As demonstrated during the 2023 Silicon Valley Bank (SVB) crisis, fiat-backed stablecoins face regulatory scrutiny and depegging risks, whereas algorithmic stablecoins like USDe rely on crypto-native yields, making them less sensitive to rate fluctuations. Tether’s $20 billion equity provides decades of runway, but Circle’s $1.68 billion revenue in 2024 and limited liquidity render it vulnerable with only 18–25 months of sustainability.

Below is the original content (edited for readability):

1. The Shift Toward Stability in Cryptocurrency

Initially, Bitcoin was envisioned as a substitute for traditional money—a decentralized, borderless, censorship-resistant form of currency. However, due to its high volatility, evolving into a speculative asset and store of value, along with elevated blockchain transaction costs, it became increasingly unsuitable as a daily payment instrument or a stable store of value.

This limitation catalyzed the rise of stablecoins. Designed to maintain fixed value—typically pegged to the U.S. dollar—stablecoins offer the transactional stability and efficiency that Bitcoin lacks.

The evolution of the crypto ecosystem reflects a pragmatic shift. While Bitcoin originally aimed to replace traditional money, the demand for stability has led to widespread adoption of stablecoins—usually backed by traditional assets—becoming foundational pillars of the entire digital economy.

These stablecoins serve as bridges between traditional financial markets and the crypto ecosystem, promoting cryptocurrency adoption while raising questions about the ideal of decentralization. For instance, stablecoins like Tether (USDT) and USD Coin (USDC), issued by centralized entities and backed by deposits held in traditional banks, represent a compromise between ideological principles and practical realities.

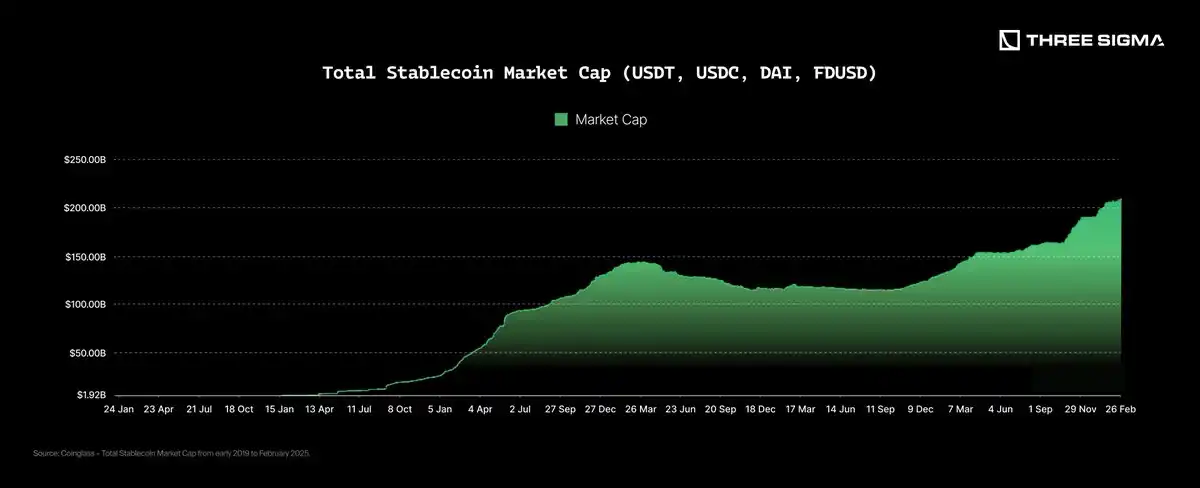

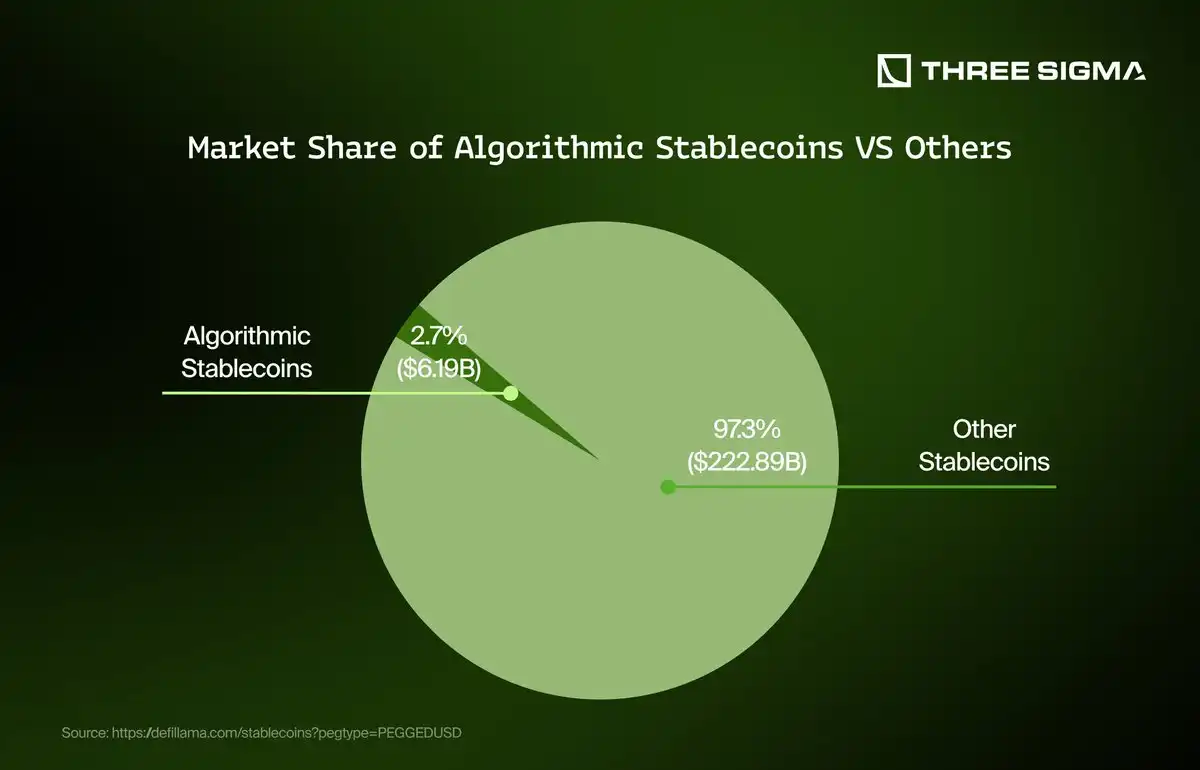

Over the years, stablecoin adoption has surged dramatically. In 2017, their total market cap was under $3 billion, but by March 2025, it had grown to approximately $228 billion. Stablecoins now account for about 8.57% of the total crypto market and serve as essential tools for trading, cross-border payments, and safe-haven strategies during market turbulence.

This growth trend underscores the pivotal role stablecoins play as connectors between traditional finance and the crypto world. A chart from Coinglass clearly illustrates the steady and substantial increase in market capitalization of major stablecoins since early 2019.

What Are Stablecoins?

Stablecoins are cryptocurrencies designed to maintain price stability by pegging their value to an external asset—such as fiat currency or commodities. For example, Tether (USDT) and USD Coin (USDC) are both pegged to the U.S. dollar at a 1:1 ratio. The goal of stablecoins is to combine the advantages of digital currencies—such as fast, borderless transactions on blockchains—without the extreme price volatility associated with Bitcoin.

Stablecoins strive to maintain price stability through holding reserve assets or employing other mechanisms, making them better suited as everyday transaction tools or stores of value within the crypto market. In practice, most mainstream stablecoins achieve price stability via collateralization mechanisms—meaning each issued stablecoin must be backed by an equivalent amount of reserve assets.

To ensure stability and credibility, clear regulation is essential. Currently, the U.S. lacks comprehensive federal legislation, relying instead on state-level rules and pending legislative proposals; the EU enforces strict reserve and audit requirements under the MiCA framework; Asia exhibits diverse regulatory approaches: Singapore and Hong Kong enforce stringent reserve requirements, Japan permits bank-issued stablecoins, while China effectively bans all stablecoin-related activities. These differences reflect varying trade-offs between "innovation" and "stability."

Despite the absence of a global regulatory framework, stablecoin usage and adoption continue to grow steadily year after year.

Why Are They Issued?

As previously discussed, the initial purpose of stablecoins was to provide users with a reliable digital asset for payments or as a value storage mechanism tied to a major global currency—particularly the U.S. dollar. However, their issuance is not altruistic but represents a highly profitable commercial opportunity, with Tether being the first company to recognize and exploit this potential.

Tether launched USDT in 2014, becoming the first stablecoin and pioneering an extremely lucrative business model—especially from a per-unit profit perspective, one of the most successful projects in history. Its business logic is straightforward: Tether issues 1 USDT for every dollar received, and destroys the corresponding USDT when users redeem dollars. The received dollars are then invested in secure short-term financial instruments (like U.S. Treasuries), generating profits that accrue entirely to Tether.

Understanding how stablecoins generate revenue is key to grasping their underlying economic mechanics.

Although the business model appears simple, Tether cannot control its primary revenue source—the interest rates set by central banks, particularly the Federal Reserve. High interest rates enable substantial profits for Tether, but low rates drastically reduce profitability.

Currently, the high-interest-rate environment is highly favorable for Tether. But what happens if interest rates fall again, even approaching zero? Will algorithmic stablecoins also be affected by interest rate fluctuations? Which type of stablecoin might perform better under such macroeconomic conditions? This article will further explore these questions and analyze how stablecoin business models adapt to changing macroeconomic environments.

2. Types of Stablecoins

Before analyzing how different stablecoins perform under varying economic conditions, understanding the operational mechanisms of various types is crucial. While all stablecoins share the common goal of maintaining a stable value pegged to real-world assets, each responds differently to interest rate changes and broader market dynamics. Below, we introduce several major stablecoin types, their mechanisms, and their reactions to economic shifts.

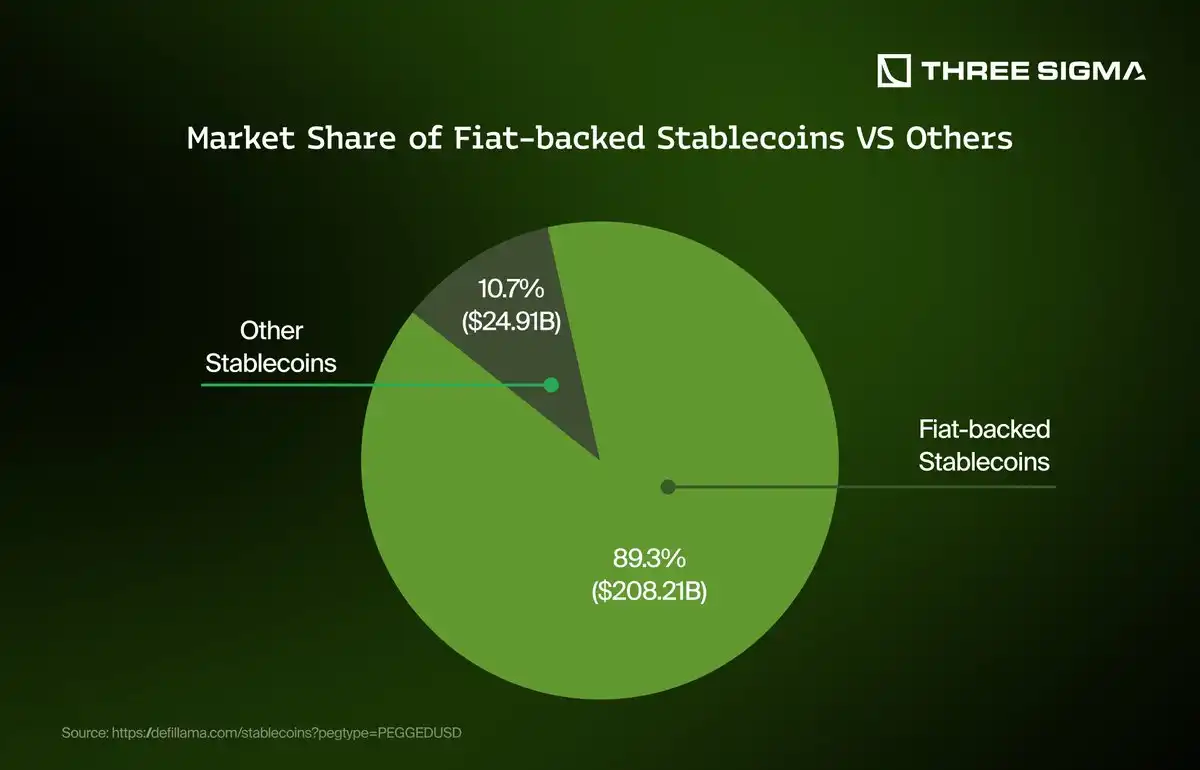

Fiat-Backed Stablecoins

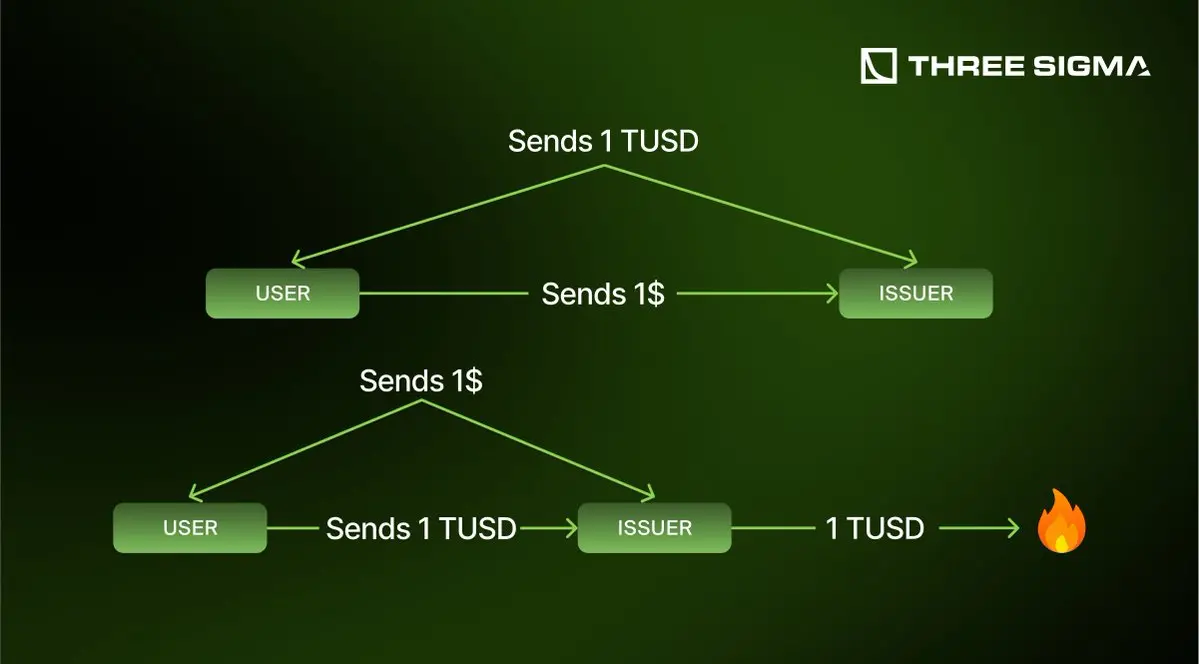

Fiat-backed stablecoins are currently the most well-known and widely used type, essentially representing the tokenization of the U.S. dollar in a centralized manner.

Their operation is straightforward: whenever a user deposits $1, the issuer mints 1 corresponding stablecoin; when the user redeems dollars, the issuer burns the corresponding token and returns an equal amount of cash.

The profit model of fiat-backed stablecoins lies largely behind the scenes. Issuers invest users' deposits into various short-term, secure financial instruments such as treasuries, guaranteed loans, cash equivalents, and occasionally higher-volatility assets like cryptocurrencies (e.g., Bitcoin) or precious metals. The income generated from these investments constitutes the primary revenue stream for the issuer.

However, high returns come with significant risks. One persistent challenge is regulatory compliance. Many governments scrutinize fiat-backed stablecoins, arguing they function essentially as digital currency issuers and thus must adhere to strict financial regulations.

Although most stablecoin issuers have successfully navigated regulatory pressures without major business disruptions, significant challenges persist. A notable example is Europe’s MiCA (Markets in Crypto-Assets) regulation, which recently barred USDT (Tether) from circulation in certain markets due to non-compliance with its stringent regulatory requirements.

Another major risk is “depeg risk.” Issuers typically place large portions of their reserve assets into various investment vehicles. If a large number of users simultaneously request redemption, the issuer may need to sell these assets quickly, potentially leading to significant losses. This scenario could trigger a chain reaction akin to a bank run, making it difficult to maintain the coin’s peg to the dollar—and potentially resulting in bankruptcy.

The most prominent case occurred in March 2023 involving USDC (issued by Circle). When Silicon Valley Bank (SVB) collapsed, rumors spread rapidly that Circle held significant reserves at SVB, sparking market concerns about Circle’s liquidity and USDC’s ability to maintain its peg. These fears led to a temporary depegging of USDC. This event highlighted the risks inherent in holding stablecoin reserves at centralized banks. Fortunately, Circle resolved the issue within days, restored market confidence, and re-established USDC’s peg.

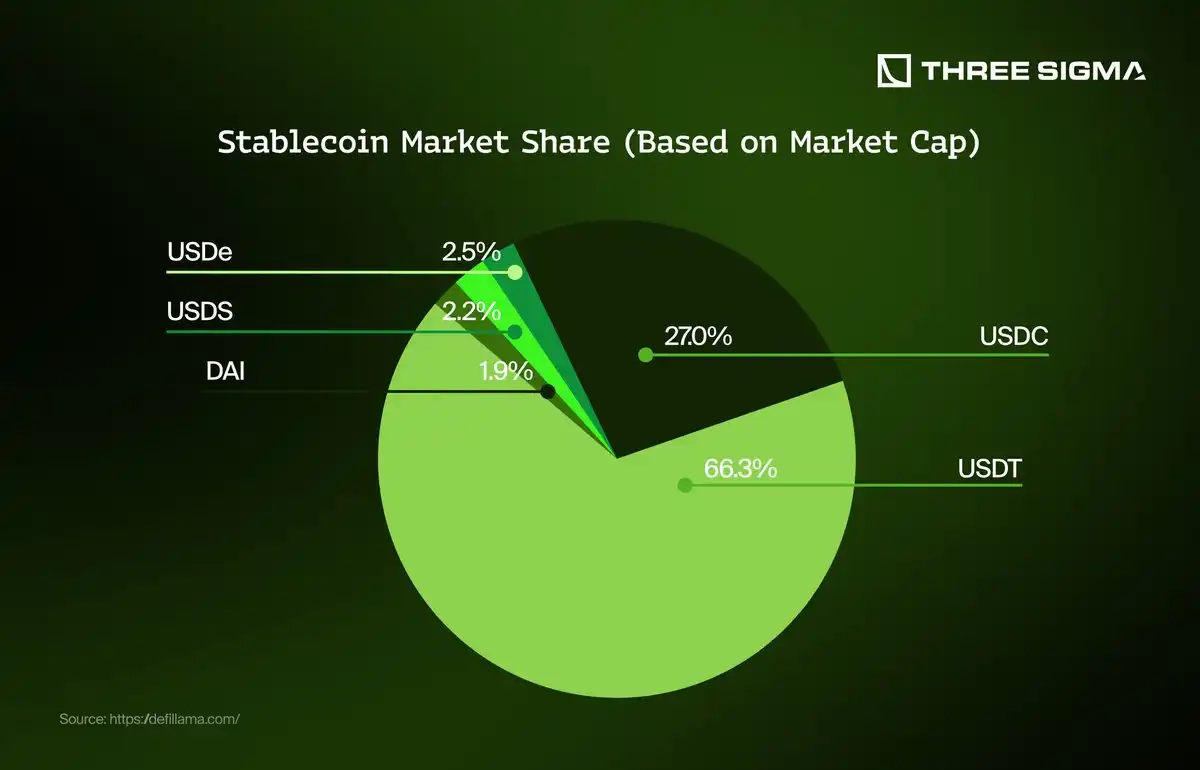

Currently, the two dominant fiat-backed stablecoins in the market are USDT (Tether) and USDC (Circle).

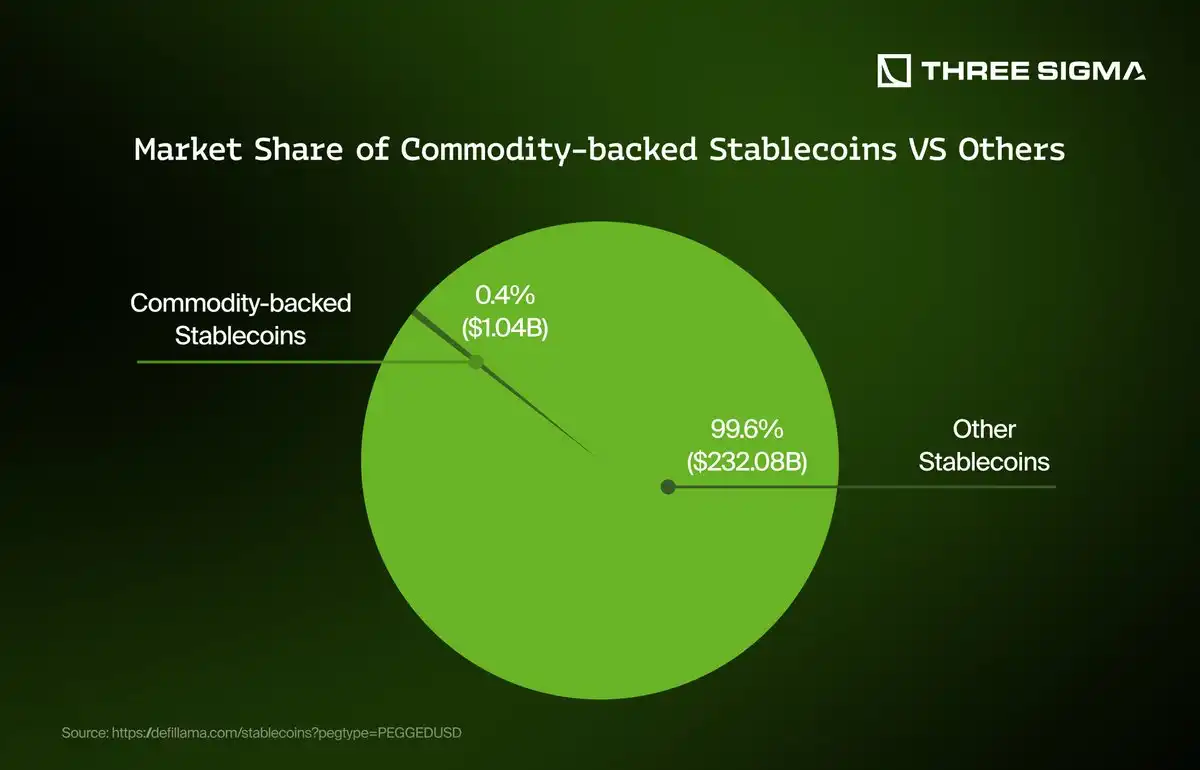

Commodity-backed stablecoins are an innovative category within the stablecoin ecosystem, issuing digital tokens backed by tangible physical assets—typically precious metals like gold and silver, or commodities such as oil and real estate.

Their operational mechanism resembles that of fiat-backed stablecoins: for every unit of physical commodity deposited, the issuer mints an equivalent digital token. Users can typically redeem these tokens for the physical commodity itself or for equivalent cash, at which point the corresponding token is destroyed.

The issuer’s revenue sources primarily stem from fees charged during token creation (minting) and redemption (burning). For example, Pax Gold (PAXG) charges small fees for minting and burning tokens, although Paxos currently does not charge storage fees for the gold it holds. Additionally, issuers may earn revenue by providing services for exchanging and converting tokens between dollars and physical commodities.

Similarly, Tether Gold (XAUT) earns revenue from fees related to redemption and delivery. Users who redeem XAUT tokens for physical gold bars or convert gold into cash through Tether are charged fees. For instance, a fee of 25 basis points (0.25%) is applied during redemption, and additional shipping fees apply for physical delivery. If users choose to sell the redeemed gold bars in the Swiss market, an extra 25 basis points fee is incurred.

Nevertheless, these stablecoins also face risks, especially the volatility of commodity prices themselves, which can impact the stablecoin’s pegged value. Moreover, compliance remains a significant challenge. Commodity-backed stablecoins are typically subject to rigorous regulatory requirements and must have transparent and secure custody arrangements.

Currently successful commodity-backed stablecoins include Paxos’ Pax Gold (PAXG) and Tether’s Tether Gold (XAUT), both backed by gold reserves, offering investors convenient digital exposure to physical commodities.

In summary, commodity-backed stablecoins bridge traditional commodity investing with digital finance, offering stability and exposure to tangible assets, while emphasizing regulatory compliance and transparency.

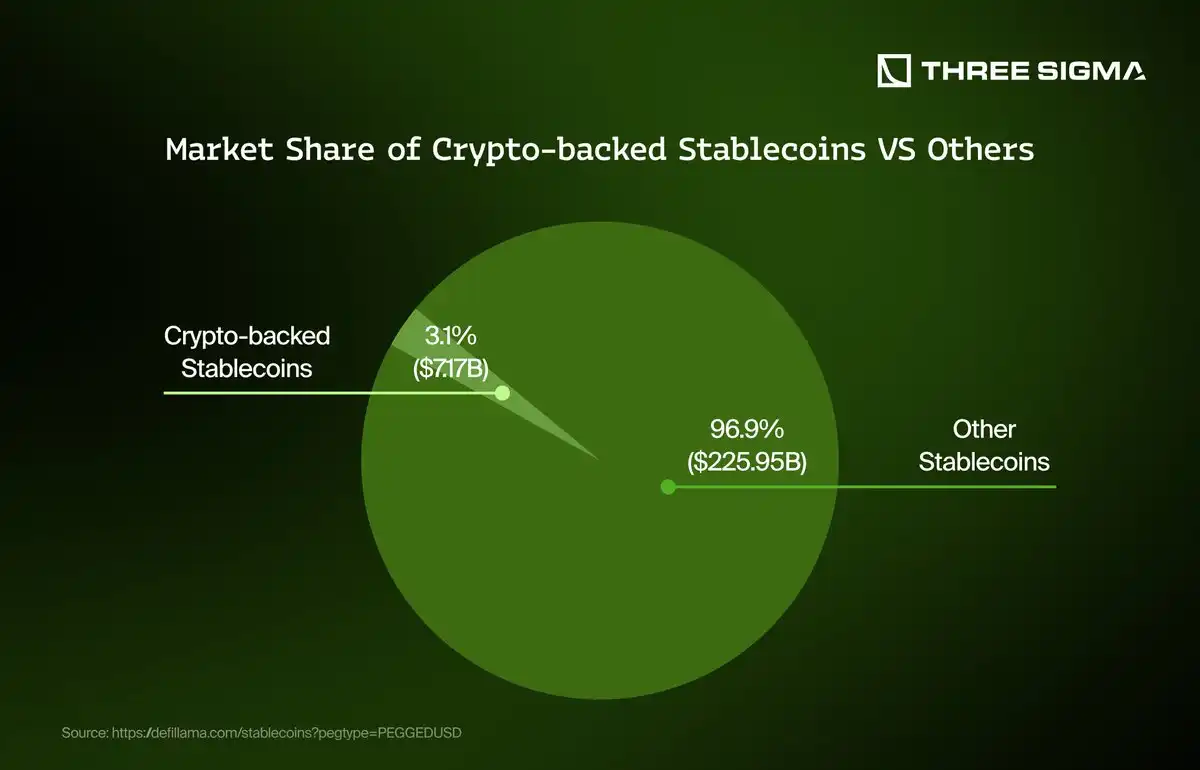

Crypto-asset-backed stablecoins are a significant category within the stablecoin ecosystem, maintaining a stable value pegged to a fiat currency—typically the U.S. dollar—by using cryptocurrencies as collateral. Unlike fiat- or commodity-backed stablecoins, these tokens rely on smart contract technology to build a transparent and automated system.

The basic mechanism is: users lock up crypto assets (usually over-collateralized) in a smart contract to mint stablecoins. The over-collateralization design buffers against price volatility of the underlying crypto assets, ensuring the stablecoin maintains its target peg. When users redeem stablecoins, they return an equivalent amount, the system burns the tokens, and releases the original collateralized crypto assets.

The revenue model for crypto-asset-backed stablecoins includes:

Interest charged on users borrowing stablecoins;

Liquidation fees collected from users whose collateral falls below the liquidation threshold;

Governance rewards set within the protocol to incentivize token holders and liquidity providers.

DAI (now known as USDs), issued by MakerDAO (renamed SKY), is a prime example, primarily using crypto assets from the Ethereum ecosystem as collateral. MakerDAO’s revenue streams include stable fees (interest) charged to borrowers of USDs and penalties collected upon liquidation. These fees collectively sustain the protocol’s operation and long-term viability.

Another example is HONEY, a stablecoin issued by Berachain, currently collateralized by USDC and pYUSD. HONEY’s revenue comes from redemption fees: users pay a 0.05% fee when redeeming HONEY and retrieving their collateral (USDC or pYUSD).

Although classified as “crypto-asset-backed,” most of these stablecoins are essentially wrapped versions of fiat-backed stablecoins, like USDC. While the initial goal was to fully rely on native crypto assets for stability, in practice, achieving true stability without depending on fiat stablecoins remains extremely difficult.

Of course, these assets carry inherent risks. For example, volatility in the underlying crypto assets can pose major challenges—such as massive liquidations during sharp downturns, potentially breaking the stablecoin’s peg. Additionally, smart contract vulnerabilities or protocol attacks can severely threaten the entire system’s stability.

In summary, crypto-asset-backed stablecoins like USDs and HONEY play a vital role in providing decentralized, transparent, and innovative financial solutions. However, despite their nominal crypto collateralization, they often heavily depend on fiat stablecoins in practice, necessitating more robust risk management mechanisms to ensure their resilience and credibility.

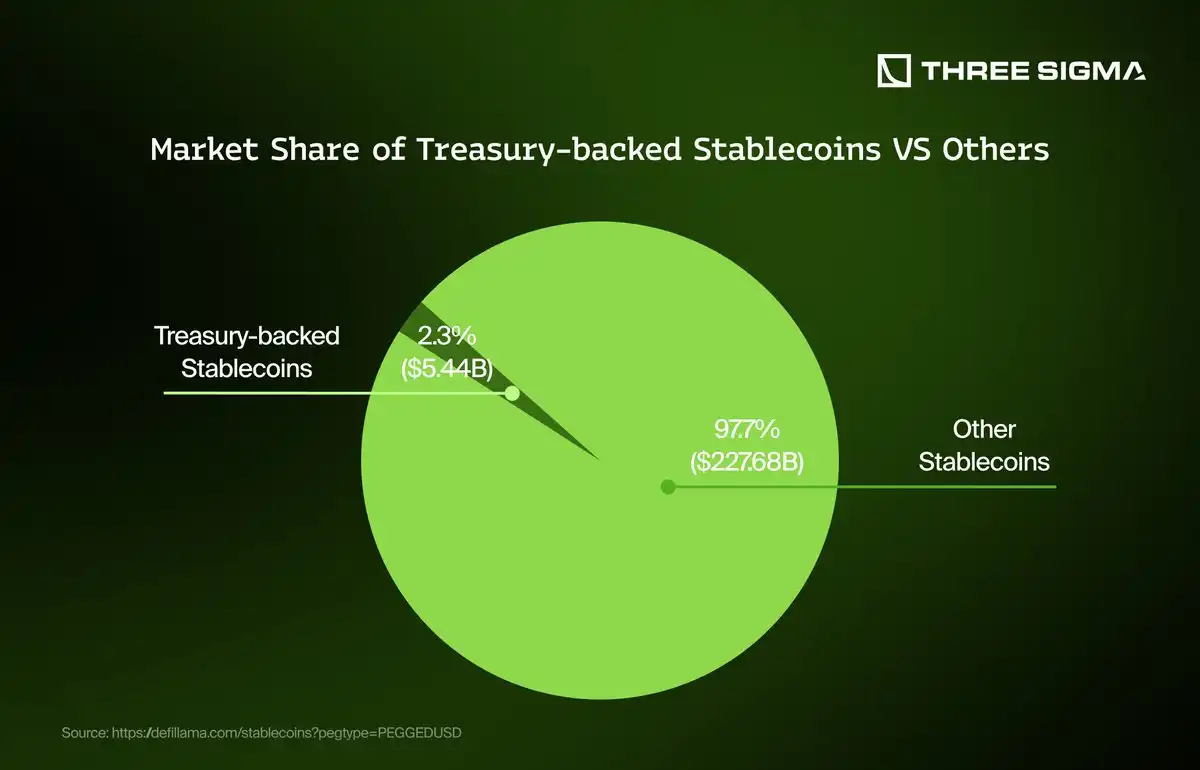

Treasury-backed stablecoins are a class of stablecoins supported by government bonds—particularly U.S. Treasuries. Typically pegged to the U.S. dollar, these stablecoins offer value stability while generating passive income from the interest earned on underlying Treasury securities, making them more akin to yield-bearing investment instruments that blend the stability of traditional stablecoins with the characteristics of financial instruments.

For example, Ondo’s USDY (Dollar Yield Token) is a tokenized note backed by short-term U.S. Treasuries and bank demand deposits. Its goal is to provide non-U.S. individuals and institutions with the convenience of a stablecoin while delivering high-quality, dollar-denominated yield. After purchasing USDY, funds are used to buy U.S. Treasuries and part of the proceeds are placed in banks, with interest distributed proportionally to token holders. USDY is a “yield-bearing asset” (bearing asset), meaning its value grows passively over time as interest accumulates from the underlying assets.

Another example is Hashnote’s USYC (Dollar Yield Coin), the on-chain representation of Hashnote’s Short-Term Yield Fund (SDYF), investing in short-term U.S. Treasuries and participating in repurchase and reverse-repurchase markets. USYC’s returns are tied to short-term “risk-free rates,” while leveraging blockchain speed, transparency, and composability, minimizing protocol, custody, regulatory, and credit risks. Users can convert USYC to USDC or PYUSD on the same day (T+0) or the next day (T+1), with atomic and instant on-chain minting. Like USDY, USYC is a “yield-bearing asset,” accumulating returns passively through interest generated by the underlying assets.

Although these stablecoins offer dual advantages of stability and yield, they also carry certain risks:

· Regulatory risk: Since these assets typically target non-U.S. users to avoid U.S. regulatory requirements, future policy changes could introduce uncertainty;

· Custody risk: Requires reliance on the issuer to properly manage and hold underlying assets;

· Liquidity risk: During periods of severe market volatility, user redemption requests may be restricted;

· Counterparty risk: Particularly in repurchase agreements, default by counterparties could lead to losses;

· Macroeconomic risk: Such as interest rate changes, which could affect overall yield levels.

Such tokens are often categorized into a rapidly growing new class—“Treasury-backed crypto assets.”

Algorithmic stablecoins are a class of stablecoins that rely on economic mechanisms and market incentives rather than full collateralization with fiat or government bonds to maintain a stable value. These models typically use supply-and-demand adjustment mechanisms to maintain a peg (e.g., to the U.S. dollar), but frequently face challenges in extreme market conditions. Their fundamental issue lies in heavy dependence on sustained market confidence and effective incentive structures—both of which can fail under severe stress.

USDe, issued by Ethena, is a novel “pseudo-algorithmic” stablecoin using a hybrid model. It maintains stability through a “delta-neutral hedging mechanism,” holding crypto assets like BTC and ETH as collateral while simultaneously establishing equivalent short positions in derivatives markets to hedge against price volatility of the underlying assets, thereby maintaining a stable peg to the dollar. USDe achieves a 1:1 full collateralization, offering greater capital efficiency compared to over-collateralized models. Additionally, Ethena includes highly liquid stablecoins like USDC and USDT in its reserves to enhance liquidity and the efficiency of its hedging strategy.

Despite multiple innovations, algorithmic stablecoins still face significant risks: market instability, extreme volatility, or liquidity crises can disrupt their peg-maintenance mechanisms. Furthermore, reliance on derivatives introduces counterparty and execution risks, making the system vulnerable to external shocks.

Although new models like USDe attempt to mitigate these issues through structured hedging and diversified reserves, their long-term stability ultimately depends on overall liquidity conditions and the ability to operate effectively under adverse market environments.

3. Current Mainstream Stablecoins

When discussing stablecoins, USDT and USDC are undoubtedly the dominant forces in the market, serving as central pillars of liquidity in the crypto ecosystem. Both share similar structures: issued by centralized entities, fully backed by fiat reserves, and widely integrated across major exchanges and financial platforms.

USDT is issued by Tether and holds the largest market share, renowned for its deep liquidity and broad adoption—especially frequent use in high-frequency trading environments. USDC, issued by Circle, positions itself as a more compliant and transparent option, favored by institutions and enterprises seeking a regulatory-friendly environment. Despite minor differences in details, their core functions remain consistent: providing a stable, trustworthy digital dollar that underpins the entire crypto ecosystem.

In contrast, USDS, DAI, and USDe represent the decentralized force countering fiat-backed stablecoins, though their degree of decentralization varies. DAI and USDS are fundamentally part of the same ecosystem—MakerDAO (now renamed Sky). USDS is a derivative evolution of DAI, a key component of Sky’s long-term strategic vision.

Historically, DAI was more decentralized, relying on over-collateralized crypto assets to maintain its peg. USDS, however, reflects Maker’s shift toward a more structured and strategic direction, prioritizing efficiency over pure decentralization.

Meanwhile, USDe is another significant decentralized stablecoin competitor, but it follows a completely different path. Unlike Maker’s model of over-collateralization and governance mechanisms, USDe introduces a yield-generating structure, using its collateral assets to deliver additional returns to token holders.

USDT

When discussing stablecoins, USDT naturally emerges as the dominant force, playing a central role as a pillar of centralized liquidity in the crypto market. Issued by Tether, USDT holds the largest market share and is renowned for its deep liquidity and wide adoption—particularly critical in high-frequency trading environments. It provides a stable and trusted digital dollar, underpinning the functioning of the entire crypto ecosystem and serving as the primary medium for trading pairs, arbitrage opportunities, and cross-exchange liquidity provision. Its widespread acceptance solidifies its role in both centralized and decentralized finance.

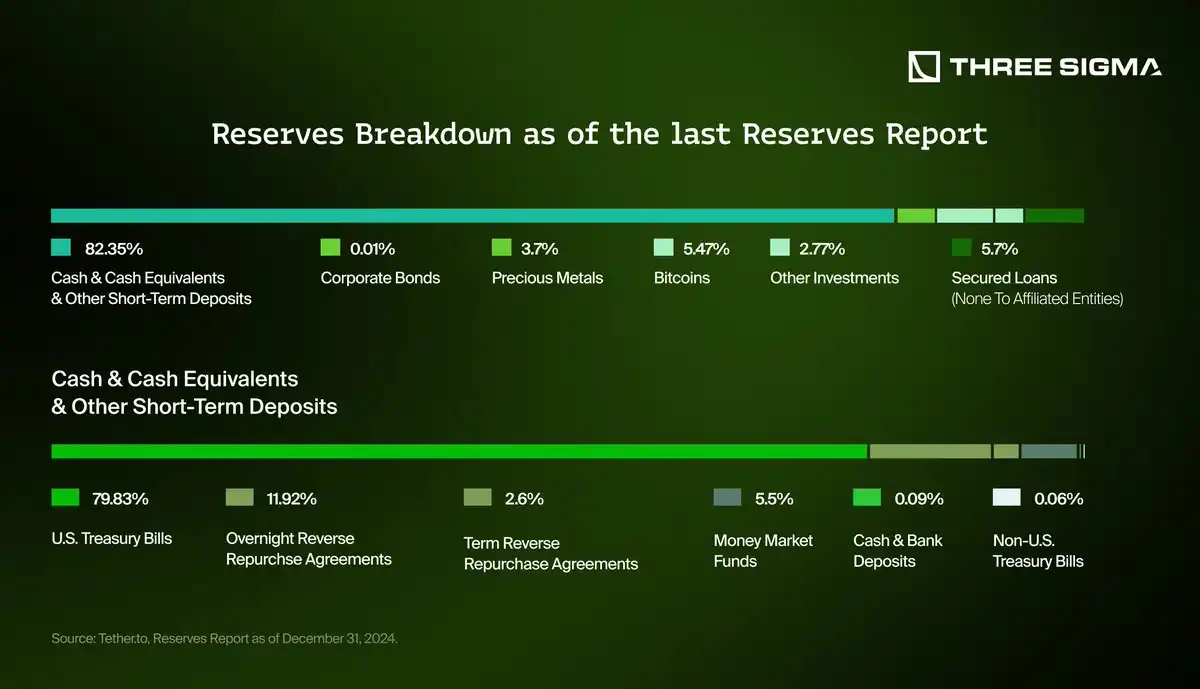

Tether’s revenue primarily stems from managing its vast reserve assets, which back every issued USDT token. These reserve assets consist mainly of cash equivalents, including U.S. Treasuries, commercial paper, short-term deposits, money market instruments, and corporate bonds. By strategically allocating these reserves, Tether accumulates interest and investment income, contributing significantly to its revenue.

Additionally, Tether occasionally participates in short-term lending and other financial instrument trades, further diversifying and enhancing its revenue streams. Through token issuance, redemption processes, and transaction fees across various blockchain platforms, Tether generates additional income.

The following is its latest reserve report, clearly showing that over 80% of its reserves consist of cash, cash equivalents, and other short-term deposits, with approximately 80% specifically invested in U.S. Treasuries.

Essentially, Tether’s revenue is heavily dependent on interest rates set by central banks, particularly those of the U.S. Federal Reserve, as the appreciation of most of its reserve assets is directly linked to these rates. Higher interest rates greatly boost Tether’s returns from its reserves, while lower rates significantly reduce its income potential.

Importantly, unlike some other stablecoins, all revenue generated by Tether is retained by the issuer and not distributed to USDT token holders. This contrasts with yield-bearing stablecoins, which distribute returns directly to holders—highlighting a key difference in stablecoin business models.

Historical Revenue Trends

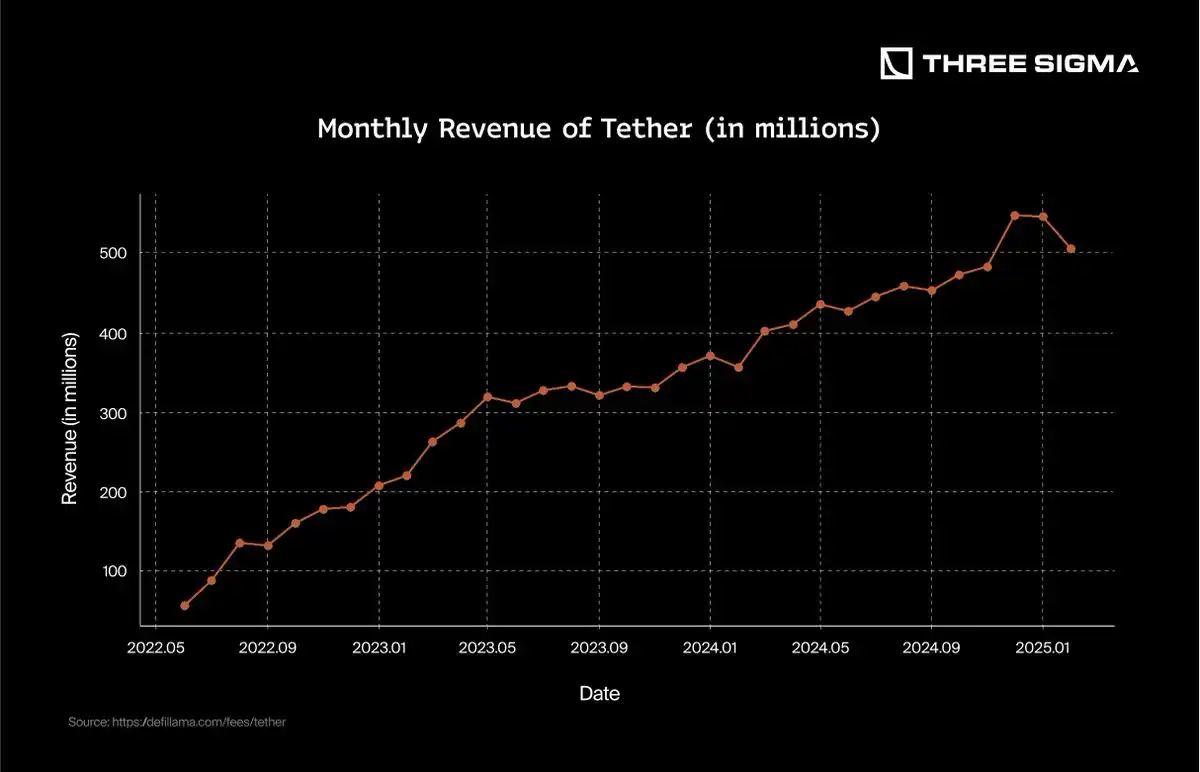

Historically, Tether’s revenue trajectory has been closely tied to global interest rate trends. During the low-interest-rate period from 2019 to early 2022, Tether’s revenue growth was relatively modest, primarily due to its conservative investment strategy yielding limited returns.

However, beginning in mid-2022, as central banks aggressively raised interest rates to combat inflation, Tether’s revenue surged significantly. From June 2022 to early 2025, monthly revenue nearly increased tenfold, highlighting Tether’s revenue model’s extreme sensitivity to macroeconomic changes and monetary policy decisions. This trend demonstrates the effectiveness of Tether’s revenue model in an interest rate hike environment.

That said, revenue is not entirely dependent on interest rates. Even in a declining rate environment, if USDT supply increases significantly, Tether could still achieve revenue growth. Larger supply means more assets under management, which can compensate for lower yields, thereby maintaining or even increasing overall revenue.

USDC

USDC, issued by Circle, is one of the most trusted centralized stablecoins in the market. Renowned for its compliance and transparency, it is widely used in decentralized finance, institutional payments, and cross-chain applications. Its presence across multiple blockchains enhances its composability and ecosystem coverage.

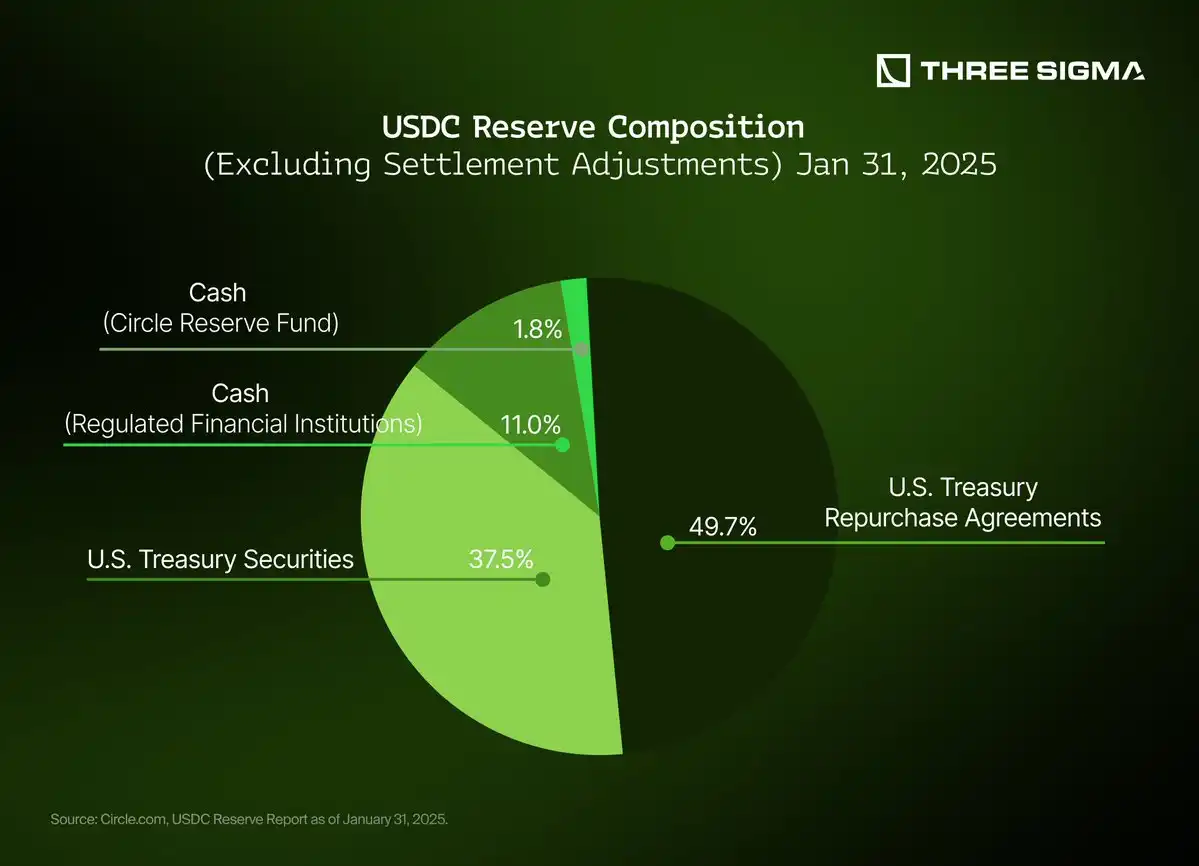

A key feature of USDC is Circle’s strict reserve structure and public disclosures. As of January 31, 2025, the circulating supply exceeded $53.2 billion and was fully backed by $53.28 billion in reserves, independently certified by accounting firms. These reserves are allocated as follows:

Circle Reserve Fund: A government money market fund holding $47.26 billion in U.S. Treasuries and repurchase agreements.

Segregated Bank Accounts: Holding an additional $6.02 billion, stored in regulated financial institutions.

Circle generates revenue by managing these reserve assets, primarily through interest income from U.S. Treasuries and overnight loan arrangements. Although structurally similar to Tether’s model, Circle’s funding structure stands out by granting USDC holders 100% ownership rights to the reserve fund. This not only ensures clearer regulatory separation but may also enable more flexible product integrations in the future.

Unlike decentralized alternatives, USDC does not directly distribute earnings to users. Instead, revenue accrues to the issuer, prioritizing simplicity, compliance, and capital preservation.

Historical Revenue Trends

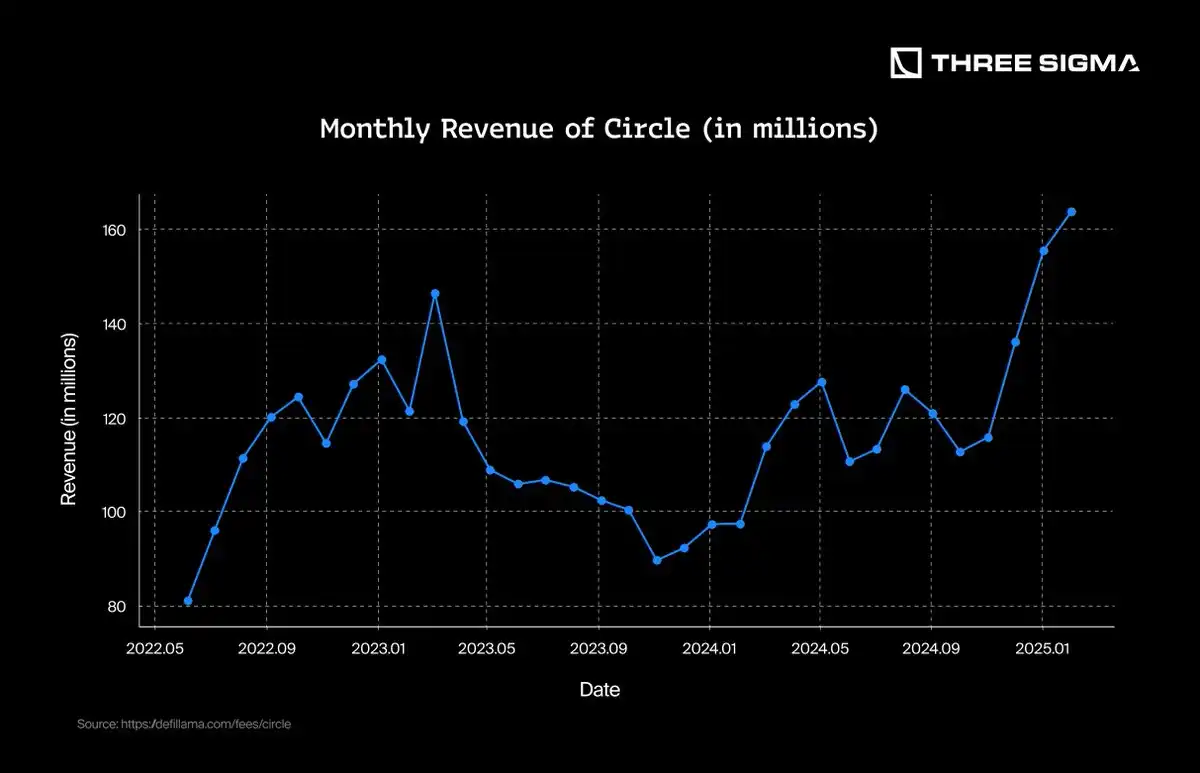

Circle’s revenue trajectory is closely tied to the overall interest rate environment, as its conservative investment strategy focuses primarily on short-term government debt.

In 2022, as the U.S. Federal Reserve raised interest rates, Circle’s revenue grew steadily and peaked at $146.5 million in March 2023. However, later that year, pressure from competing stablecoins, blockchain reliability issues (particularly on Solana), and reputational volatility tied to banking partners led to a gradual decline in revenue. By the end of 2023, monthly revenue had dropped below $90 million.

In 2024, as redemptions decreased, crypto activity rebounded, and high interest rates persisted, Circle’s revenue began to recover, reaching $126 million in August and ending the year on a strong note. In February 2025, Circle achieved its highest single-month revenue record, hitting $163.7 million.

This trend highlights USDC’s resilience and the close relationship between stablecoin revenue models and monetary policy. Circle’s sustained recovery underscores its ability to maintain user trust and leadership in liquidity throughout market cycles.

USDS/DAI (SKY)

USDS is the current evolution of DAI, the first major decentralized stablecoin issued by MakerDAO, designed as an censorship-resistant alternative to traditionally fiat-backed assets. Although both belong to the Maker ecosystem, they differ structurally in collateral models and target use cases.

DAI is an over-collateralized stablecoin, supported by a mix of crypto assets, RWAs, and stablecoins. Users deposit ETH, stETH, or USDC into Maker Vaults to mint DAI, ensuring it remains fully collateralized at all times. This design gives DAI strong risk resistance but limits scalability.

On the other hand, USDS represents MakerDAO’s evolution toward more traditional-finance-compatible stablecoins. Although still over-collateralized, USDS employs a structured reserve approach, including tokenized short-term U.S. Treasuries. This aligns it with institutional demand, positioning it as a competitor to USDT and USDC while preserving MakerDAO’s decentralized governance model.

The transition from DAI to USDS reflects a move toward broader institutional adoption. While DAI initially served as a crypto-native stablecoin primarily backed by decentralized assets, USDS optimizes its collateral structure by incorporating more RWAs, especially U.S. Treasuries.

Moreover, USDS enhances stability through direct convertible mechanisms, making it easier to maintain its peg to the dollar. Unlike DAI’s early reliance on external DeFi incentives, USDS was designed from the outset to provide built-in yield through the DSR, making it more attractive in both DeFi and TradFi environments. This structure aligns with the growing popularity of RWA yield DeFi strategies in 2025.

Transparency is foundational to the Sky ecosystem’s design—it serves not just as a tool to maintain the peg but as a prerequisite for building trust, attracting institutional participation, and responsible capital allocation. In an environment managing tens of billions in assets, users and institutions demand clear visibility into where funds are held, how they are used, and the backing of the system.

Thus, Sky provides a publicly accessible real-time dashboard clearly displaying USDS’s backing, diversification, and yield. Yet, transparency alone cannot stabilize a currency—the peg is maintained through over-collateralization, risk-managed asset allocation, and protocol-level mechanisms.

USDS always maintains more collateral than its supply. As of now, the total collateral base exceeds $10.8 billion, with a supply of approximately $8.3 billion, ensuring sufficient buffer to withstand market volatility or redemptions. Its collateral is distributed across several key sources:

· Stablecoins (54.8%): Primarily supported by the LitePSM module, a pegged stable module enabling 1:1 exchange between DAI and USDC to support USDS’s peg.

· Spark (24.7%): Sky’s lending and liquidity protocol, using high-quality, yield-generating collateral to mint USDS.

· Cash RWA (9.7%): Fully held at BlockTower Andromeda, a strategy investing in short-term U.S. Treasuries, providing low-risk real-world yield.

· Core (9%): Sky’s over-collateralized Vault system, where users mint USDS using ETH and stETH under strict collateral thresholds.

These mechanisms collectively ensure USDS remains stable, over-collateralized, and supported by a range of liquid, yield-generating assets, while transparency allows anyone to verify this at any time.

Historical Revenue Trends

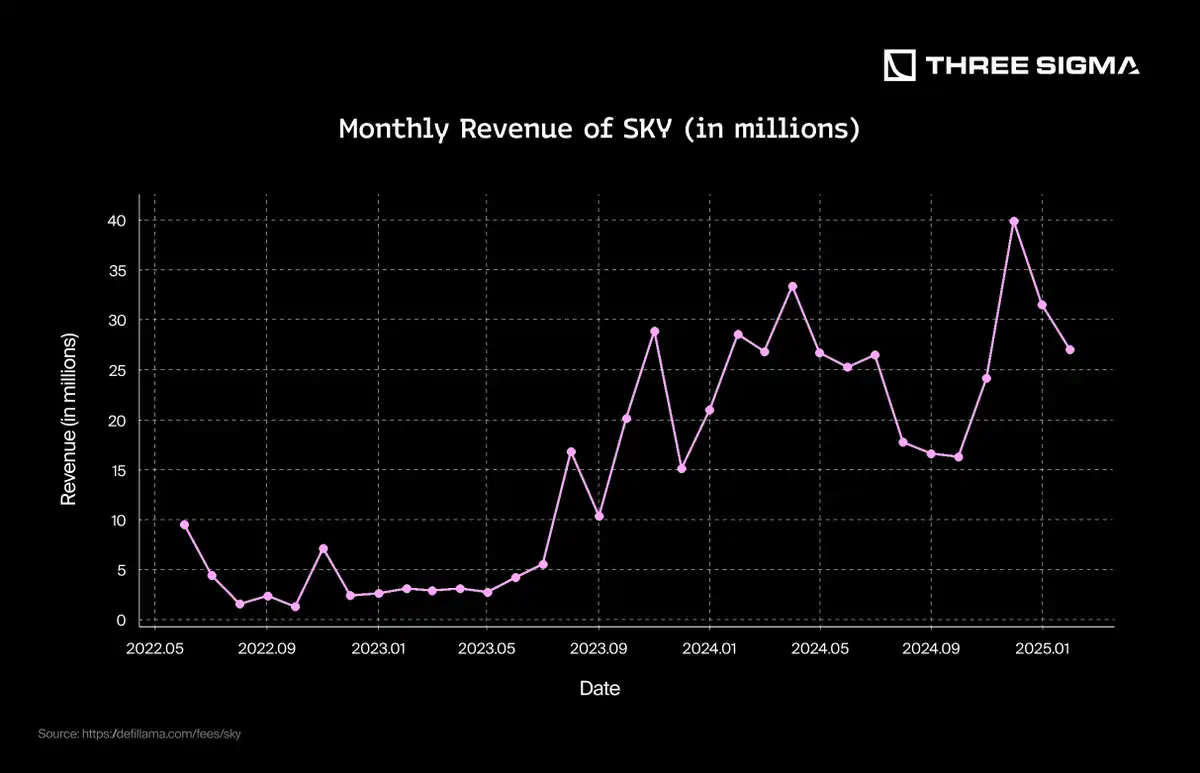

The chart above shows Sky protocol’s cumulative revenue from mid-2022 to early 2025. Although revenue grew steadily in the initial months, it accelerated significantly by late 2023 as DeFi integration expanded, USDS adoption increased, and deeper exposure to real-world assets (like short-term U.S. Treasuries) took hold—coinciding with rising interest rates. By early 2025, cumulative revenue surpassed $500 million, reflecting Sky’s ability to scale sustainably while capturing yield in both crypto-native and institutional strategies.

USDe

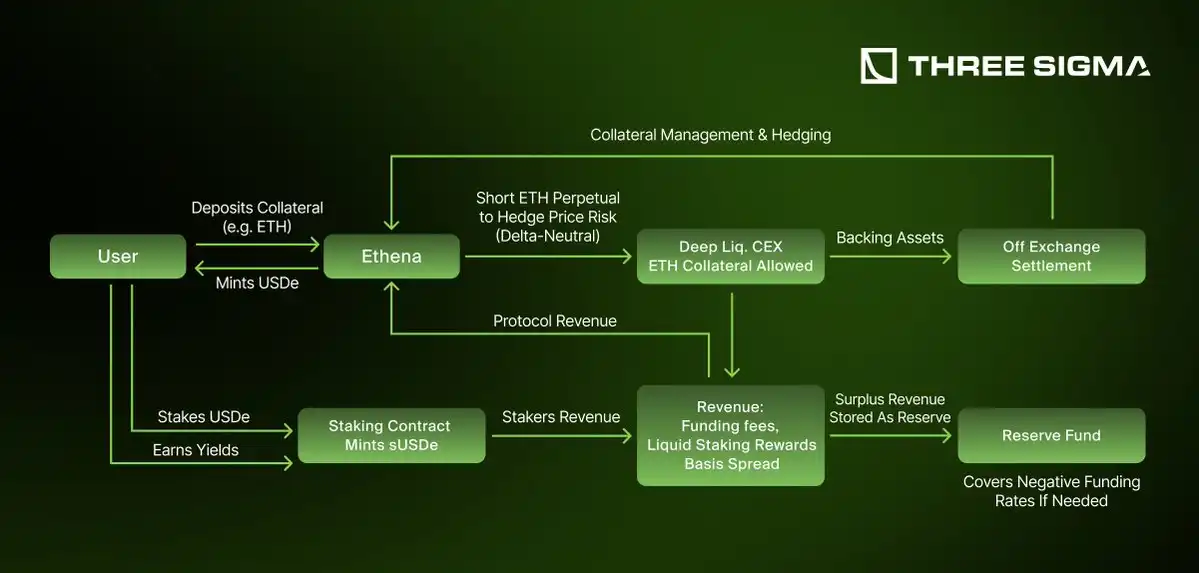

USDe is a delta-neutral synthetic dollar stablecoin built on a perpetual futures-based synthetic dollar structure, developed by Ethena Labs. Unlike traditional stablecoins backed by fiat reserves or over-collateralized crypto assets, USDe maintains its dollar peg through an automated hedging strategy. This grants it full backing, scalability, and censorship resistance. Ethena also offers sUSDe, a yield-bearing version of USDe, capable of earning rewards through liquid staking assets and yield arbitrage in the futures market.

Since its public launch in early 2024, Ethena has scaled rapidly, reaching a supply of $6 billion in just ten months, making USDe the third-largest dollar-denominated asset in the crypto space. It has also become a foundational component of DeFi, integrated into major protocols like Pendle, Morpho, and Aave, driving significant growth. Beyond DeFi, USDe has penetrated CeFi, now integrated as collateral on approximately 60% of centralized exchanges—surpassing USDC balances on Bybit within a month.

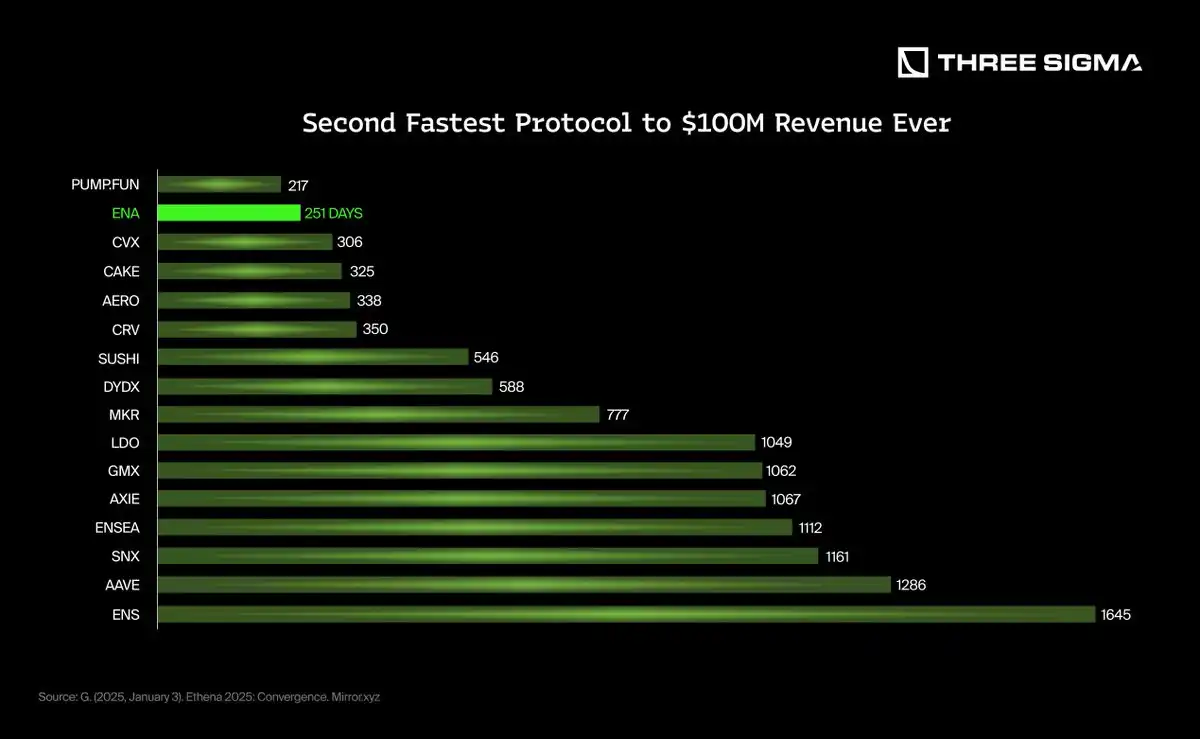

If we dive deeper into revenue, Ethena performs exceptionally well, becoming the second-fastest dApp in history to reach $100 million in revenue (after Pump.fun), achieving this milestone in just 251 days. In 2024, Ethena emerged as a dominant force in DeFi, accounting for over 50% of Pendle’s TVL, around 30% of Morpho’s TVL linked to Ethena, and becoming the fastest-growing new asset on Aave—reaching $1.2 billion in deposits in just three weeks.

Ethena's next phase is defined by Convergence, aiming to unify DeFi, CeFi, and TradFi through USDe. By introducing iUSDe, a wrapped version of sUSDe designed for institutional adoption, Ethena plans to deliver a high-yield, crypto-native dollar product tailored for asset managers, private credit funds, and exchange-traded instruments. By bridging capital flows and interest rate dynamics across financial systems, Ethena positions USDe as the foundational pillar of the evolving digital dollar ecosystem.

How Does USDe Work?

USDe maintains stability through a delta-neutral hedging strategy, ensuring its value remains insulated from market volatility. When users mint USDe, the collateral received by Ethena can include ETH, BTC, LSTs, USDT, USDC, and SOL. To neutralize price risk, Ethena opens a perpetual futures short position for each collateral asset received. For example, if the collateral is ETH, Ethena takes a short position in ETH perpetual futures.

This mechanism ensures that any price fluctuation in the collateral is offset by the corresponding futures position. If the collateral appreciates, the short position incurs losses but is compensated by the appreciation. Conversely, if the collateral depreciates, the short position profits, offsetting the decline. This mechanism ensures USDe remains stable regardless of market fluctuations.

Unlike other synthetic stablecoins, Ethena does not employ additional leverage—only the leverage naturally embedded in derivative exchanges is used to assess collateral. This minimizes liquidation risk and ensures each short position is fully backed 1:1 by assets.

To enhance security, Ethena’s supporting assets remain on-chain and are custodied via over-the-counter settlement systems, reducing counterparty risk. Ethena never fully transfers asset control to derivative platforms but only uses them as margin for its short hedging positions, thereby ensuring decentralized and transparent asset management.

Ethena generates revenue by capturing a portion of the returns produced by its delta-neutral strategy, including:

Funding Rate Arbitrage: Ethena profits when perpetual futures funding rates are positive.

Liquid Staking Rewards: A portion of staking yields from deposited LSTs is retained by Ethena.

Basis Profit: Ethena benefits from inefficiencies between spot and futures markets.

Protocol Fees: A portion of total returns is allocated to reserve funds and protocol treasuries, ensuring long-term sustainability.

Although USDe’s delta-neutral strategy minimizes exposure to price volatility, it remains vulnerable to funding rate fluctuations, market imbalances, and counterparty risk. If funding rates remain negative for extended periods, Ethena’s reserve fund absorbs losses, but prolonged negative rates could strain the system.

Liquidity crises or extreme volatility may temporarily cause USDe to deviate from peg when spot and futures markets diverge. Additionally, reliance on centralized exchanges for hedging introduces counterparty risk, though Ethena mitigates this by keeping assets on-chain and using OTC settlements.

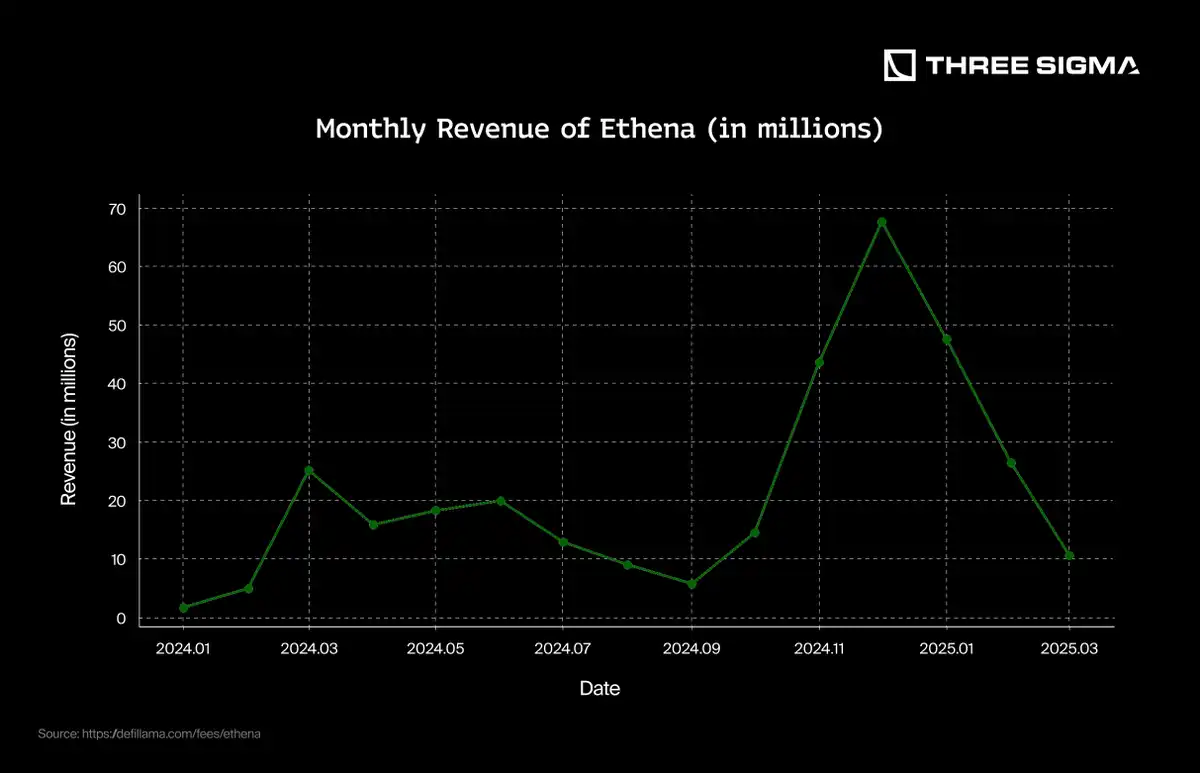

Historical Revenue Trends

Ethena opened to the public on February 19, 2024, enabling users to mint USDe by depositing stablecoins and stake it as sUSDe to earn yield. Within less than a year, the protocol generated cumulative revenue exceeding $320 million, establishing one of the fastest revenue curves in DeFi history.

Steady revenue growth in the first half of 2024 reflected the continuous increase in USDe supply and widespread adoption across DeFi and CeFi platforms. However, revenue acceleration began sharply in October 2024, coinciding with:

Integration of USDe and sUSDe into major lending markets such as Aave and Morpho.

Increased market volatility creating a surge in funding rate arbitrage opportunities.

Launch of new institutional products like iUSDe, extending Ethena’s influence into TradFi.

By Q1 2025, the protocol’s cumulative revenue surpassed $300 million. Despite launching under 15 months prior, Ethena has already emerged among the top revenue-generating projects in the crypto space. This rapid growth signals strong market demand and validates the sustainability of USDe’s delta-neutral model.

However, after peaking at the end of 2024, monthly revenue declined sharply in Q1 2025. This drop correlates with reduced funding rate arbitrage opportunities as perpetual futures funding rates normalized across major exchanges. With lower volatility and a more neutral funding environment, one of Ethena’s primary revenue sources temporarily weakened, highlighting the model’s sensitivity to market conditions.

4. Correlation Between Interest Rates and Revenue

Interest rates are one of the most decisive factors influencing stablecoin revenue performance. As previously discussed, stablecoins generate revenue through various mechanisms—including interest-bearing reserves, market arbitrage, and other yield-generation strategies. Since many stablecoins hold assets sensitive to interest rate changes, their revenue potential is typically influenced by macroeconomic conditions.

To better understand this relationship, we normalize revenue by dividing it by supply. This adjustment enables more accurate comparisons, as an increase in stablecoin supply naturally leads to higher potential revenue generation. By focusing on revenue per unit of supply, we isolate the direct impact of interest rate fluctuations on stablecoin profitability.

USDT

Deep chart analysis vividly illustrates the positive correlation between Tether’s revenue and interest rate volatility. Historical charts comparing Tether’s quarterly revenue with interest rate changes show clear synchronization, highlighting near-instantaneous responsiveness to rate adjustments.

These visualizations effectively emphasize Tether’s sensitivity to interest rate environments, providing predictive insights into future potential scenarios. They underscore the importance of proactive financial and reserve management strategies to mitigate revenue risks associated with interest rate volatility or downturn cycles.

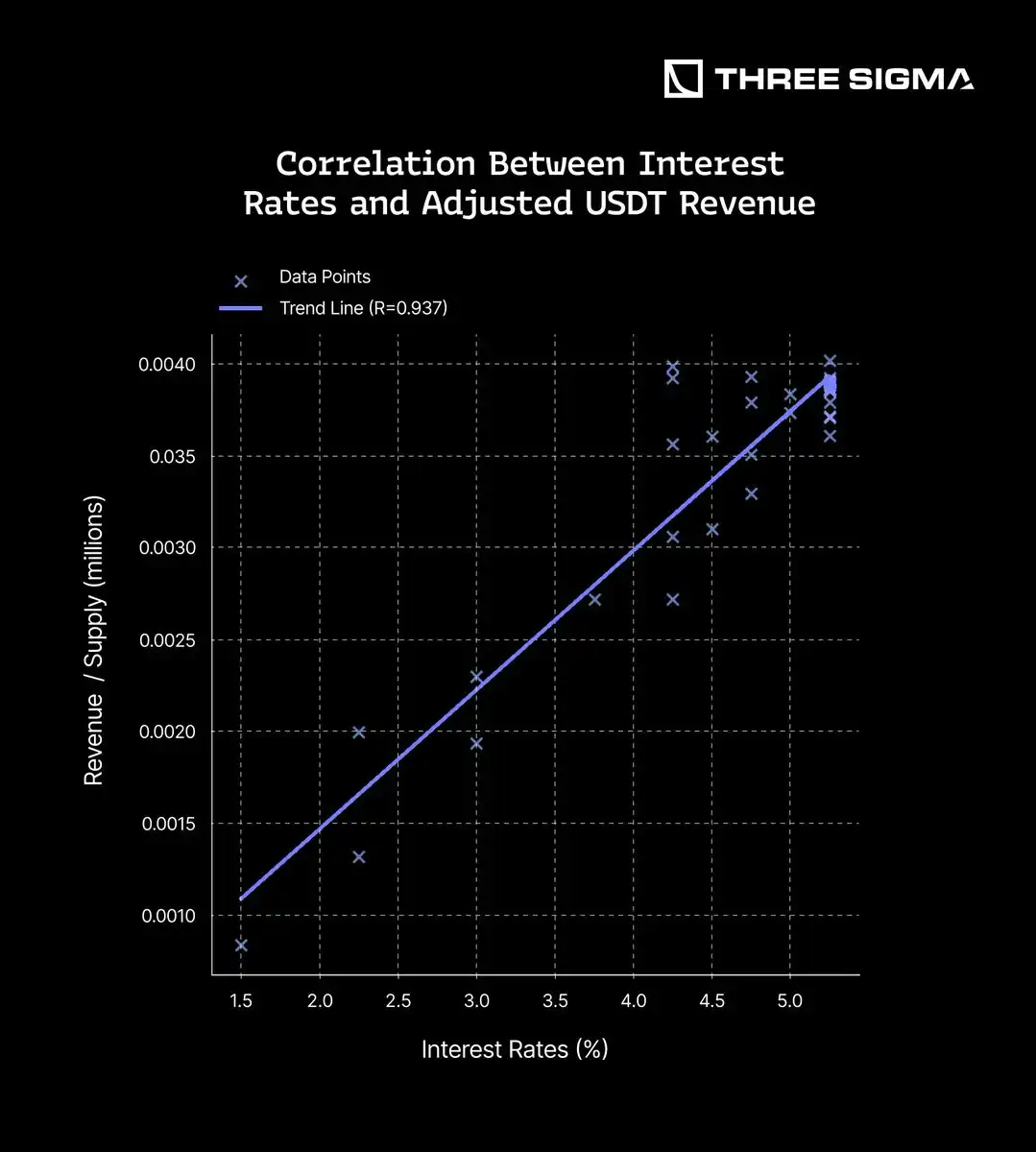

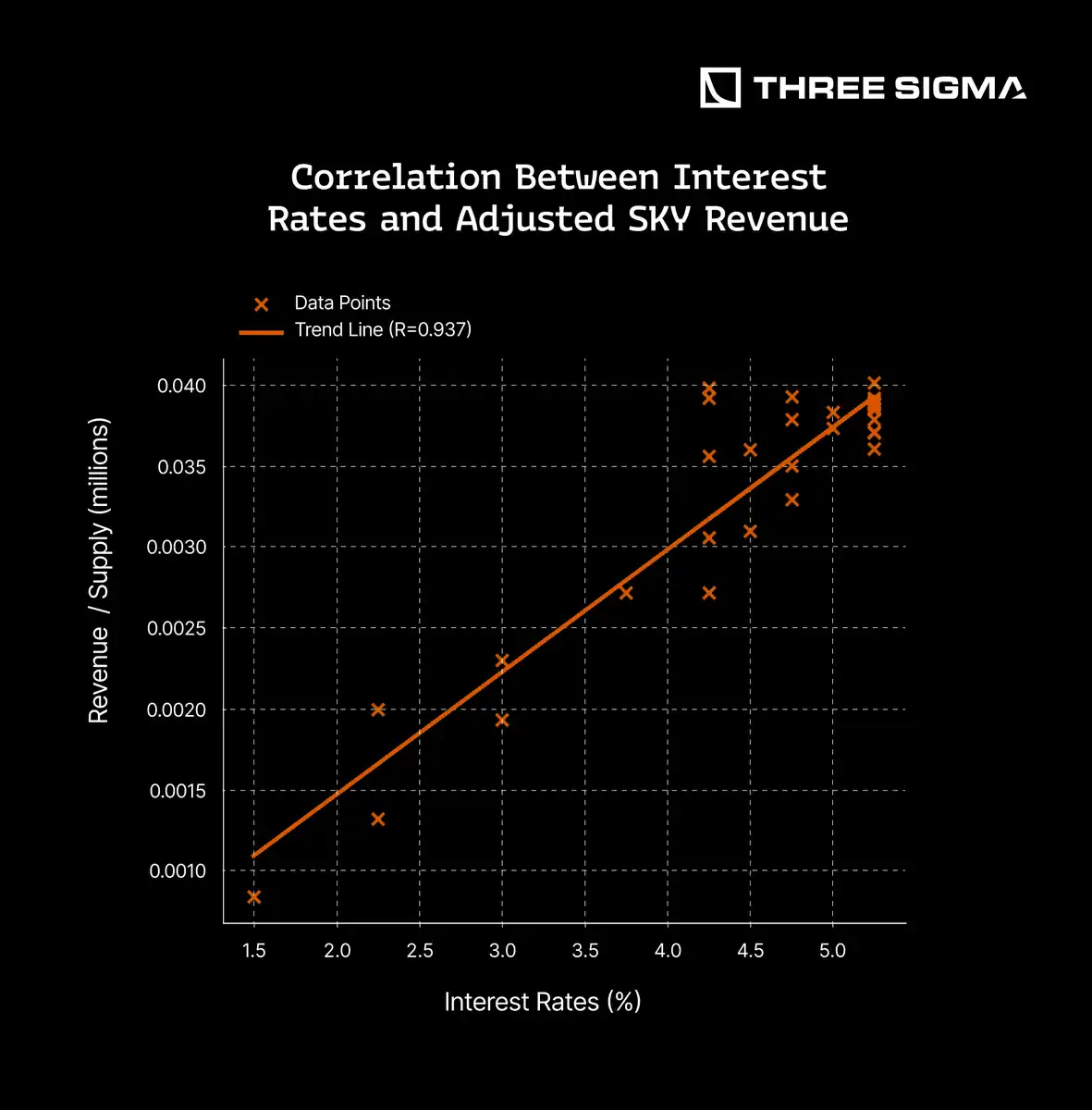

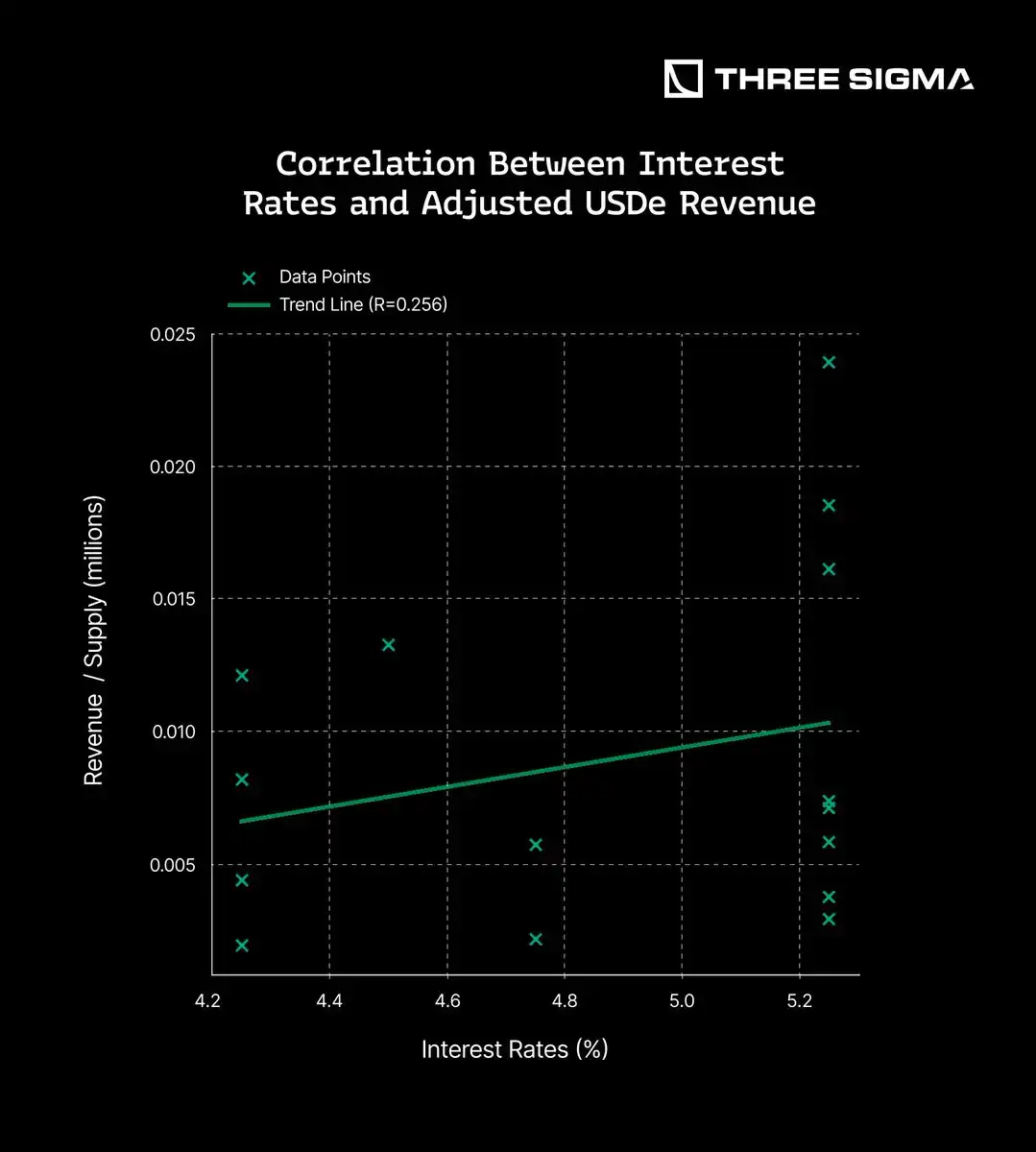

The following chart illustrates the correlation between interest rates and adjusted stablecoin revenue. Each chart shows the evolution of revenue per unit of stablecoin supply (y-axis) against interest rates (x-axis).

The chart further highlights a strong positive correlation (R = 0.937) between interest rates and USDT’s adjusted revenue per unit of supply. This indicates that as interest rates rise, USDT’s revenue per unit increases, reflecting enhanced yields from Tether’s holdings in U.S. Treasuries. As rates increase, Treasury yields rise, directly impacting USDT’s overall revenue.

This correlation underscores how effectively USDT manages its reserve assets to benefit from changing economic conditions, particularly in high-yield environments. It reflects USDT’s flexible financial strategy and its strong positioning during rising interest rate cycles, reinforcing its economic stability and role as a reliable digital asset. As previously noted, perfect 100% correlation is impossible due to the fact that 80% of reserves are held in cash and government bonds, with approximately 80% specifically allocated to Treasury bills.

USDC

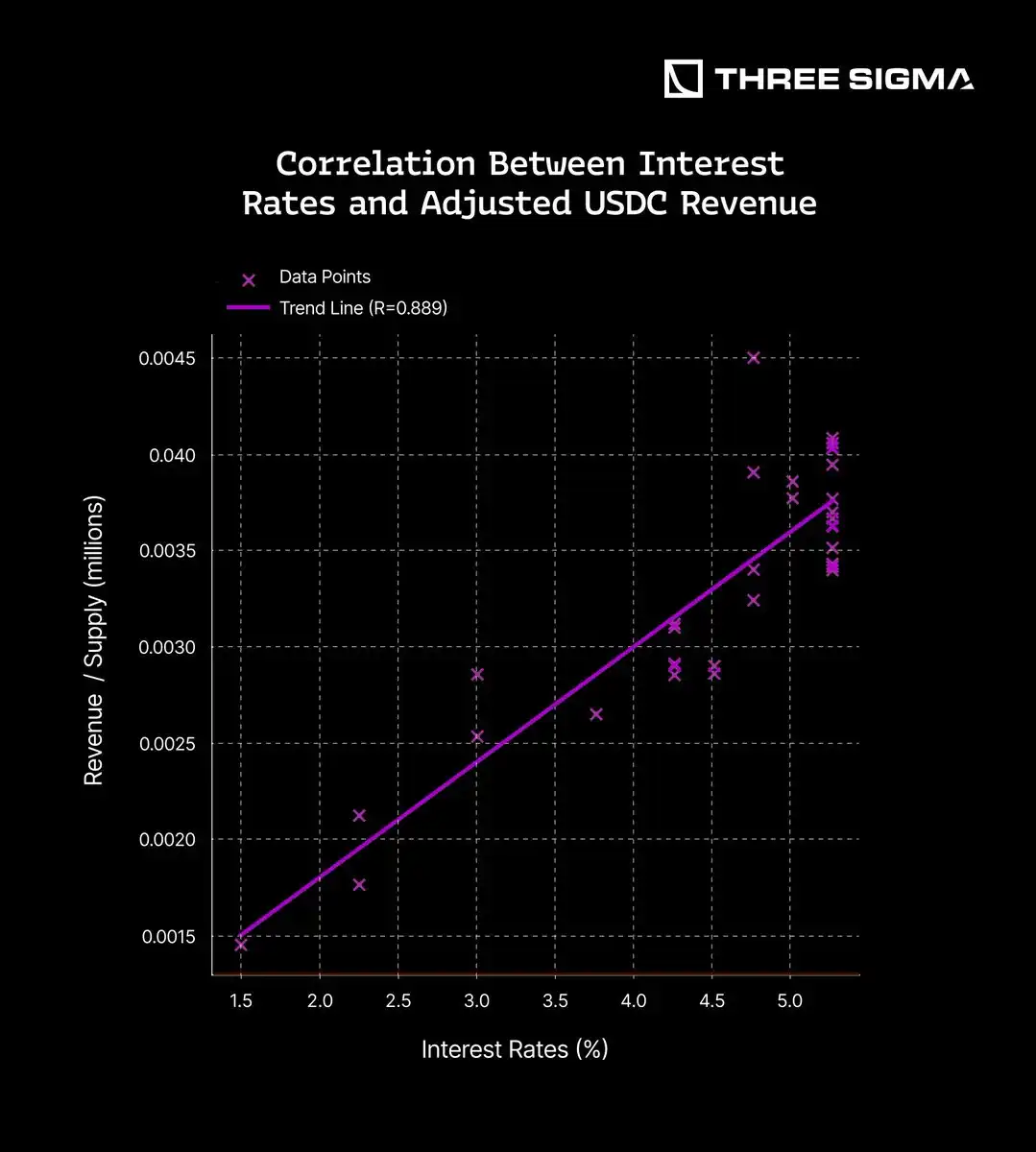

USDC’s economic strength lies in strategic reserve management. As interest rates rise, USDC benefits from its substantial holdings in U.S. Treasuries, which provide higher returns. USDC allocates 75%-80% of its reserves to government bonds, maintaining stability while generating additional income as bond yields increase. The direct link to interest rate fluctuations allows USDC to profit in rising rate environments, further solidifying its status as a yield-optimized stablecoin.

The trend line reveals a strong positive correlation (R = 0.889), indicating that as interest rates rise, USDC’s revenue per unit of supply increases accordingly. This aligns with expectations, as USDC, like other reserve-backed stablecoins, derives returns from high-yielding assets such as U.S. Treasuries.

This correlation highlights USDC’s ability to optimize reserves and adapt to economic shifts. It also emphasizes how reserve-backed stablecoins leverage rising interest rates to enhance yield generation, further cementing their role within the digital asset ecosystem.

Although this correlation is strong (R = 0.889), it is weaker than USDT’s due to differences in reserve composition. USDT maintains a larger portion of its reserves (~80%) in short-term U.S. Treasury bills, which are highly sensitive to rate changes. In contrast, USDC’s reserves are more diversified—only 37.5% in government bonds, nearly 50% in repurchase agreements (repos), which respond more indirectly to rate fluctuations. This diversification enhances liquidity and stability but slightly weakens the direct impact of rate hikes on revenue, resulting in a lower correlation. In summary, the comparison between USDT and USDC revenues underscores the impact of reserve composition and yield strategy.

SKY (DAI/USDs)

SKY’s economic strength lies in strategic reserve management. As interest rates rise, SKY stablecoins (USDS and DAI) benefit from their exposure to yield-generating assets.

Unlike USDC and USDT, traditionally backed by institutional reserves, DAI has historically relied on crypto-collateralized assets such as ETH. However, in October 2022, MakerDAO began allocating a significant portion of DAI’s reserves into U.S. Treasuries and other real-world assets (RWAs) to capture higher yields. As of July 2023, over 65% of DAI’s reserves were linked to RWAs, making its revenue more sensitive to interest rate fluctuations. This shift brought DAI’s behavior closer to that of institutional stablecoins, allowing it to directly benefit from rising interest rates.

As expected, the change in DAI’s reserve composition led to a strong positive correlation (R = 0.937) between interest rates and SKY stablecoin revenue per unit of supply. Data confirms that higher interest rates contribute to increased revenue generation, further validating SKY stablecoins’ current performance as akin to yield-optimized institutional stablecoins.

USDe

USDe’s revenue model is primarily driven by funding rate arbitrage in perpetual futures markets, rather than traditional interest-bearing assets like U.S. Treasuries. As seen, its hedging strategy involves holding short positions in perpetual futures, profiting from fees paid by long-position traders when open interest imbalances occur.

When demand for long positions increases, funding rates rise, making long positions more expensive while creating profit opportunities for short traders—including USDe. However, this revenue model is less directly affected by traditional interest rate changes and instead depends more on market volatility, trader positioning, and the overall leveraged demand in the crypto market.

The trend line shows a weak positive correlation (R = 0.256), indicating that although higher interest rates may have some impact on USDe’s revenue, the relationship is not particularly strong.

This aligns with expectations, as USDe’s revenue model is primarily driven by the state of perpetual futures markets, not interest rate movements. Funding rates and leveraged demand play a far greater role in revenue generation than conventional interest rate hikes.

This correlation highlights USDe’s revenue dependence on trader behavior, not direct exposure to real-world interest rate changes. While lower interest rates may encourage greater risk-taking and leverage use in the crypto market, USDe’s profitability remains closely tied to funding rate imbalances in perpetual futures trading.

5. Impact of Interest Rates Falling to 0%

Interest Rates

Interest rates represent the cost of borrowing, or conversely, the return earned from lending or depositing funds. Central banks, such as the U.S. Federal Reserve, set benchmark rates (e.g., the federal funds rate) to manage economic growth, control inflation, and stabilize financial systems. Lower rates typically encourage borrowing, stimulating economic activity, but may fuel inflation.

Conversely, higher interest rates discourage borrowing, slow economic expansion, but help curb inflationary pressures. Historically, interest rates have fluctuated dramatically across economic cycles and crises, often approaching zero during recessions (e.g., the 2008 financial crisis, the COVID-19 pandemic) and surging during inflationary periods (e.g., post-pandemic 2022–2024). These fluctuations directly affect Treasury bill (T-Bill) and bond yields, which are crucial for stablecoin issuers relying on such investment returns.

Historical Interest Rates

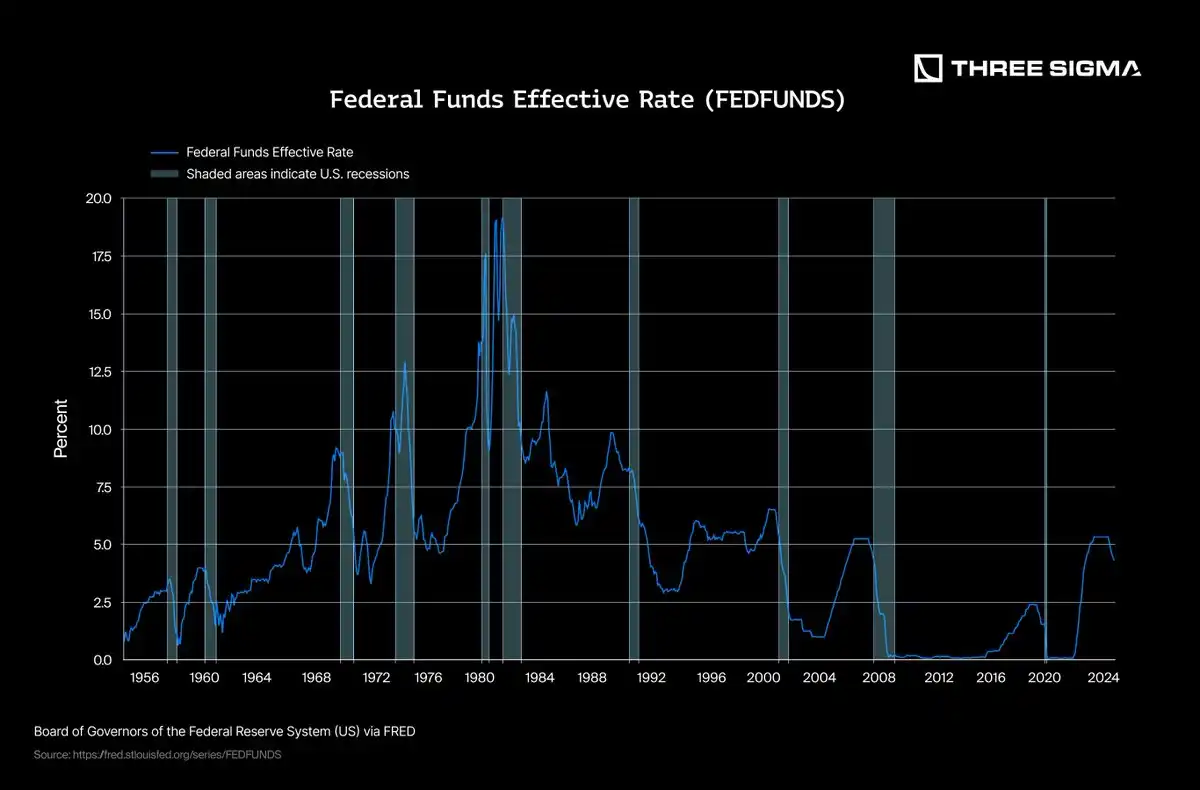

The most critical interest rate is the one set by the U.S. Federal Reserve System, especially the federal funds rate, due to the global dominance of the U.S. dollar as a reserve currency and its wide-ranging impact on international financial markets. Changes in U.S. interest rates significantly affect global economic activity, currency valuations, investment flows, and borrowing costs, making them a key benchmark for global financial stability.

Historical charts clearly illustrate several major interest rate cycles, including the record-high rates of the early 1980s aimed at combating inflation, followed by a steady decline into the low-rate environment of the past two decades. The 2008 financial crisis particularly forced rates close to zero to stimulate economic recovery.

Specifically, during the previous interest rate cycle (2010–2020), the Fed maintained rates at historically low levels (near 0%) for an extended period until gradual increases began around 2015–2018 as the economy recovered. However, the outbreak of the COVID-19 pandemic in early 2020 again prompted a sharp reduction in rates to near-zero levels, aimed at countering economic slowdown, ensuring liquidity, and stabilizing financial markets.

Correlation Between Interest Rates and Revenue: A Comparison

As previously discussed, certain stablecoins’ revenue models are highly dependent on interest rates, while others are structurally insulated from such fluctuations.

The provided data clearly demonstrates this distinction. USDT, USDC, and SKY exhibit high correlations (R ~0.89–0.94), highlighting their significant dependence on prevailing interest rates. Their revenue primarily stems from traditional investments such as government bonds, making them particularly vulnerable in a zero-interest-rate environment, which could severely impact their profitability.

In stark contrast, USDe exhibits a markedly weaker correlation (R = 0.256), reflecting its fundamentally different revenue generation mechanism. USDe’s revenue primarily originates from crypto-market dynamics—such as perpetual futures funding rate arbitrage and staking rewards—not from traditional, interest-sensitive assets.

In conclusion, these data strongly suggest that fiat- and treasury-backed stablecoins (like USDT, USDC, and SKY) face considerable risks in low-interest-rate environments. Conversely, algorithmic stablecoins like USDe, with alternative revenue strategies, demonstrate greater resilience and may serve as strategic diversification tools within investment portfolios, offering relative stability during interest rate declines.

Scenario of Interest Rates Falling to 0%

The impact on stablecoins varies significantly depending on their revenue model and asset allocation when interest rates return to 0%:

Tether

Since USDT primarily generates revenue through traditional financial assets (e.g., Treasury bills), a fall in interest rates to 0% would drastically reduce its revenue sources, severely impacting profitability. However, Tether’s strategic diversification into alternative investments—including Bitcoin (BTC), Ethereum (ETH), and precious metals—may partially offset this impact. Nonetheless, these alternative assets bring higher volatility and risk, potentially failing to fully compensate for lost interest income, possibly weakening its overall market position.

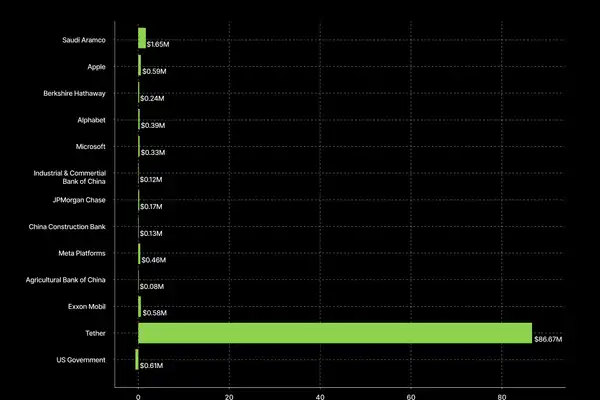

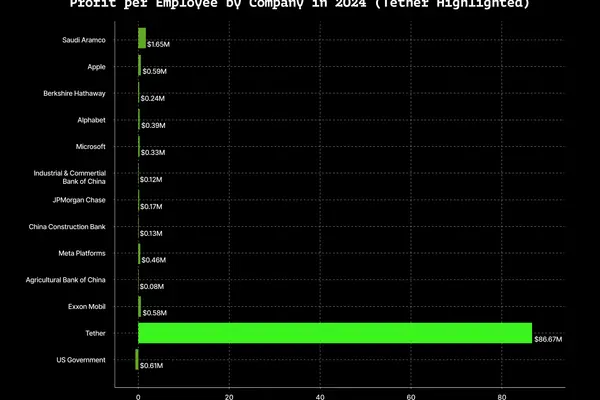

In 2024, Tether maintained very low operating expenses, thanks to a lean team of fewer than 50 employees, minimal administrative overhead, and transaction fees from the USDT token broadly covering operational costs. Legal and regulatory expenses were also relatively low, with no major fines this year—unlike the $18.5 million penalty paid to New York’s Attorney General in 2021.

Financially, Tether ended 2024 with strong reserves, exceeding its USDT holder obligations by approximately $7.1 billion, with total equity around $20 billion. Given its conservative annual operating expenses (likely below $100 million), even if future revenue were to drop to zero, Tether could sustain operations for over 70 years, demonstrating exceptional financial stability and virtually infinite operational runway.

Circle

Circle recently filed an S-1 registration statement with the U.S. Securities and Exchange Commission, indicating plans to list on the New York Stock Exchange under the ticker symbol "CRCL".

In 2024, Circle reported total revenue of approximately $1.68 billion, a 16% increase from $1.45 billion in 2023. Notably, over 99% of this revenue came from reserve income, primarily interest earned on assets backing USDC. Net income for 2024 was approximately $156 million, a significant decrease from $268 million in the prior year, mainly due to increased operating and distribution expenses.

Total operating expenses for 2024 amounted to about $492 million, with the majority going toward employee compensation ($263 million), general and administrative costs ($137 million), IT infrastructure ($27 million), depreciation and amortization (~$51 million), marketing expenses ($17 million), and digital asset losses ($4 million). Additionally, Circle incurred approximately $1.01 billion in distribution and transaction costs, with about $908 million paid to major distribution partners like Coinbase.

As of December 31, 2024, Circle held $751 million in cash and cash equivalents, plus $294 million in other liquid investments, totaling approximately $1.045 billion in available liquidity. When estimating financial sustainability under zero-revenue scenarios, it is crucial to distinguish between these two asset categories:

The $751 million in cash and cash equivalents represents highly liquid, immediately usable funds—ideal for conservative financial sustainability estimates. Based solely on this, assuming current annual operating expenses of $492 million, Circle’s financial sustainability period is approximately 18 months.

If the full $1.045 billion in liquidity (cash and other liquid assets) is included, and assuming these additional assets can be used without restrictions, the financial sustainability period extends to about 25 months.

A more conservative approach focuses only on cash equivalents to avoid relying on potentially illiquid or restricted assets. However, if Circle can seamlessly utilize its broader liquidity pool, it gains greater flexibility.

In a prolonged zero-interest-rate environment, Circle’s heavy reliance on interest income from reserves could significantly impact its revenue stream. If it fails to effectively diversify its income sources, the company’s profitability could suffer, potentially requiring strategic adjustments such as restructuring fees or exploring new investment avenues.

Under 0% interest rates, Sky Protocol (formerly MakerDAO) indeed faces significant challenges, particularly regarding revenue sources and financial sustainability. The protocol relies on U.S. Treasuries, ETH staking rewards, and DeFi income, meaning the absence of interest could greatly affect its revenue.

Revenue sources face pressure:

Stability fees and lending demand: Decreased lending demand may lead to lower stability fees on DAI loans. This decline, combined with reduced yields from U.S. Treasuries and other bonds, could exacerbate the protocol’s financial strain.

DeFi funding fees: In a low-interest-rate environment, traders may be less inclined to engage in leveraged activities, leading to reduced funding fees in DeFi ecosystems.

Historically, Sky Protocol has demonstrated adaptability to low-interest-rate environments by adjusting parameters such as Sky Savings Rate (SSR). For example, SSR was recently lowered to 4.5%, effective March 24, 2025, to align with current market conditions.

Sky Protocol’s total asset value is approximately $220 million, comprising:

$101 million in DAI – stable

$82.2 million in SKY tokens – volatile

$36.4 million in MKR tokens – volatile

$243,000 in stkAAVE – volatile

$470,000 in ENS – volatile

This $220 million total value combines liquid assets like DAI with volatile tokens such as SKY and MKR, whose values may fluctuate based on market conditions. Liquid assets are the most accessible funds for protocol operations, while volatile tokens represent a more strategic asset class subject to market swings.

The operational runway is the duration Sky Protocol can sustain itself without generating new revenue, based on current assets and annual operating expenses. The protocol’s estimated annual operating expenses are $35 million. The calculation is as follows:

If only liquid assets (DAI) are considered: operational runway = $101 million ÷ $35 million = 2.89 years

If the total asset value (liquid + volatile assets) at current prices is considered: operational runway = $220 million ÷ $35 million = 6.29 years

In a 0% interest rate scenario, Sky Protocol’s financial sustainability largely depends on the value of volatile assets like SKY and MKR, which may fluctuate and affect the overall operational runway. However, based solely on DAI surplus, Sky Protocol can sustain operations for approximately 2.89 years without generating additional revenue. If the entire asset pool (including both liquid and volatile assets) is considered, Sky can maintain operations for roughly 6.29 years, assuming no other major market changes.

As a protocol historically demonstrating adaptability, Sky Protocol can adjust fee structures and make strategic asset allocation decisions to navigate prolonged low-interest-rate environments.

If the Federal Reserve lowers interest rates to 0%, several factors could affect USDe’s ability to maintain or grow its revenue. Lower interest rates reduce borrowing costs, making leveraged positions more attractive for traders and investors. In traditional markets, this typically drives capital into higher-risk assets as fixed-income returns decline, prompting investors to seek higher yields elsewhere. This dynamic applies equally to the crypto market—lower interest rate environments usually lead to capital inflows into cryptocurrencies like Bitcoin and Ethereum.

As more liquidity enters the market, traders become more inclined to take leveraged long positions in crypto assets, anticipating continued price appreciation. This creates imbalance in perpetual contracts markets, with long demand exceeding short supply. Consequently, funding rates rise, increasing the cost of holding long positions while benefiting short traders—such as the USDe strategy.

However, this benefit comes with potential risks. If interest rates remain low for an extended period, USDe’s revenue may eventually stabilize or even decline, as market participants adjust their strategies to the new normal. Such adjustments could involve reducing leverage or altering trading strategies. Moreover, while a low-interest-rate environment initially supports USDe’s revenue generation through perpetual contract funding rates, the long-term stability of these conditions might incentivize shifts in investor behavior toward assets beyond those currently yielding the highest returns.

From a protocol perspective, Ethena is in a favorable financial position. The project has raised over $120 million through venture capital and token sales and maintains a reserve fund of approximately $61 million, verifiable via the on-chain wallet 0x2b5ab59163a6e93b4486f6055d33ca4a115dd4d5. This reserve fund acts as a buffer during negative-return environments, supporting USDe’s stability. Ethena also operates with a lean team, with estimated annual operating expenses ranging from $2 million to $5 million, allowing the project to sustain operations for years even if protocol revenue significantly declines.

In conclusion, while a low-interest-rate environment provides USDe with a unique opportunity to remain attractive in the short term, its long-term sustainability depends on sustained market activity and volatility. Nevertheless, Ethena’s strong reserve position and low burn rate provide a solid financial buffer, ensuring the protocol can operate stably during prolonged low-yield periods without compromising its core stability.

6. Conclusion

The stablecoin ecosystem is deeply intertwined with macroeconomic dynamics, particularly interest rates. As this analysis demonstrates, under the scenario of interest rates falling to 0%, the performance and sustainability of various stablecoin models vary significantly.

Most Affected:

USDC is almost entirely reliant on yields from U.S. Treasuries, making its business model structurally fragile in a prolonged low-interest-rate environment without effective diversification. High operating costs and relatively limited treasury reserves further constrain Circle’s long-term operational capacity.

Significantly Impacted but More Resilient:

USDT and SKY will also face substantial revenue compression due to their dependence on interest-bearing assets. However, both possess certain buffers. Tether (USDT) holds large treasury surpluses, extremely low operating costs, and partial investments in diversified assets (e.g., Bitcoin, gold), granting it a longer financial runway under zero-interest conditions.

SKY (USDS/DAI) similarly faces revenue decline risks. However, it maintains diversified revenue streams through DeFi-native mechanisms (e.g., protocol fees, crypto-collateral liquidations, smart contract lending), offering greater operational flexibility. Additionally, the protocol can rely on governance token sales to cover expenses, as demonstrated in past cycles.

Least Affected / Most Adaptive:

Ethena (USDe) stands out with its market-driven, crypto-native revenue model, independent of interest-bearing instruments. Instead, Ethena captures value through perpetual futures funding rates, staking rewards, and market inefficiencies. In a 0% interest-rate world, USDe may even benefit from increased leverage and speculation, making it one of the few projects poised to thrive when other stablecoins contract.

However, in the long run, sustained low interest rates could lead to a neutral or bearish market environment, potentially reducing Ethena’s profitability. Indeed, when funding rates turn strongly negative for short positions, the protocol may even face short-term losses.

This comparative analysis highlights a key insight: revenue diversification is no longer optional—it is essential. In a world where interest rates may revert to historical lows, stablecoin issuers overly reliant on traditional financial instruments face significant profit erosion risks. Protocols with flexible, crypto-native revenue engines—especially those like USDe—are likely not only to survive but emerge stronger.

Ultimately, the sustainability of the stablecoin market will depend not just on peg stability or market acceptance, but on resilience across economic regimes. Protocols that adapt through product innovation, diversified collateral, or yield mechanisms will define the next generation of digital dollars.

Finally, it is worth noting that Circle and Tether may already be preparing for a low-interest-rate revenue world. Each is actively building or participating in its own blockchain infrastructure: Circle is developing Cortex, and Tether has Plasma. These efforts appear aimed at diversifying service offerings and potentially unlocking new revenue streams beyond treasury yields.

Additionally, Circle’s IPO announcement coincided precisely with the conclusion of our research. Public disclosures align closely with identified vulnerabilities and strategic directions, particularly the need for diversification and expansion through new ventures. The IPO may signify both a liquidity event and a strategic pivot toward a service- and infrastructure-focused business model.

Finally, one cannot help but wonder: does Circle have a hidden ace up its sleeve? Is it quietly preparing to become the official issuer of the digital dollar? While no formal announcement confirms this, such a move would certainly align with its regulatory-first strategy and partnership with the U.S. government. Who knows.

The secret to Web3’s success is just one step away—don’t let someone else get ahead while you’re still hesitating.

Disclaimer: Contains third-party opinions, does not constitute financial advice

AI Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

Popular Airdrop Tutorial

Selected potential airdrop opportunities to gain big with small investments

FusnChain

FusnChain