ChainThink

Stay ahead, master crypto insights

Beosin Releases "2025 Stablecoin Anti-Money Laundering Research Report"

Beosin Releases "2025 Stablecoin Anti-Money Laundering Research Report"

2025-09-10 12:31

*For the complete PDF version of this report, please contact service@beosin.com

A B S T R A C T

This report, supported by the Digital Asset Anti-Money Laundering Committee (DAAMC) under the Hong Kong Virtual Assets Industry Association (HKVAIA) and led by Beosin in research and writing, focuses on core AML issues surrounding stablecoins. It systematically reviews foundational concepts of stablecoins, global regulatory disparities, financial security risks, and constructs a comprehensive technical solution and ecosystem governance framework for Hong Kong, providing professional reference for compliant development of stablecoins.

The report clearly defines stablecoins as digital assets pegged to real-world assets such as fiat currencies, with fiat-collateralized types (e.g., USDT, USDC) dominating the market. Their applications span cross-border remittances, daily consumption, and value storage. The regulatory policy section highlights key differences between Hong Kong’s Stablecoin Ordinance and the U.S. GENIUS Act, while also analyzing policies from Singapore, Japan, South Korea, and the UAE.

Regarding financial security risks associated with stablecoins, their anonymity and cross-border convenience make them susceptible to illicit activities such as terrorist financing, ransomware attacks, and darknet transactions, necessitating vigilance against these risks that could undermine stablecoin development. In response, Beosin proposes a full-lifecycle “source prevention – dynamic monitoring – precise governance” solution tailored for Hong Kong, incorporating technologies like smart contract security auditing, on-chain monitoring of stablecoins, and KYT/KYA risk assessment to enable effective AML surveillance and intelligent criminal analysis.

The report concludes with recommendations from three dimensions—industry self-regulation, interdepartmental coordination, and user education—to assist DAAMC in advancing Hong Kong’s compliant stablecoin ecosystem.

Chapter 1: Definition and Development Trends of Stablecoins

1.1 Definition and Classification of Stablecoins

A stablecoin is a digital asset designed to maintain a relatively stable value by being pegged to a real-world asset such as fiat currency, gold, commodities, or real estate. Within the digital asset ecosystem, stablecoins have been widely adopted for trading, payments, and value storage, serving as a bridge between traditional finance and digital finance.

Currently, multiple countries and regions are either already legislating or preparing legislation regarding stablecoins, aiming to clarify definitions and establish issuer licensing frameworks to provide legal certainty for market participants.

Hong Kong’s regulatory framework provides a clear definition of "fiat-referenced stablecoins (FRS)," which are stablecoins whose value is fully backed by one or more official currencies, HKMA-designated bookkeeping units, or economic store-of-value forms—or combinations thereof—to maintain stability. In contrast, the U.S. GENIUS Act defines a stablecoin as a digital asset used as a means of payment or settlement tool, requiring issuers to maintain a stable value relative to a fixed currency.

The mechanism behind a stablecoin determines its operational model within the financial system, regulatory difficulty, and risk level. Beyond fiat-collateralized stablecoins, other types exist in blockchain ecosystems designed to peg to the U.S. dollar.

Table 1-1: Classification of Stablecoins

| Type | Examples | Characteristics |

| Fiat-Collateralized | USDT, USDC | Backed by real assets (bank custody) held by centralized entities; on-chain representation is merely a tokenized form of real-world assets |

| Token-Collateralized | DAI, RAI | Collateralized by digital assets like ETH, with minting and liquidation governed by smart contracts |

| Algorithmic Stablecoins | UST, AMPL | Stabilized through algorithmic supply-demand adjustments — high-risk models |

| Partially Collateralized + Algorithmic | FRAX | Combines partial collateral with algorithmic demand management |

1.2 Overview of the Top 10 Global Stablecoins by Market Capitalization

Stablecoins have been evolving for over a decade. Since the launch of USDT in 2014, the market has grown rapidly, with fiat-pegged stablecoins leading the sector. As of August 20, 2025, according to DefiLlama data, the total circulating market capitalization of global stablecoins reached $277.5 billion. The top ten stablecoins by market cap are:

Table 1-2: Top 10 Stablecoin Overview

| Token Name | Market Cap | Number of Holding Addresses | Issuer | Freeze Function Supported? |

| USDT | $166.987 billion | 112 million | Tether | Yes |

| USDC | $66.663 billion | 30.5 million | Circle | Yes |

| USDe | $11.852 billion | 773,000 | Ethena Labs | No |

| DAI | $4.786 billion | 1.819 million | Sky | No |

| USDS | $4.503 billion | 45,000 | Sky | Yes |

| USD1 | $2.208 billion | 349,000 | BitGo | Yes |

| FDUSD | $1.448 billion | 62,000 | First Digital Labs | Yes |

| PYUSD | $1.193 billion | 91,000 | PayPal | Yes |

| RLUSD | $666 million | 35,000 | Standard Custody & Trust Company | Yes |

| TUSD | $493 million | 368,000 | TrueUSD | Yes |

Data Source: https://defillama.com/stablecoins

From a market share perspective, fiat-referenced stablecoins account for over 83.46% of the market, including USDT, USDC, USD1, FDUSD, PYUSD, RLUSD, and TUSD, which dominate the landscape. USDe, as a synthetic dollar stablecoin, gains traction through yield generation via arbitrage between spot and futures markets on centralized exchanges, earning recognition in the crypto space and becoming the third-largest stablecoin.

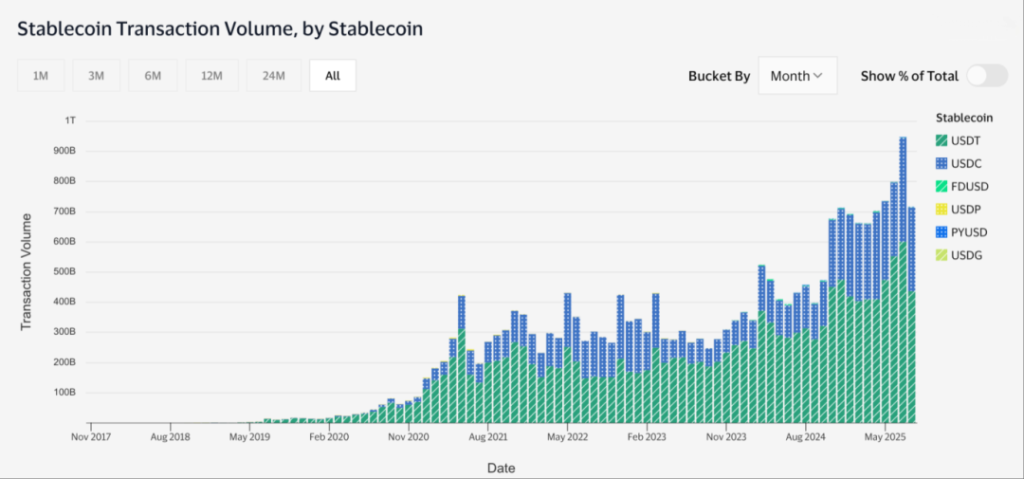

In terms of on-chain transaction data, transaction frequency for stablecoins is rising. According to Visa, the total transaction volume of stablecoins exceeded $27.6 trillion in 2024, with adjusted transaction volume reaching $5 trillion. USDT consistently leads in transaction volume, followed by USDC, together accounting for over 90% of all stablecoin transaction data.

Figure 1-1: Monthly Stablecoin Transaction Volume

Data Source: Transactions | Visa Onchain Analytics Dashboard

Note: Adjusted Transaction Volume excludes robot activity, internal smart contract transactions, exchange-to-exchange transfers, and high-frequency trader transactions.

Over the past year, USDT on the TRON network has seen significant growth, with circulating USDT surpassing $82.6 billion, overtaking Ethereum as the blockchain network with the largest USDT circulation. BSC (also known as BNB Chain) has experienced explosive transaction volume due to Binance’s support for free withdrawals of stablecoins to the BSC network, making it the most active blockchain for stablecoin transactions over the past year.

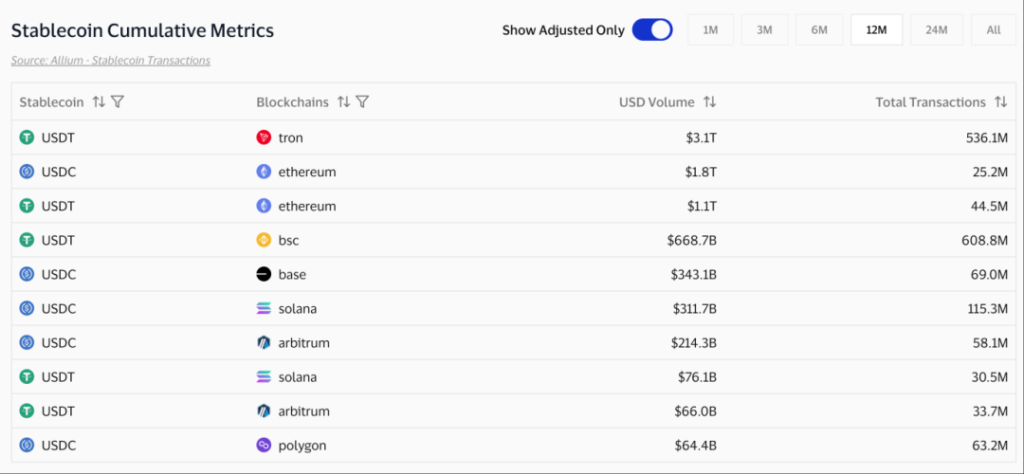

Figure 1-2: Annual Transaction Volume and Count for USDT and USDC on Major Blockchain Platforms

Data Source: Transactions | Visa Onchain Analytics Dashboard

Stablecoin transaction volume and count on networks such as Base, Solana, Arbitrum, and Polygon are also significant. As shown in the chart, although Ethereum remains the primary blockchain for stablecoin circulation and trading, low-cost and high-speed blockchains are emerging as preferred choices for enterprises and general users.

1.3 Key Application Scenarios of Stablecoins

In July 2025, the International Monetary Fund analyzed approximately $2 trillion in adjusted transaction volume across six major chains—Ethereum, Binance Smart Chain, Optimism, Arbitrum, Base, and Linea—for the year 2024, assessing the global flow of stablecoins.

The report reveals that North America has the largest stablecoin flow, amounting to $633 billion, followed by Asia-Pacific at $519 billion. When considering the proportion of stablecoin flow relative to GDP, Latin America and the Caribbean reach 7.7%, while Africa and the Middle East stand at 6.7%. Emerging markets (e.g., Latin America and the Caribbean, Africa and the Middle East) frequently use stablecoins due to capital controls and unstable domestic currencies, primarily for cross-border flows, with internal circulation accounting for only 12%-14%.

These data indicate that stablecoins have become an indispensable component of the global financial ecosystem, with primary application scenarios as follows:

1. Cross-Border Remittances and Settlements

Traditional cross-border remittances rely on the SWIFT system, involving multiple intermediaries such as banks and correspondent banks, resulting in slow speed, high fees, and low transparency. Stablecoins leverage blockchain technology to rebuild a highly efficient, low-cost global payment network through peer-to-peer transactions.

2. Daily Consumption

Southeast Asian ride-hailing platform Grab now supports users in Singapore and the Philippines topping up their GrabPay wallets with digital assets like USDC and USDT for everyday payments such as rides, food delivery, and coffee purchases.

E-commerce platform Shopify integrates Solana Pay, enabling users to pay using USDC on the Solana blockchain. As of May 2025, over 2,000 Shopify merchants have adopted Solana Pay.

3. Value Storage and Financial Yield Generation

The “value stability” feature of stablecoins makes them the foundational currency in the digital asset market, satisfying risk-averse needs while leveraging the technological characteristics of digital assets to spawn diverse financial applications, serving as a bridge between traditional and digital finance.

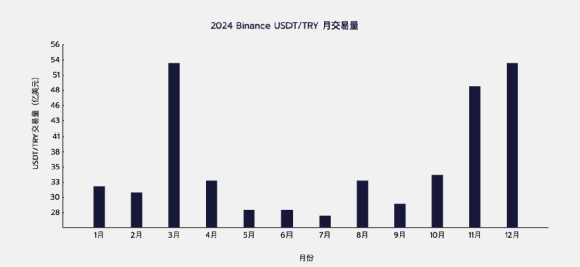

In countries experiencing high inflation in local fiat currencies (e.g., Argentina, Turkey), residents often convert their domestic money into stablecoins like USDT (pegged to the U.S. dollar) to hedge against currency depreciation. For instance, Turkey has long faced persistent inflation and currency devaluation, driving continuous growth in stablecoin and mainstream digital asset adoption. In 2024, the total trading volume of USDT/TRY (Turkish Lira) on Binance, the world’s largest digital asset exchange, surpassed $43.82 billion.

Figure 1-3: USDT-Turkish Lira Exchange Volume on Binance Exchange in 2024

Data Source: https://www.tradingview.com/symbols/USDTTRY/

Beyond hedging against fiat depreciation, stablecoins can also be used for financial yield generation. In decentralized finance (DeFi), stablecoin holders, after understanding the associated risks, may deposit stablecoins into decentralized lending protocols (e.g., Aave) to earn interest from borrowers, with annual yields determined by market demand. Alternatively, they can provide liquidity for stablecoin pairs like USDT-USDC on decentralized exchanges such as Uniswap and earn transaction fees.

1.4 Rise of Stablecoins and Regulatory Landscape

2025 is hailed as the “Year of the Stablecoin,” marking the transition of stablecoins from peripheral tools in digital asset trading to a central role in global finance. As digital assets pegged to fiat currencies or commodities, stablecoins offer price stability, low transaction costs, and efficient settlement, demonstrating disruptive potential across cross-border payments, supply chain finance, and asset tokenization, and emerging as a new focal point in the global financial infrastructure competition.

However, alongside rapid growth, stablecoins bring numerous potential risks, including challenges to monetary policy, financial stability, consumer protection, and illicit financial activities such as money laundering and terrorist financing. International financial institutions have maintained heightened concern over these risks. For example, the Bank for International Settlements (BIS) issued a stern warning in its report about the performance of stablecoins as widely used currencies, highlighting deficiencies such as lack of central bank backing, insufficient safeguards against illicit use, and inability to generate loans due to funding flexibility. BIS reports note that the anonymous nature of stablecoin holdings may facilitate hiding “dirty money,” and face risks of rapid redemptions by investors, potentially undermining monetary sovereignty and triggering capital flight from emerging economies.

To address the technological challenges and systemic risks posed by high liquidity, cross-border accessibility, and anonymity inherent in digital assets and stablecoins, the Financial Action Task Force (FATF) recommended in 2019 extending the Travel Rule to digital asset service providers, requiring them to adhere to the same transfer standards as banks. Under the Travel Rule, digital asset transactions exceeding a certain threshold (typically $1,000) must undergo KYC and due diligence procedures.

Various countries and regions have gradually advanced regulatory frameworks for digital assets based on FATF’s guidance, covering digital asset trading service providers, stablecoins, and digital asset custody. 2025 marks a turning point in global stablecoin regulation. The U.S. introduced the GENIUS Act, Hong Kong launched the Stablecoin Ordinance, most provisions of the EU’s MiCA Act took effect in 2025, and Japan and South Korea began evaluating the issuance of their own fiat-pegged stablecoins. The global stablecoin regulatory framework is gradually taking shape.

Chapter 2: Policy Research on Stablecoins

2.1 Analysis of Hong Kong's Stablecoin Regulatory Policies

Hong Kong has clearly articulated its strategic goal of becoming a leading global hub for digital asset innovation and investment. To achieve this vision, Hong Kong emphasizes establishing a robust and appropriate regulatory environment, viewing it as a prerequisite for sustainable and responsible development of the stablecoin ecosystem. This strategy leverages Hong Kong’s inherent advantages as an international offshore financial center, including a mature financial infrastructure in cross-border payments, asset management, clearing, and custody.

Hong Kong’s linked exchange rate system grants the Hong Kong dollar a high degree of stability, creating a solid monetary foundation for issuing stablecoins denominated in HKD and backed by fiat reserves. This strategic integration of digital assets into existing financial infrastructure and monetary systems indicates that Hong Kong does not view digital assets as entirely independent but rather seeks to embed them within established financial ecosystems. The stability of the HKD provides a credible anchor for stablecoins, enabling Hong Kong to stand out competitively against jurisdictions with less developed financial infrastructure or higher volatility in their fiat currencies.

2.1.1 Regulatory Objectives and Guiding Principles

The core objective of Hong Kong’s stablecoin regulatory framework is to mitigate potential risks posed by fiat-referenced stablecoins (FRS) to monetary policy, financial stability, and investor protection. Its guiding principle is “same activity, same risk, same regulation,” a concept deeply embedded in the Stablecoin Ordinance, ensuring regulatory requirements align with international standards while reflecting Hong Kong’s local context. This approach aims to promote healthy and orderly development of the digital asset market.

The regulatory framework also specifically addresses unique challenges posed by stablecoins, such as their anonymity and ease of cross-border use, which may increase AML and CFT risks. Combining the “same activity, same risk, same regulation” principle with a clear acknowledgment of stablecoin-specific risks (e.g., anonymity and cross-border nature) reflects the maturity of Hong Kong’s regulatory philosophy. This is not a simple transplantation of existing rules into the digital asset domain but a tailored adjustment recognizing functional equivalence with traditional financial instruments while adapting to the unique technical characteristics of digital assets. This meticulous approach aims to prevent regulatory arbitrage and ensure effective mitigation of emerging risks. If stablecoins function similarly to traditional financial instruments (e.g., payments, value storage), they should be subject to similar regulation to close potential regulatory gaps. However, their technical features (e.g., distributed ledger technology, potential anonymity) introduce new risks not fully covered by traditional rules. Therefore, the HKMA must adjust existing principles and introduce new measures (e.g., stringent AML/CFT requirements for DLT) to achieve comprehensive oversight.

2.1.2 Definition and Scope of Regulation

1. Clear Definition: "Fiat-Referenced Stablecoins (FRS)"

Hong Kong’s regulatory framework provides a clear definition of "stablecoin" and "fiat-referenced stablecoin (FRS)" to ensure precision and effectiveness in regulation.

Definition of "Fiat-Referenced Stablecoin (FRS)": FRS refers to stablecoins whose value is fully backed by one or more official currencies, HKMA-designated bookkeeping units, or economic store-of-value forms—or their combination—to maintain stable value. Currently, the scope of "designated stablecoins" is limited to fiat-referenced stablecoins. The regulatory framework covers both single-currency and multi-currency FRS.

The HKMA has focused its regulatory efforts primarily on FRS, reflecting a risk-based approach. FRS, especially those pegged to major fiat currencies, are considered to pose the most direct and significant risks to monetary and financial stability due to their widespread potential as payment instruments and their direct link to the traditional financial system. In contrast, stablecoins pegged to commodities (e.g., gold) or other digital assets typically have narrower use cases and smaller direct systemic impact. By prioritizing FRS regulation, the HKMA first addresses the most urgent regulatory needs and retains flexibility to expand the scope as the market evolves.

2. Licensing Requirement: Issuance Activities Require a License

In Hong Kong, any entity engaging in any of the following “regulated stablecoin activities” must obtain prior approval from the HKMA: issuing designated stablecoins during business operations in Hong Kong, issuing designated stablecoins overseas but pegged to the HKD, or actively promoting the issuance of fiat-referenced stablecoins to the public in Hong Kong.

The determination of "active promotion" involves a comprehensive assessment, including marketing language (especially Chinese usage), targeting of Hong Kong residents, use of Hong Kong domain names, and presence of detailed marketing plans. "Issuance" or "minting" generally refers to the initial recording and allocation of tokens to digital wallet addresses on a distributed ledger. The determination of "issuance in Hong Kong" also involves a holistic assessment, including day-to-day management and operational locations, incorporation location, minting and burning locations, reserve asset management location, and the location of bank accounts handling cash flows.

3. Treatment of Algorithmic Stablecoins: De Facto Exclusion

Hong Kong’s regulatory framework adopts a de facto exclusion stance toward algorithmic stablecoins. Due to the lack of actual reserve assets backing, algorithmic stablecoins cannot meet the HKMA’s strict reserve-related licensing conditions for FRS issuers. Although they may technically satisfy the definition of "designated stablecoin," their inability to meet minimum standards, particularly reserve requirements, effectively prevents them from obtaining a license.

This de facto exclusion of algorithmic stablecoins, despite their theoretical inclusion in the "designated stablecoin" definition, represents a strong prudential position. It reflects the global consensus among regulators post-Terra/Luna collapse that unsupported or under-collateralized stablecoins pose unacceptable systemic risks, placing financial stability and investor protection above speculative innovation. The HKMA’s approach aligns with international standards (e.g., FSB, BCBS recommendations), which emphasize that stablecoins used for payments must have adequate reserve support. By setting strict reserve requirements, the HKMA effectively filters out inherently unstable algorithmic models, signaling a cautious stance on innovation and placing financial stability first.

2.1.3 Licensing Framework for Fiat-Referenced Stablecoin Issuers

The cornerstone of Hong Kong’s stablecoin regulatory regime is a mandatory licensing framework imposing strict requirements on fiat-referenced stablecoin (FRS) issuers. The Stablecoin Ordinance establishes a “license-first” or “closed-loop” regulatory model emphasizing ex-ante authorization. This model is generally stricter than the “post-compliance” paths adopted in some other jurisdictions. The HKMA is the primary regulator, possessing comprehensive authority over licensing, audits, revocation of licenses, and issuing operational guidelines. The HKMA has the power to establish a “Designated Stablecoin List” and prohibit unauthorized stablecoins from circulating or being used for payments in Hong Kong.

The “license-first” approach, combined with the HKMA’s broad discretion (including the establishment of the “Designated Stablecoin List”), indicates a highly controlled and centralized regulatory environment in Hong Kong. This contrasts sharply with more lenient or decentralized regulatory philosophies, reflecting Hong Kong’s emphasis on prudential supervision and market integrity from the outset. By requiring pre-authorization, the HKMA can review the business model, financial soundness, and control systems of a stablecoin before it enters circulation, significantly reducing risks. The “Designated Stablecoin List” serves as a dynamic market control tool, allowing the HKMA to swiftly respond to emerging risks or non-compliant entities by restricting market access.

Obtaining and maintaining a Hong Kong stablecoin issuer license requires meeting a series of strict conditions and ongoing regulatory requirements designed to ensure the issuer’s sound operation and protection of stablecoin holders.

1. Corporate Status and Local Presence Mandate

FRS issuers must be companies incorporated in Hong Kong. Senior management teams and key personnel must reside in Hong Kong. Non-Hong Kong incorporated companies (except those already recognized and prudentially regulated) seeking an FRS issuer license must establish a subsidiary in Hong Kong.

2. Minimum Financial Resources and Capital Adequacy

FRS issuers must meet minimum financial resource requirements. The minimum paid-up share capital requirement is HK$25,000,000. The HKMA reserves the right to impose additional capital requirements when necessary. Retaining the discretion to impose extra capital ensures a flexible yet firm risk management stance. While sufficient capital buffers are crucial for financial stability, excessively high initial capital requirements could stifle innovation and hinder new entrants. This reflects a nuanced consideration balancing encouragement of participation with ensuring adequate financial support, acknowledging that the stablecoin market is still in its early stages.

3. Comprehensive Reserve Asset Management and Custody

FRS issuers must establish an effective stability mechanism. The total market value of reserve assets must never fall below the total face value of circulating FRS (i.e., full backing). Issuers should also consider the risk profile of their reserve assets and ensure adequate over-collateralization to provide a buffer. Reserve assets must be high-quality, highly liquid assets (e.g., bank deposits denominated in the reference currency). Reserve assets must be held in the same reference currency as the stablecoin, and each stablecoin’s reserve assets must be strictly segregated from the issuer’s other reserve pools and operational assets. Effective trust arrangements (e.g., appointing an independent trustee or issuing a trust declaration) must be established to ensure these assets are held for the benefit of stablecoin holders.

The HKMA will adopt a risk-based approach to assess the adequacy of reserve assets. The strict requirements for full backing, high liquidity, segregation, and sound trust arrangements are the bedrock of Hong Kong’s investor protection and financial stability strategy. This effectively imposes a “bank-like” prudential standard on stablecoin reserves, aiming to prevent liquidity crises and de-pegging events common in less regulated models. Past failures of stablecoins often stemmed from inadequate reserves, poor liquidity, commingling of funds, or insufficient legal protection for holders. By imposing these stringent requirements, the HKMA directly addresses these vulnerabilities, ensuring stablecoin holders have clear and enforceable rights to their underlying assets and that the peg can be maintained even under stress.

4. Robust Redemption Mechanism and Timeliness Standards

FRS holders must be able to redeem their stablecoins at face value promptly, without incurring undisclosed or disproportionate fees, or unreasonable redemption conditions. Redemption requests must be fulfilled within one business day of receipt. If an issuer anticipates being unable to meet a redemption request within one business day (e.g., due to unforeseen market pressure), they must seek prior approval from the HKMA.

The “within one business day” redemption standard sets a very high bar for FRS issuers’ operational efficiency and liquidity management. This directly addresses the inherent “run risk” of stablecoins, aiming to maintain confidence and prevent systemic contagion. Rapid redemption capability is crucial for maintaining the peg and preventing panic redemptions. By enforcing a strict one-day standard, the HKMA forces issuers to maintain highly liquid reserves and robust operational processes, minimizing the risk of liquidity mismatches that could destabilize the stablecoin.

5. Requirements and Impacts for Ordinary Users

For digital asset wallet holders or individuals considering entering the stablecoin market, the following points are noteworthy under Hong Kong’s stablecoin regulations:

(1) KYC/AML Requirements

Users must complete identity verification when using stablecoins issued by licensed Hong Kong stablecoin issuers or related platforms (exchanges, custodial wallets).

(2) Source of Funds Review

Large cross-border transfers or frequent transactions may trigger anti-money laundering scrutiny.

(3) Usage and Trading Restrictions

In Hong Kong, future stablecoin usage and trading may be subject to strict licensing constraints. According to HKMA requirements, users holding licensed stablecoins can redeem them at any time. Before the OTC Bill is enacted, ordinary users can still trade USDT and USDC on licensed digital asset platforms in Hong Kong (e.g., HashKey, OSL). However, it remains uncertain whether ordinary users will be allowed to trade unlicensed stablecoins like USDT and USDC under the future OTC licensing regime.

(4) Taxation Requirements

Hong Kong currently imposes no capital gains tax. Buying and selling stablecoins themselves are generally not taxed, but if used for commercial purposes (e.g., receiving payments, salary settlements), taxation is required.

2.1.4 Anti-Money Laundering (AML) and Counter-Terrorist Financing (CFT) Framework

1. Adherence to International Standards: FATF Recommendations and the “Travel Rule”

Hong Kong proactively adopts international standards in AML/CFT, particularly the recommendations of the Financial Action Task Force (FATF). Hong Kong’s updated AML framework, including regulations for virtual asset service providers (VASPs), aligns with FATF and its Recommendation 16—the “Crypto Travel Rule.” The Travel Rule applies to all digital asset transfers exceeding HK$8,000 (approximately $1,000). VASPs are granted a six-month window to comply, allowing for gradual integration and avoiding business disruption.

Hong Kong’s proactive implementation of FATF Recommendation 16 (the Travel Rule) demonstrates its commitment to global AML/CFT standards and its aspiration to be a responsible leader in digital asset regulation. This alignment enhances cross-border interoperability and reduces the risk of being perceived as a weak link in the global financial crime prevention network. The Travel Rule requires financial institutions and VASPs to transmit sender and beneficiary information during digital asset transfers, analogous to traditional wire transfers. By adopting this rule, Hong Kong enhances traceability, reduces anonymity, and addresses AML challenges arising from the cross-border and potential anonymity of stablecoins. This strengthens Hong Kong’s reputation as a compliant jurisdiction, crucial for attracting legitimate digital asset business.

2. Risk-Based Approach (RBA) for Money Laundering/Terrorist Financing Assessment and Mitigation

Licensed entities must adopt a Risk-Based Approach (RBA) when designing and implementing AML/CFT policies and procedures. An institution-level ML/TF risk assessment must be conducted, considering customer, country, product, and delivery channel risks. Assessments must be properly documented, approved by senior management, and kept up to date. Systems can be simplified for lower-risk scenarios, but simplification is not permitted when there is suspicion of money laundering or terrorist financing.

Adopting RBA allows for flexible and proportionate AML/CFT measures, adjusting controls based on the specific risk profiles of the issuer’s business model and customer base. This avoids a “one-size-fits-all” approach that might impose excessive burdens on low-risk activities while ensuring sufficient rigor for high-risk activities. The ML/TF risk associated with stablecoin activities can vary significantly. RBA enables issuers to allocate resources effectively, focusing on high-risk areas. This also reflects international best practices in AML/CFT, promoting effective risk mitigation without stifling legitimate innovation.

3. Wallet Management and Enhanced Customer Due Diligence (CDD)

Licensed entities must properly manage AML/CFT risks associated with wallets used by their clients for stablecoin transactions. They must identify client wallet addresses and verify ownership through micro-payments, message signature tests, or evidence obtained from custodial wallet providers.

For self-custody wallets provided by custodial wallet providers or used by financial institutions/VASPs, due diligence measures include collecting owner information, assessing their reputation and AML/CFT quality, and evaluating the adequacy of their control measures.

Detailed requirements for wallet management and CDD, including wallet ownership verification and due diligence on third-party wallet providers, directly address the challenge of pseudonymity in digital asset transactions. This is a critical step in bridging the gap between blockchain anonymity and financial transparency. One of the primary AML challenges in the digital asset space is the ability to transact with non-custodial wallets without clear identity. By requiring wallet ownership verification and due diligence on third-party providers, the HKMA mandates that issuers establish a clear link between stablecoin transactions and verified identities, significantly reducing anonymity risk and enhancing traceability.

4. Continuous Monitoring of Stablecoin Transactions and Mitigation Strategies for Illicit Activities

Licensed entities must monitor circulating stablecoins to prevent their use for illegal purposes, with monitoring intensity proportional to ML/TF risk. Stablecoin transactions are recorded on the blockchain, providing traceability to identify illicit activities. Possible measures include using blockchain analytics technology to continuously screen transactions and wallet addresses, blacklisting sanctioned or illegal wallet addresses, and freezing stablecoins upon request from regulatory or law enforcement agencies. Unless the licensed entity can demonstrate the effectiveness of these measures to the HKMA, the identity of every stablecoin holder must be verified by the licensed entity, a regulated financial institution/VASP, or a reliable third party.

The HKMA holds higher expectations for the effectiveness of blockchain analytics and blacklist mechanisms. In the absence of proof of AML technology effectiveness, the default requirement is to verify the identity of “every stablecoin holder,” indicating a highly conservative and risk-averse approach to emerging AML technologies. This suggests that relying solely on technological solutions may not suffice to meet Hong Kong’s stringent AML standards, and manual verification remains crucial. While blockchain analytics offers promising tools for identifying illicit activities, the HKMA acknowledges its limitations (e.g., difficulty identifying ultimate beneficiaries, reliance on external data). By prioritizing direct identity verification, the HKMA signals it will not compromise on fundamental AML principles, even when exploring technological advancements. Thus, the current Hong Kong stablecoin ecosystem maintains a robust “KYC” foundation.

2.2 Analysis of the U.S. Stablecoin Act

2.2.1 Definition and Scope of “Payment Stablecoins”

The GENIUS Act primarily regulates a specific category of digital assets known as “payment stablecoins.” These assets are typically defined as digital assets intended to serve as a means of payment or settlement, with issuers obligated to redeem or repurchase these assets at a fixed monetary value. The assets are not national currencies. A key aspect of the act is explicitly stating that payment stablecoins issued by authorized issuers are not considered “securities” under U.S. federal securities laws or “commodities” under the Commodity Exchange Act. This legislative exemption aims to establish a clear regulatory path for compliant stablecoins, largely removing them from the direct oversight of the U.S. Securities and Exchange Commission (SEC) or the Commodity Futures Trading Commission (CFTC).

This clear definition primarily targets fiat-backed stablecoins maintaining a 1:1 peg. Consequently, algorithmic stablecoins lacking a 1:1 reserve and relying on complex algorithms to maintain the peg likely do not qualify under this framework. This effectively excludes them from the “safe harbor” provided by the SEC/CFTC classification, potentially leaving them subject to existing securities or commodity laws.

Explicitly excluding compliant payment stablecoins from the definitions of “security” and “commodity” represents a significant step forward in regulation. This directly addresses one of the most persistent sources of regulatory uncertainty plaguing the U.S. crypto industry for years. By clearly defining regulatory classification, the act shifts the primary regulatory responsibility for these specific digital assets to banking regulators, rather than market regulators. This clarity aims to enhance confidence among traditional financial institutions and enterprises, encouraging their use of stablecoins for various purposes such as payments, cross-border transactions, and treasury management. It also creates a distinct niche within the broader digital asset market, where “payment stablecoins” are treated differently from other digital assets or tokenized assets, thereby establishing a more specialized and predictable regulatory environment for this particular asset class.

2.2.2 Core Prudential and Operational Requirements

1. Reserve Asset Management

Authorized Payment Stablecoin Issuers (PPSIs) are strictly required to maintain at least a 1:1 reserve, fully supporting the circulating payment stablecoins. Eligible reserve asset types include: U.S. coins and paper currency (including Federal Reserve notes), deposits at insured depository institutions or foreign depository institutions, short-term U.S. Treasury bills with maturities of 93 days or less, repurchase agreements collateralized by short-term U.S. Treasuries, certain reverse repurchase agreements, money market funds invested exclusively in the aforementioned eligible assets, and central bank reserve deposits. Notably, the act does not grant primary federal regulators the power to expand the list of eligible reserve assets, even if they believe other assets possess sufficient liquidity.

Reserve assets must not be pledged, re-pledged, or reused, except for the purpose of providing liquidity to meet reasonable expected stablecoin redemption requests. In such cases, short-term U.S. Treasury bills may be used as collateral for repurchase agreements, but these repurchase agreements must be cleared through an approved central clearing counterparty or receive prior approval from the relevant regulator. Reserve assets must be held by qualified third-party custodians and strictly segregated from the issuer’s operating funds. The issuer must publicly disclose monthly the total amount of circulating payment stablecoins and the amount and composition of reserve assets on its website. Monthly reports must be reviewed by a registered public accounting firm, and the CEO and CFO must certify the accuracy of the report; intentional false certification carries criminal penalties.

The strict limitation on reserve assets in the GENIUS Act, primarily restricting them to U.S.-denominated assets and U.S. Treasury bonds, is no accident. This provision clearly supports the dominant role of the U.S. dollar in the global digital economy and brings sustained demand to the U.S. Treasury market. This contrasts sharply with Hong Kong’s more flexible approach to reserve assets, reflecting a deeper strategic consideration in the U.S. regard for stablecoin regulation as a national economic instrument.

2. Redemption Mechanisms and Activity Restrictions

All authorized payment stablecoin issuers must establish a “timely” redemption procedure for circulating payment stablecoins and publicly disclose their redemption policies. The business activities of PPSIs are strictly limited, typically confined to issuing and redeeming payment stablecoins, managing related reserves, providing custody and safekeeping services, and other activities directly supporting these functions. The act also prohibits “tied sales,” meaning services cannot be offered contingent upon customers acquiring additional paid products or services from the issuer or its subsidiaries, or upon customers agreeing not to acquire any paid products or services. Additionally, stablecoin issuers are explicitly prohibited from offering any form of interest or yield to stablecoin holders. In the event of issuer bankruptcy, stablecoin holders have priority claims over all other creditors.

3. Capital, Liquidity, and Risk Management

Federal and state regulators are required to develop capital requirements rules tailored to the business model and risk profile of payment stablecoin issuers, with a $100 billion threshold dividing regulatory authority. Issuers must possess the technical capabilities, policies, and procedures to prevent, freeze, and reject illicit transactions and to comply with all applicable court orders. Regulators will also incorporate Bank Secrecy Act (BSA) and sanctions compliance standards into their risk management requirements. For banks holding stablecoins on their balance sheets, current U.S. banking rules may require holding additional capital. The act also specifies a timeline for rulemaking and implementation by regulators: unless otherwise stated, relevant rules must be promulgated by July 2026. The act’s effective date is the earlier of 18 months after enactment or 120 days after the primary federal stablecoin regulatory agency issues final implementing regulations, meaning the latest possible effective date is January 18, 2027.

4. Anti-Money Laundering / Counter-Terrorist Financing (AML/CFT) and Privacy Requirements

Under the GENIUS Act, authorized payment stablecoin issuers are designated as “financial institutions” under the Bank Secrecy Act (BSA). This means they must comply with strict AML, customer identification (KYC), and transaction monitoring requirements. They are also required to file Suspicious Activity Reports (SARs) with the Financial Crimes Enforcement Network (FinCEN) and comply with Office of Foreign Assets Control (OFAC) sanctions. In terms of privacy protection, the privacy requirements of the Gramm-Leach-Bliley Act (GLBA) apply to most authorized payment stablecoin issuers.

The comprehensiveness of the U.S. AML/CFT framework, including KYC, transaction monitoring, suspicious activity reporting, and sanctions compliance, undoubtedly imposes significant compliance costs on issuers. This may provide a competitive advantage to companies already possessing robust KYC, risk management, and regulatory change management procedures. This area is also a common point of strict regulation in both U.S. and Hong Kong regulatory frameworks.

2.3 Comparative Analysis of Hong Kong and U.S. Stablecoin Regulatory Frameworks

2.3.1 Regulatory Philosophy and Strategic Goals

As Hong Kong’s stablecoin licensing framework takes shape, increasing market participants are comparing it with the U.S. regulatory path. Differences in legal systems, financial positioning, and strategic goals between the two regions reflect varying risk appetites among regulators and distinct strategic visions for the future of digital finance. Below is a comparative analysis based on regulatory philosophy and strategic objectives.

Table 2-1: Comparison of Regulatory Philosophy and Strategic Goals between Hong Kong and the U.S.

| Dimension | Hong Kong | United States |

| Regulatory Model | Centralized under HKMA, with a licensing system to mitigate risks and foster innovation. | Decentralized, with multiple federal and state agencies involved, balancing risk and innovation. Over $100 billion regulated by the Fed; under $100 billion by state-level authorities. |

| Compliance Threshold | High barrier (HK$25 million paid-up capital requirement, strict redemption mechanisms), 100% high-liquidity assets, regular audits and public disclosure. | Limited to deposit institutions' subsidiaries/federal/state-qualified issuers. 1:1 cash/short-term treasuries, monthly public disclosure, prohibition on re-pledging. |

| Risk Attitude | Conservative, emphasizing payout guarantees and risk control, prohibiting algorithmic stablecoins. | More inclusive, encouraging innovation and tolerating some trial and error. |

| User Protection | Clear payout guarantees, protection of user priority rights and redemption rights, restricted to licensed institutions for sales, regulation of advertising behavior, relatively strict AML requirements. | Emphasis on investor protection and consumer safety, mandatory disclosure of reserves, key personnel required to submit monthly reports, strict AML requirements. |

| Strategic Goal | Establishment of an international regulatory-compliant stablecoin hub to reinforce Hong Kong’s status as an international financial center. | Strengthening the dominance of the U.S. dollar, promoting the application of dollar-pegged stablecoins and fiscal support. |

| Core Legislation | Stablecoin Ordinance (effective August 1, 2025) | Guiding and Establishing National Innovation for U.S. Stablecoins Act (effective July 18, 2025) |

2.3.2 Regulatory Structure and Authority

The U.S. stablecoin regulatory system is characterized by a dual-track model, featuring a complex, multi-tiered federal/state structure involving several federal banking regulators, such as the Federal Reserve, OCC, FDIC, and NCUA. Despite the establishment of the Stablecoin Certification Review Committee (SCRC) to promote coordination, this multi-agency model still risks regulatory fragmentation.

In stark contrast, Hong Kong adopts a centralized, unified regulatory model, with the Hong Kong Monetary Authority (HKMA) serving as the sole primary prudential regulator. This “one-stop” regulatory approach provides higher clarity and efficiency for market participants. For institutions seeking entry, Hong Kong’s centralized structure offers a clear path and transparent rules, contrasting with the potential complexity of navigating multiple states and federal agencies in the U.S., which could lead to higher compliance burdens for U.S. issuers.

2.3.3 Reserve Assets and Custody Requirements

In terms of reserve assets, both the U.S. and Hong Kong adhere to the 1:1 full backing principle, requiring stablecoins to be backed by high-quality, highly liquid assets. This is a universal consensus in global stablecoin regulation.

However, in practical execution, significant differences exist. The U.S. GENIUS Act imposes strict limitations on the types of eligible reserve assets, primarily restricting them to U.S. dollars and short-term U.S. Treasury bonds. Additionally, the act mandates that reserve assets be held by qualified third-party custodians and strictly segregated from the issuer’s operating funds. This strict restriction reflects the U.S. policy consideration of using stablecoins as a tool to consolidate dollar hegemony and support the U.S. Treasury market. Hong Kong, while emphasizing the quality and liquidity of reserve assets, offers greater flexibility. Although asset segregation is required, Hong Kong allows issuers to independently manage custody or delegate management to qualified institutions like banks. This flexibility aims to balance prudent regulation with market innovation, permitting a wider range of operational models while still ensuring asset security.

2.3.4 Retail Investor Access and Consumer Protection

The U.S. GENIUS Act aims to establish federal safeguards to protect the interests of stablecoin holders and enhance public confidence in the payment stablecoin market. Its consumer protection measures are reflected in strict requirements for reserve assets, transparent disclosures, and redemption mechanisms. Hong Kong, however, adopts a more rigorous and detailed investor protection strategy, particularly concerning retail investors. According to the Stablecoin Ordinance, only stablecoins issued by HKMA-licensed fiat stablecoin issuers can be sold to retail investors. Furthermore, Hong Kong imposes strict restrictions on stablecoin advertising to prevent fraud and misleading statements. This protective strategy is more cautious, aiming to isolate retail investors from the risks associated with stablecoin investments.

2.3.5 Cross-Border Collaboration and Reciprocal Arrangements

In terms of cross-border collaboration, both the U.S. and Hong Kong recognize the importance of international coordination. The U.S. GENIUS Act authorizes the Secretary of the Treasury to establish reciprocal arrangements or other bilateral agreements with foreign jurisdictions possessing “comparable” stablecoin regulatory regimes to facilitate international transactions and interoperability with U.S.-denominated stablecoins. In Hong Kong, the HKMA has the authority to assess on a case-by-case basis whether to modify or exempt certain minimum standards for applicants who are already adequately regulated in other jurisdictions. This is not automatic mutual recognition but a case-by-case prudent review. While both sides are committed to international cooperation, their differing reciprocal mechanisms may lead to friction in practice or require further bilateral agreements to achieve true seamless cross-border interoperability.

Despite both jurisdictions recognizing the necessity of cross-border cooperation, the lack of an immediate, automatic mutual recognition framework poses a significant challenge to the global adoption of stablecoins. This means issuers seeking to operate in both markets face a dual compliance burden, which could hinder the seamless flow of stablecoins in cross-border trade and payments and limit their full potential. The future success of stablecoins as a global payment rail depends on the actual implementation and breadth of these reciprocal arrangements.

2.3.6 Comparison of AML/CFT Policy Requirements

Table 2-2: Comparison of Anti-Money Laundering Regulatory Policies between Hong Kong and the U.S.

| Dimension | Hong Kong (Stablecoin Ordinance and accompanying guidelines) | United States (Federal BSA/FinCEN + State Rules/Potential Federal Law) |

| Regulated Entity | “Stablecoin issuers” must be licensed and treated as financial institutions under the AMLO; subject to the “Stablecoin Issuer AML/CFT Guidelines” | CVC (“convertible virtual currency”) “operators/exchangers” are MSBs under BSA and must register, establish AML systems; proposed federal stablecoin bill would explicitly designate issuers as BSA subjects |

| Risk Management | Explicit requirement for issuers to conduct institutional-level ML/TF risk assessments and design systems using RBA | BSA-based risk approach; FinCEN 2019 guidance requires MSBs to implement risk-based procedures and monitoring |

| CDD/KYC | Implement tiered CDD (including PEPs, purpose and nature, ongoing due diligence) for clients and beneficial owners; verify identity of every stablecoin holder | Conduct KYC/CDD and risk assessment on customers during stablecoin issuance and redemption, along with ongoing monitoring; file SARs/CTRs |

| On-Chain Transaction Monitoring | Require continuous monitoring of circulating stablecoins (including on-chain address screening, blockchain analytics, blacklists, and, where necessary, closed-loop (whitelist-only) circulation) | Emphasize transaction monitoring and suspicious reporting; propose additional record-keeping and reporting requirements (NPRM 311 special measures) for mixers |

| Travel Rule | AMLO adds a “Stablecoin Transfer” section: collect, retain, and transmit sender and recipient information for stablecoin transfers; prohibited from transferring with non-compliant VASPs/FIs; implement additional risk controls for non-custodial wallet transfers | Funds Travel Rule (31 CFR 1010.410(f)) applies to MSBs, requiring sender information for transactions ≥ $3,000; FinCEN document explicitly states CVC applicability |

| Record Keeping | Records must be retained for at least 5 years | Must comply with the 5-year retention requirement under BSA, including customer records, transaction records, SARs/CTRs, and supporting documents |

| Organization and Governance | Must establish a CO and MLRO; board or senior management must bear AML responsibility | Regulators expect banks or regulated entities to have sufficient BSA/AML governance and resources |

| Level of Hierarchy | Uniformly issued by HKMA for licensing and guidance | Federal level managed by BSA/FinCEN + existing state licensing framework (e.g., NYDFS BitLicense/Stablecoin Guidance); GENIUS Act/STABLE Act text explicitly defines issuers as BSA “financial institutions” |

2.4 Other Countries and Regions’ Stablecoin Regulatory Policies

2.4.1 Singapore’s Stablecoin Regulatory Policy

The Monetary Authority of Singapore (MAS) released the Stablecoin Regulatory Framework in 2023, though it has not yet been codified into law. In 2025, MAS plans to conduct public consultations and draft amendments to formalize the framework. Until the revised legislation is implemented, Singapore relies on the existing Payment Services Act (PSA) and the Stablecoin Regulatory Framework to regulate stablecoins.

The PSA clarifies the definition of stablecoins, entry thresholds, reserve assets, and redemption mechanisms. The subsequent release of the Stablecoin Regulatory Framework extends regulation to single-currency stablecoins pegged to the Singapore dollar or G10 currencies issued in Singapore, adding new regulatory requirements for stablecoin issuance services, further safeguarding the rights of stablecoin holders and mitigating financial risks.

Under the Stablecoin Regulatory Framework, stablecoin issuers must comply with the following regulatory requirements:

- 1. Reserve Asset Requirements

- l Composition: Cash/equivalents, low-risk bonds with remaining maturities ≤ 3 months (issued by governments, central banks, or AA- rated international institutions), ensuring asset value stability;

- l Valuation: Marked-to-market daily, with value ≥ 100% of circulating SCS face value, preventing redemption risks due to insufficient reserves;

- l Custody: Isolated accounts must be held at custodians rated A- or higher, preventing misuse of reserve assets;

- l Auditing: Monthly independent audit + annual audit, enhancing transparency and reducing market trust risks.

- 2. Capital Requirements

- l Base Capital: ≥ SGD 1 million or 50% of annual operating expenses (whichever is higher), ensuring the issuer has sufficient financial strength to withstand operational risks;

- l Solvency: Liquid assets ≥ 50% of annual operating expenses or amount needed for liquidation (verified annually by independent auditors), ensuring orderly redemption even in extreme circumstances.

- 3. Anti-Money Laundering Requirements

- l Stablecoin issuers and intermediaries must strictly comply with AML/CFT regulations, including Customer Due Diligence (CDD), transaction monitoring, and reporting large and suspicious transactions.

Notably, Singapore’s Stablecoin Regulatory Framework exhibits a “voluntary” characteristic: stablecoin issuers can choose whether to apply to MAS for certification and become a “MAS-regulated stablecoin,” and those choosing not to follow this path can continue operating as “digital payment tokens” under the PSA framework. The upcoming amendment bill may still adhere to the previous voluntary nature of stablecoin regulation, providing flexibility for different stablecoin issuers.

2.4.2 Japan’s Stablecoin Regulatory Policy

Japan has built a stablecoin regulatory system based on “issuer limitation + reserve transparency + full-process monitoring,” emphasizing a balance between compliance and innovation. Its core logic is integrating stablecoins into the traditional financial regulatory framework, reducing money laundering risks through KYC, travel rules, and asset segregation, while planning to enhance the competitiveness of its stablecoins through flexible reserve investment (e.g., allowing up to 50% in government bonds).

According to the revised provisions effective June 2023, fiat-pegged stablecoins are classified as “Electronic Payment Instruments” (EPIs) and must comply with strict AML and CFT obligations. This institutional design aims to balance compliance, financial stability, and innovative development.

1. Core AML Requirements

- l Customer Identity Verification (KYC) and Transaction Record Keeping: Stablecoin issuers and intermediaries (e.g., exchanges) must verify user identities, including name, address, and identification documents, and record information on both parties involved in transactions. For example, stablecoins issued by fund transfer service providers have a per-transaction limit of 1 million JPY, and recipients must undergo KYC verification.

- l Transaction Record Keeping: Must retain user information and fund flow details for at least five years.

- l Suspicious Transaction Reporting (STR): If unusual transactions are detected, they must be reported to the Japanese Financial Intelligence Center (JAFIC), which may result in criminal liability.

- l Travel Rule: Since June 2023, stablecoin transfers across borders or between platforms must include sender and recipient identity information to prevent anonymous fund movement.

2. Regulatory Oversight of Intermediaries and Business Categories

Entities engaged in stablecoin trading, conversion, or custody must register with the Financial Services Agency (FSA) as an EPISP and meet capital adequacy and system security requirements. For example, exchanges supporting stablecoin trading must regularly undergo reviews by the Japanese Virtual Asset Trading Association (JVCEA).

3. User Asset Protection and Bankruptcy Response

- l Domestic Asset Preservation Order: In the event of issuer or exchange bankruptcy, the FSA can order user assets to be retained within Japan, preventing cross-border transfers. This mechanism was applied during the 2022 bankruptcy of FTX Japan, ensuring user assets were not affected by overseas liquidation.

- l Reserve Fund Safeguarding and Independent Audit: Issuers must fully back stablecoin issuance with demand deposits or highly liquid assets (e.g., government bonds), and must have their reserve funds verified quarterly by a third-party auditor. For instance, the first JPY-pegged stablecoin, JPYC, expected to be approved by the Japanese Financial Services Agency in autumn 2025, plans to publish reserve proofs monthly and implement Hardware Security Modules (HSMs) for private key management.

- l International Standards and Cross-Border Collaboration: As a FATF member, Japan has fully implemented the “Travel Rule” and is conducting stablecoin interoperability and cross-border compliance cooperation with South Korea, ASEAN, and the G20. This strategy strengthens AML/CFT international consistency and promotes the compliant application of Japanese stablecoins in the global market.

2.4.3 South Korea’s Stablecoin Regulatory Policy

1. Legislative Implementation and Background

The Virtual Asset User Protection Act (VAUPA) was announced on July 18, 2023, and came into effect on July 19, 2024, marking the first dedicated legislation in South Korea to regulate digital asset platforms. The draft Digital Asset Basic Act, proposed on June 10, 2025, aims to further expand the regulatory scope, including clarifying the stablecoin issuance framework and regulatory standards. This reform stems from the market trust crisis triggered by the Terra-Luna collapse in 2022, with the legislative intent to strengthen compliance foundations and risk control systems.

2. Regulatory Authorities and Compliance Requirements

The Korea Financial Intelligence Unit (KoFIU), also known as the Financial Intelligence Agency, is responsible for overseeing the registration of digital asset service providers and conducting AML/CFT compliance reviews;

The Financial Services Commission (FSC) and the Financial Supervisory Service (FSS) oversee market operations, protect user rights, and enforce on-site regulatory actions.

3. AML/CFT Regulatory Compliance Measures

South Korea enforces highly detailed AML/CFT regulations on digital asset service providers. All such providers must register with KoFII prior to commencing operations, obtain ISMS (Information Security Management System) certification, and open accounts with financial institutions that support real-name banking. Failure to complete these requirements may result in KoFIU rejecting the registration application; no digital asset business activities are permitted before registration is finalized. Customer Identification (KYC) and Customer Due Diligence (CDD) are fundamental prerequisites. Digital asset service providers must verify user identities before account opening or when transaction volumes reach 1 million KRW (approximately $700 USD), and must enhance due diligence for high-risk users. The Travel Rule has been enforced since March 25, 2022, requiring digital asset service providers to provide sender and receiver names and wallet addresses when transferring funds ≥1 million KRW to another digital asset service provider. In cases where required by the registration authority or official request, identity documentation—including identification numbers—must be submitted within three working days. Records must be retained for five years; violations may incur fines up to 30 million KRW. Suspicious Transaction Reports (STRs) and transaction monitoring systems are mandatory. Providers must report any suspicious transactions to KoFIU or FSS upon detection.

4. User Asset Protection Mechanisms

Asset Segregation Requirement: Digital asset service providers must maintain user assets separately from platform-owned assets to prevent user losses in case of platform insolvency.

Bankruptcy Trust and Preservation Mechanism: In the event of a digital asset service provider’s bankruptcy, the FSC/FSS may issue an asset retention order to ensure user assets remain in South Korea, protecting them from foreign liquidation proceedings.

Reserve Transparency and Auditing: Stablecoin issuers must maintain full collateralization of issued stablecoins by underlying assets, conduct regular audits, and enhance transparency in disclosing reserve holdings.

5. Strategic Trends and International Cooperation

In July 2025, the Bank of Korea established a dedicated "Digital Assets Task Force" to strengthen policy responsiveness, monitor international developments in stablecoin regulation (e.g., the U.S. GENIUS Act), and prepare for future legal institutionalization.

Media reports indicate the government plans to submit a “second phase” VAUPA tax bill in October 2025, covering stablecoin issuance, secure custody, and internal control mechanisms, further refining the regulatory framework.

2.4.4 UAE Stablecoin Regulatory Policy

The UAE divides token regulation among the Dubai Virtual Assets Regulatory Authority (VARA), the Abu Dhabi Financial Services Regulatory Authority (FSRA), and the Securities and Commodities Authority (SCA). In 2024, the Central Bank of the UAE introduced the Payment Token Services Regulations (PTSR), formally bringing stablecoins under regulatory oversight.

Stablecoin Definition: The UAE Central Bank explicitly classifies stablecoins as "payment tokens." A payment token is a digital asset whose value is maintained through pegging to fiat currency or another payment token denominated in the same fiat currency.

Stablecoin Issuance: Includes Dirham-pegged and foreign-currency-pegged stablecoins. Entities issuing Dirham-pegged stablecoins must obtain a payment token issuance license from the UAE Central Bank. Key conditions include being registered under Federal Law No. 2 of 2015 on Commercial Companies in the UAE; ensuring stablecoin issuance is fully backed by independent reserve assets; and undergoing independent audits and financial disclosures. Foreign entities issuing stablecoins pegged to non-dirham currencies must register with the UAE Central Bank as foreign payment token issuers. Additionally, foreign-currency stablecoins are restricted to digital asset transactions only and cannot be used for goods/services or domestic payments within the UAE.

Stablecoin Custody and Transfer: Must be licensed by SCA or any local licensing authority as a digital asset service provider. Individuals providing custody services for digital assets may apply for a non-objection registration to execute stablecoin custody and transfer. Any other party seeking to perform payment token custody and transfer must obtain a license from the central bank.

Stablecoin service providers holding licenses must meet the following requirements when engaging in stablecoin custody/transfer or stablecoin exchange services:

If the monthly average value of stablecoin transfers initiated, facilitated, executed, guided, or received as part of their stablecoin services reaches or exceeds 10 million AED, they must hold at least 3 million AED in regulatory capital;

If the monthly average value of payment token transfers falls below 10 million AED, they must hold at least 1.5 million AED in regulatory capital.

Additionally, the Payment Token Services Regulations apply to natural or legal persons offering "payment token services" in the UAE but do not cover financial free zones such as DIFC and ADGM. Currently, the Dubai Financial Services Authority (DFSA) has approved the use of USDC, EURC, and RLUSD in the DIFC region.

2.5 Chapter Summary

Overall, this chapter systematically compares the stablecoin regulatory frameworks of Hong Kong and the United States, while reviewing policies across other jurisdictions (such as Singapore, Japan, South Korea, and the UAE), revealing current trends in international stablecoin regulation regarding differences and convergence in philosophy, objectives, and institutional design.

First, in terms of regulatory philosophy and strategic goals, Hong Kong primarily prioritizes financial stability and systemic risk mitigation, emphasizing licensing regimes, reserve transparency, and end-to-end AML/CFT controls—reflecting a "risk-first" cautious model. The U.S., meanwhile, applies BSA horizontally and recently attempts to establish a federal-level stablecoin regulatory framework via the GENIUS Act, aiming to safeguard the dollar's core role in global payment systems and gradually strengthen prudential requirements on issuers. Singapore's approach balances innovation encouragement with risk control; Japan’s regulation follows traditional financial licensing logic, with banks and trust institutions as primary issuers; South Korea emphasizes investor protection and holds exchanges and issuers accountable for compliance; the UAE adopts a "regulatory sandbox + segmented regulation" model, showcasing strong institutional flexibility and a preference for attracting foreign investment.

Second, in regulatory tools and institutional arrangements, Hong Kong provides clearer definitions of stablecoins, mandating pegging to fiat currency and imposing strict rules on reserve asset custody, consumer redemption guarantees, and cross-border cooperation. The U.S. focuses more on functional orientation, particularly in AML/CFT (e.g., Travel Rule, SAR/CTR reporting) and consumer protection, forming a multi-layered, multi-agency regulatory policy. Other countries like Singapore, Japan, and South Korea have also incorporated AML/CFT obligations and investor protection measures into their regulatory frameworks, though each varies in emphasis and openness.

Based on the above analysis, current stablecoin regulatory approaches across jurisdictions mainly fall into three types: First, those exemplified by Hong Kong and Japan emphasize ex-ante regulation and financial stability; second, represented by the U.S., focus on function-based regulation, seeking balance between compliance and market development; third, led by Singapore and the UAE, adopt flexible regulatory models, promoting innovation through pilot projects and regulatory sandboxes. As stablecoins increasingly embed into cross-border payments and financial market infrastructure, future convergence in AML/CFT cooperation, reserve transparency, and cross-border recognition mechanisms among different jurisdictions appears likely.

Chapter Three: Financial Security Risks Facing Stablecoins

3.1 Risk Characteristics of Stablecoins

- 1. Anonymity and Tracing Challenges

Due to their anonymity, rapid cross-border transaction capabilities, and complex regulatory environments, stablecoins are increasingly exploited by criminals across various scenarios, posing new challenges to financial order and social security. Their risk characteristics are primarily manifested in the following aspects:

Criminals leverage the anonymous addresses and intricate transaction behaviors of stablecoins to increase tracing difficulty. By splitting transactions, using mixing techniques (e.g., Tornado Cash), and transferring funds via cross-chain bridges, they create complex fund flow paths, making it difficult for regulators to trace the origin and destination of funds. This technical feature provides natural cover for illicit activities such as money laundering and terrorist financing.

- 2. Inherent Risks of Algorithmic Stablecoins

Algorithmic stablecoins maintain price stability through smart contract mechanisms dynamically adjusting supply and demand (minting/burning). However, under extreme market pressure, this mechanism may fail, leading to severe price volatility or even de-pegging, triggering systemic market and social risks. For example, the “UST collapse event”: Terra’s algorithmic stablecoin TerraUSD (UST), which was pegged 1:1 to the U.S. dollar, lost its peg due to market panic and massive withdrawals. UST’s price plummeted from $1 to $0.05 within hours, causing the LUNA token’s value to crash, resulting in over $50 billion in market cap destruction. This event exposed the structural vulnerabilities of algorithmic stablecoins, prompting global regulators to intensify oversight.

- 3. Smart Contract Vulnerabilities

If smart contract code contains flaws or malicious backdoors, it can lead to theft or unauthorized manipulation of funds. Common vulnerabilities include inadequate input validation, calculation errors, and missing access controls.

- 4. Functional Deficiencies in Smart Contracts

Some stablecoin projects lack essential control features in their design, such as freezing functions or transaction limits, preventing timely intervention when suspicious activity is detected.

- 5. Abuse of Privacy-Enhancing Technologies

Privacy-enhancing technologies like zero-knowledge proofs (ZKP) improve transaction confidentiality but may also be used to fully anonymize transaction details, increasing tracing difficulty. Criminals exploit such technologies to conceal transaction pathways, creating a "technical black box" that prevents regulators from obtaining actionable intelligence, resulting in compliance blind spots.

- 6. Regulatory Arbitrage and Cross-Border Regulatory Risks

Stablecoin issuers often choose to register in jurisdictions with lax regulations, designing structures to evade scrutiny and reduce operational costs. This regulatory arbitrage can render domestic supervision ineffective, creating transnational regulatory vacuums and posing significant challenges to international anti-money laundering (AML) and counter-terrorist financing (CTF) cooperation.

- 7. Classification of Risk Activities

From the perspective of social harm caused by stablecoin-related incidents, risk activities include:

Illegal Activities: Such as terrorist financing, human trafficking, drug trafficking, ransomware attacks, fraud, identity theft, and impersonation scams.

Suspicious Activities: Including darknet markets, unlicensed gambling, and the use of mixers.

3.2 Illegal Activity Risks

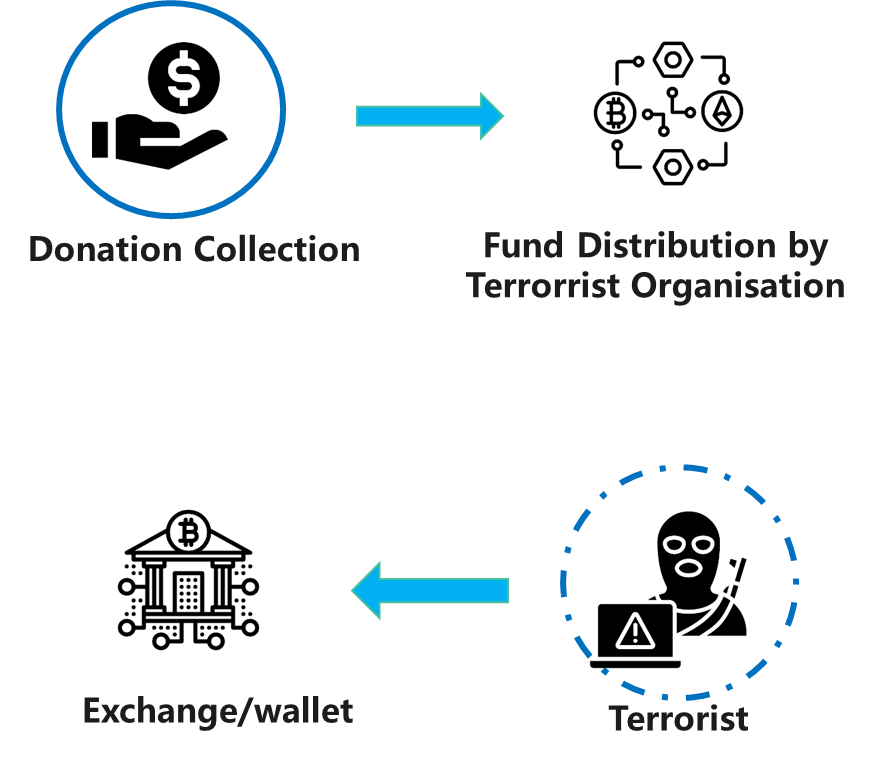

3.2.1 Terrorist Financing

On April 3, 2025, the U.S. Department of Treasury’s Office of Foreign Assets Control (OFAC) announced the addition of eight Tron wallet addresses linked to Yemen’s Houthi movement to the Specially Designated Nationals (SDN) list, accusing them of using Tether (USDT) for illicit financial activities.

According to Treasury disclosures, this illicit financial network was orchestrated by Sa’id al-Jamal, a senior financial officer of the Houthi movement based in Iran, who has been designated a Global Specially Designated Terrorist since 2021. His network is involved in procuring Russian weapons, stolen Ukrainian grain, and other sensitive goods, shipping them to Houthi-controlled areas.

On June 15, 2025, Tether, the issuer of USDT, froze 12.3 million USDT directly targeting Houthi-linked wallet addresses.

The Houthi case demonstrates that digital assets have become a key tool for terrorist financing and arms trading. Their anonymity, fast settlement, and cross-chain characteristics provide loopholes for criminals to evade sanctions.

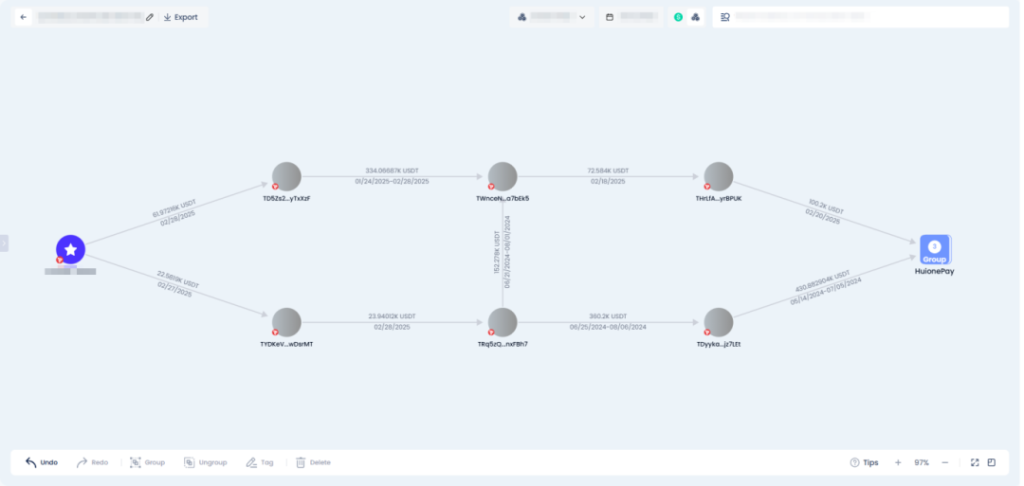

Figure 3-1 Diagram of Terrorist Financing Fund Flow

3.2.2 Human Trafficking and Drug Trafficking

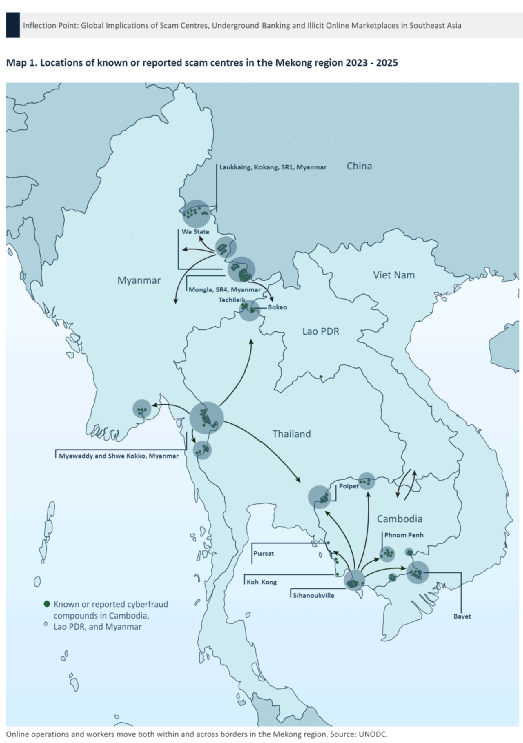

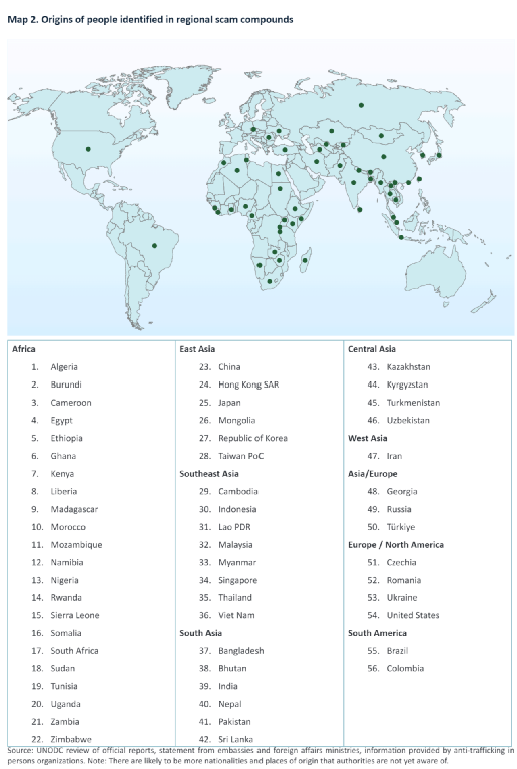

Early in 2025, we provided partial information, data, and analysis support for a report by the United Nations Office on Drugs and Crime (UNODC) titled “Inflection Point: Global Implications of Scam Centres, Underground Banking and Illicit Online Marketplaces in Southeast Asia.” The report indicates that transnational organized crime in Southeast Asia is growing faster than ever in history.

This is first evident in synthetic drug production data: over the past decade, methamphetamine supply from Myanmar’s Shan State has risen annually to record highs. Meanwhile, industrial-scale networks of fraud and scams driven by interconnected webs of complex multinational syndicates, money launderers, human traffickers, data brokers, and an increasing number of other professional service providers and accomplices have surged.

Asian criminal groups have become authoritative leaders in global online fraud, money laundering, and underground banking, actively strengthening collaboration with other major criminal networks worldwide. The emergence of new illicit online markets in Southeast Asia has further exacerbated the situation, greatly expanding sources of criminal income and enabling transnational organized crime to scale up. These platforms not only create new opportunities for criminal operations abroad but are increasingly used by criminal groups outside Southeast Asia to launder money and circumvent formal financial systems. These network fraud and other cybercrimes are closely linked to forced human trafficking. Meanwhile, major criminal groups collude with one another, infiltrating casinos, special economic zones, commercial parks, and various traditional financial and digital financial services—establishments proven capable of providing all necessary conditions, infrastructure, and regulatory, legal, and fiscal safeguards for sustained growth and expansion.

Under this context, many criminal organizations already operating at substantial scale within Southeast Asia and continuing to expand globally have rapidly diversified into multiple critical infrastructure sectors. This goes far beyond building and managing physical scam centers; their operations now include online gambling platforms and software services, illegal payment platforms and digital asset exchanges, encrypted communication platforms, stablecoins, blockchain networks, and illicit online marketplaces—all typically controlled by the same criminal network. These organizations have also developed large multilingual workforces comprising hundreds of thousands of victims of human trafficking and accomplices.

These developments have rapidly expanded the victim base of Asian criminal groups to a global scale, intensifying the challenges faced by law enforcement agencies.

Figure 3-2 Map of Scam Hubs and Human Trafficking in the Mekong River Basin from the Report

Figure 3-3 Distribution of Victims’ Origins in the Report on Human Trafficking

Report Access Link: “Inflection Point: Global Implications of Scam Centres, Underground Banking and Illicit Online Marketplaces in Southeast Asia”

3.2.3 Ransomware Attacks

Attackers encrypt victims’ device data and demand ransom payments in BTC or other digital assets to restore access. Due to their anonymity, cross-border payment convenience, and irreversible transactions, stablecoins are frequently used by ransom gangs for money laundering after receiving ransoms.

Risk Case: On March 7, 2025, the U.S. Department of Justice (DOJ) joined forces with German and Finnish authorities to seize Russia-based digital asset exchange Garantex, which had been investigated multiple times for allegedly helping ransomware gangs launder money. It is reportedly deeply connected to the global cybercrime economy, with previously destroyed ransomware groups like Conti relying on Garantex for money laundering. The exchange helped ransomware operators clean stolen digital assets by converting Bitcoin into USDT and then transferring it to other exchanges for conversion into USD and other fiat currencies.

3.2.4 Fraud and Identity Theft

Identity theft and fraud are among the most serious cybercrimes, potentially causing long-term, devastating, and irreparable consequences for affected individuals, groups, and companies. In recent years, stablecoins—due to their broad consensus and rapid transaction speed—are increasingly appearing in related scenarios such as hacking tool sales, illegal rental of personal accounts, illegal trade of personal information, fraudulent victim payments, and extortion payments.

Risk Case:

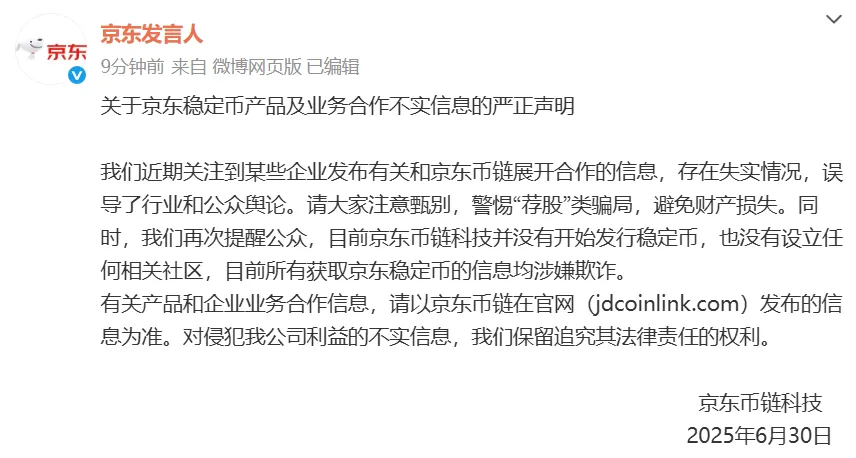

1. Fraudulent Activities Using Stablecoins as a Hook: With the implementation of Hong Kong’s Stablecoin Ordinance, the concept of "stablecoin" has gained significant attention. However, during market euphoria, illegal activities exploiting the "stablecoin" narrative have already begun emerging.

For example, since July 2025, financial regulators and industry self-regulatory bodies in Zhejiang, Shenzhen, Beijing, Suzhou, Chongqing, Ningxia, Henan, and other regions have repeatedly issued risk warnings, emphasizing that "stablecoins" are being misused by criminals, highlighting the need for heightened vigilance. Hong Kong regulators have also issued repeated warnings urging the public to beware of scams exploiting the stablecoin concept. Furthermore, authoritative media outlets such as Economic Daily have concentrated coverage on the risks associated with stablecoins.

Recently, numerous scams have emerged under the banner of "JD Stablecoin," claiming "state-owned background," "guaranteed profits," and "endorsed by Dong Ge." Some even posted "profit screenshots" to urge quick participation. JD’s official team has issued two statements clarifying that the so-called "JD Stablecoin" has not yet been launched, and all related investment information circulating online is fraudulent.

Figure 3-4 Fake JD Stablecoin

2. Fraudulent Activities Using Stablecoins as a Channel: On June 26, 2025, the “Xinkangjia” investment platform, purportedly backed by the “Dubai Gold Exchange (DGCX)” and promising a daily return of 1%, collapsed suddenly. The platform had offices across China (Guizhou, Suzhou, Chongqing, Sichuan, Xiangtan, Shenzhen), with involved amounts reaching hundreds of billions and affecting approximately 2 million investors.

DGCX Xinkangjia used USDT for project participation and fund settlement. Registration required an invitation code and spread almost exclusively through personal networks. Participants had to pay a minimum of 1,000 USDT as an entry fee, requiring them to purchase USDT themselves for top-up. However, due to operational complexity, most newcomers directly exchanged their USDT for RMB and transferred the funds to their superiors. The USDT deposited by users entered the platform-controlled private wallets directly.