Circle Releases White Paper on "Stablecoin Payment Network"

Circle Releases White Paper on "Stablecoin Payment Network"

Author: Will Awang, Web3 Legal

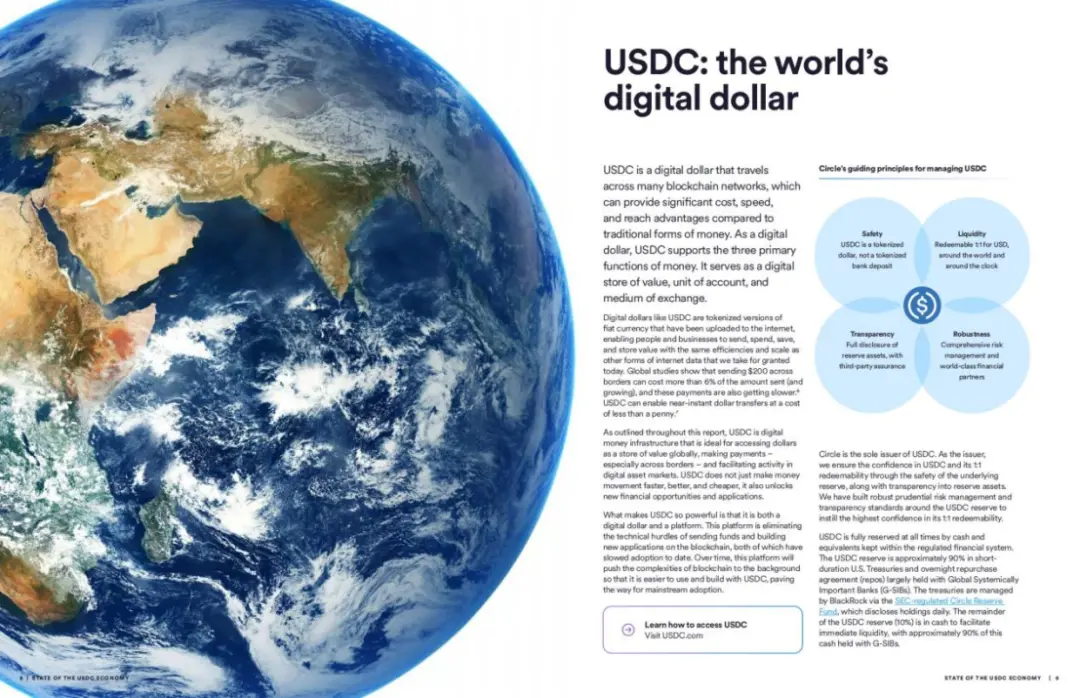

In the January 2025 report “Digital Dollar on the Value Internet — 2025 USDC Market Economy Report” released by Circle, the threefold narrative of USDC was clearly defined: (1) financial upgrading of the internet; (2) an interconnected network via USDC; and (3) leveraging network effects to expand USDC use cases.

Given Circle’s current stablecoin market share of 26%, it is evidently no longer satisfied with just the first two narratives. Thus, its recently launched Circle Payments Network represents Circle’s strategic move as a globally compliant stablecoin issuer to capture value from USDC—or more broadly, stablecoins—within the global digital network.

The U.S. dollar itself, along with the internet, inherently possesses strong network effects. In both the physical world and cyberspace, the U.S. dollar functions as a currency with network effects. Blockchain technology endows USDC with superior functionality and new application potential compared to traditional fiat dollars, while leveraging existing internet infrastructure for real-world deployment.

Circle is building an open technological platform centered around USDC, leveraging the current dominance and widespread adoption of the U.S. dollar, and fully utilizing the scale, speed, and cost advantages of the internet to achieve similar network effects and practicality in financial services.

Circle Payments Network is a framework where Circle, leveraging its robust compliance background, aggregates financial institutions (USDC service providers) within a compliant, seamless, and programmable ecosystem to coordinate global payments involving fiat currencies, USDC, and other payment stablecoins.

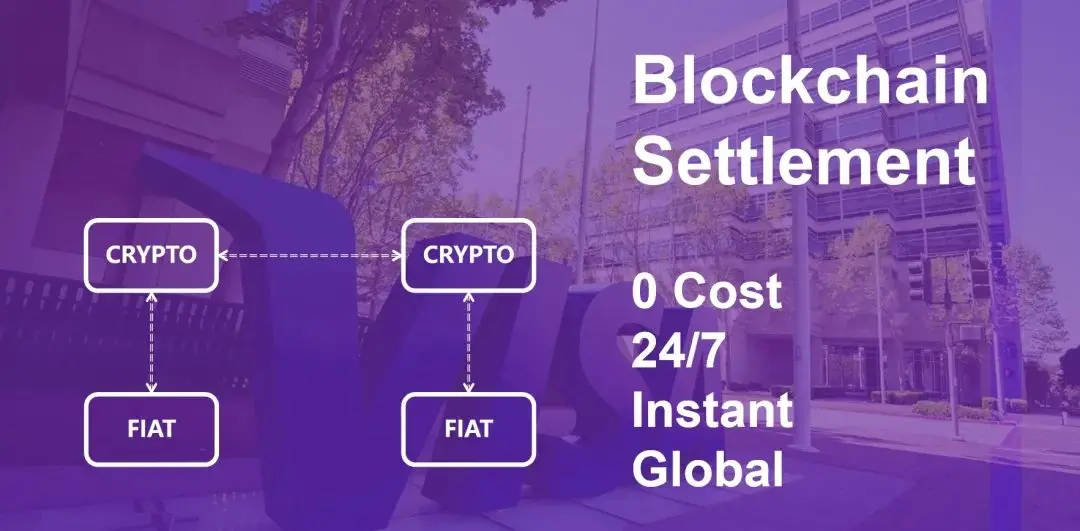

Thus, fiat currencies no longer need to rely on outdated traditional SWIFT systems for circulation—the digital dollar, built on blockchain as the settlement layer, will become its new pathway.

Fundamentally, Circle’s blockchain-based payment network serving as a settlement layer is a eulogy for legacy payment corridors like SWIFT / VISA / Mastercard, heralding a massive era of transformation—from postal mail to email, from horse-drawn carriages to electric vehicles, from transatlantic telegraph cables to blockchain-powered internet value transfer.

Crucially, Circle positions Circle Payments Network (CPN) as a novel protocol layer built upon a comprehensive, open, and internet-native settlement system, with stablecoins at its core. This positioning enables compatibility across multiple settlement-layer blockchains, avoiding the trap of competing over financial infrastructure supremacy.

Dr. Xiao Feng of Hashkey, starting from the essence of finance, defines blockchains as next-generation financial infrastructure—not merely marginal improvements to existing systems, but transformative shifts across trading, clearing, and settlement, forming a new financial paradigm.

Notably, Circle aims to build an open network based on blockchain, already showing early signs of a VISA-like network. Future evolution may offer glimpses into answers found in VISA’s historical development. This stands in stark contrast to the relatively closed ecosystems of Ripple & RippleNet and Stripe & Bridge.

In October 2023, when I presented to Ant Group on Web3 Payments, I was pondering whether bridging fiat assets onto-chain and settling via stablecoins could be a superior solution. Clearly, one and a half years later, Circle has provided a definitive answer—and a compelling use case.

Thus, this article compiles Circle’s Circle Payments Network Whitepaper to explore its design principles, real-world use cases, future potential use cases and growth opportunities, and the governance model of this VISA-like network organization.

I. Whitepaper Overview

Stablecoins have long been considered capable of becoming the foundation for payments and capital flows on the internet. However, until recently, stablecoins—functioning as digital cash—were primarily used within global digital asset markets and decentralized finance (DeFi).

With the launch of Circle Payments Network (CPN), Circle is advancing stablecoins further, unlocking their potential to upgrade the global payment system—just as past internet innovations transformed media, commerce, software, communications, and other industries. These transformative changes greatly enhanced customer experience, reduced costs, increased speed, and drove economic growth for individuals and businesses worldwide.

To realize this potential, Circle Payments Network (CPN) as infrastructure aims to overcome many barriers that have previously limited stablecoin adoption in mainstream payments. These include entry barriers, ambiguous compliance requirements, technical complexity, and concerns about secure storage of digital cash.

Circle Payments Network (CPN) brings financial institutions together within a compliant, seamless, and programmable framework to coordinate global payments involving fiat, USDC, and other payment stablecoins.

Corporate and individual clients of these financial institutions can enjoy faster and lower-cost payment services compared to traditional payment systems, which are often constrained by fragmented networks or closed systems. Crucially, Circle Payments Network (CPN) establishes the infrastructure foundation for the entire ecosystem, eliminating much of the technical complexity and operational hurdles that have impeded mainstream stablecoin adoption—including the need for enterprises to self-host stablecoins. CPN also opens the door to breakthroughs in programmable money, unlocking entirely new use cases for currency in global value exchange.

This whitepaper outlines the design principles of Circle Payments Network (CPN), summarizes initial and near-term use cases, and proposes future potential use cases and growth opportunities. The aim is to help financial institutions, payment companies, app developers, innovators, and other stakeholders understand their roles in building and leveraging CPN—and how the network enables them to innovate and deliver stablecoin benefits to their customers.

II. Introduction

2.1 Deficiencies of the Global Financial Payment System

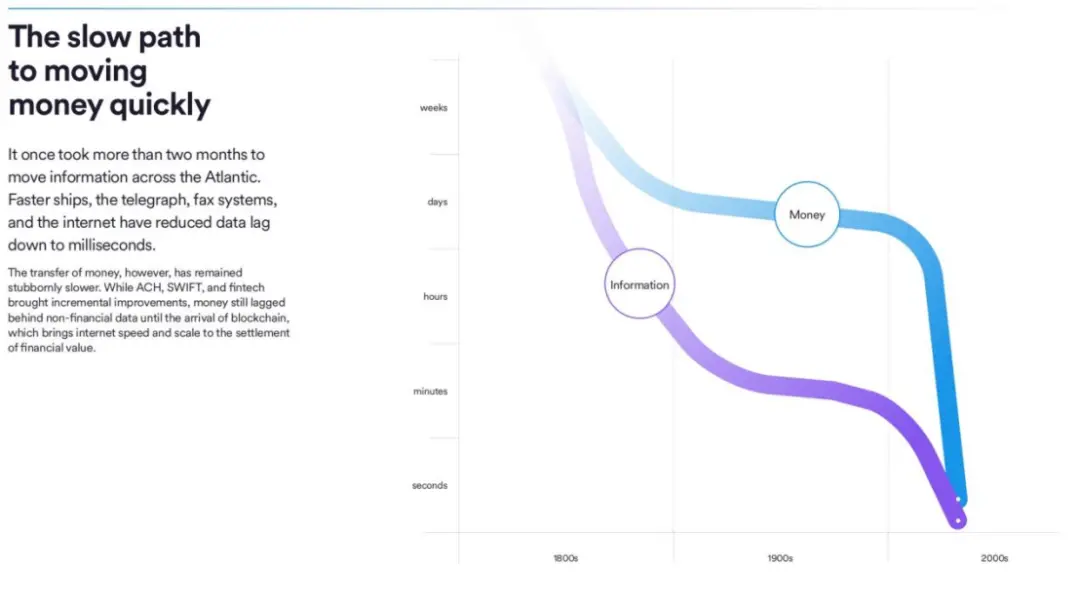

Today’s global economy is more interconnected than ever, yet unlike other economic sectors, the infrastructure supporting capital flows still largely relies on pre-internet frameworks.

In the past, it was impossible to have a “money protocol” capable of transferring value in fully native digital form over the internet.

The U.S. Automated Clearing House (ACH) and similar protocols have now become core components of a fragmented global payment landscape, emerging globally in the early 1970s. Despite recent developments—such as the Single Euro Payments Area (SEPA) in the eurozone, Brazil’s PIX, and India’s Unified Payments Interface (UPI)—these national real-time payment systems have improved domestic transaction speeds, but they still lack a global interoperability standard and global scale, and do not leverage the openness and scalability of programmable money built on open blockchain networks.

Global businesses and individuals are paying a high price for relying on this traditional payment infrastructure. According to the McKinsey report (Global Payments in 2024), the global payment industry generates revenue exceeding $2.4 trillion annually. Most of this "revenue" comes in the form of fees charged to senders and recipients—reflecting the operational complexity and intermediation of traditional infrastructure, which effectively acts as a tax on global commerce and households.

Currently, international wire transfer fees can reach up to $50 per transaction, and intermediaries along the path often impose additional charges. According to World Bank data, the average cost of sending $200 globally in Q2 2024 was 6.65%. Moreover, foreign exchange conversion further exacerbates these challenges, introducing costly forex fees and price volatility.

Fragmented settlement processes within correspondent banking systems continue to impose significant economic costs on businesses and society. For importers and procurement managers, payments must wait several days to settle, weakening cash flow and increasing the complexity of liquidity planning. For exporters and sellers, unpredictable multi-day settlement windows mean they must rely more on expensive short-term working capital loans to sustain operations. Recipients depending on cross-border remittances for food, housing, and other basic living needs may face erosion of vital income due to intervention by traditional intermediaries, endure payment delays, and in some cases, confront inherent risks associated with handling cash in crime-prone environments.

(Digital Dollar on the Value Internet — 2025 USDC Market Economy Report)

2.2 Change Is Here

Change should have arrived long ago. Although the internet has almost completely transformed every aspect of global business over the past few decades, the way capital moves still relies on fragmented, opaque, inefficient, and innovation-limited traditional networks. While some countries have successfully implemented national real-time payment systems, these solutions cannot scale globally and offer limited access for developers.

Since the emergence of early payment information and settlement systems like ACH half a century ago, global communication technology has evolved to instantly connect people across the world. Today, billions can watch movies on their phones while riding the subway, access humanity’s entire knowledge base nearly free of charge, and buy virtually any product from anywhere on Earth.

It is time to adopt a new global capital movement paradigm—one that operates 24/7, seamlessly connects users, eliminates inefficiencies of traditional payment systems, and leverages the solid foundation of traditional finance.

(Digital Dollar on the Value Internet — 2025 USDC Market Economy Report)

2.3 Internet-Native Settlement Layer — Circle Payments Network

With the launch of Circle Payments Network (CPN), this vision is becoming reality.Circle Payments Network (CPN) is a new protocol layer built upon a comprehensive, open, and internet-native settlement system, with USDC, EURC, and future regulated payment stablecoins at its core. By connecting a globally scaled open platform and reducing intermediaries, CPN enables capital flows in ways traditional closed networks cannot.

Crucially, CPN does not directly transfer funds; instead, it functions as a marketplace for financial institutions and serves as a coordination protocol to enable seamless exchange of global capital flows and information.

CPN marks the first integration of regulated settlement assets (in the form of stablecoins) with a dedicated coordination and governance layer designed specifically for financial institutions. This integration links traditional payment systems with assets like USDC and EURC, while establishing a trusted counterparty framework to enable more efficient, intermediary-light global settlements.

By introducing a compliant, 24/7 digital dollar-based “clearing layer,” CPN lays the foundation for internet-scale cross-border settlements.

(https://x.com/circle/status/1914411337683480654)

2.4 Benefits of Circle Payments Network

A. Internet-Based Financial Payment Services

CPN will benefit hundreds of millions of individuals and millions of businesses, enabling them to access capital and other financial services just like other transformative global internet services. Payors can initiate payments using either fiat or stablecoins, while payees (whether corporate or individual) can choose to retain stablecoins upon receipt or convert them into local currency. CPN will make near-instant, borderless payments a common reality.

The launch of CPN enables us to envision a future where international suppliers can receive cross-border payments almost instantly and at low cost through a modern, compliance-first platform supporting global supply chains; small merchants can achieve near-real-time collections without profit erosion from high fees; global sellers can directly enter new markets; content creators can receive micro-payments from consumers efficiently via stablecoins; and remittance recipients can receive a larger proportion of funds, thereby enhancing purchasing power where it matters most.

B. Reducing Technical Complexity

Beyond serving as an upgrade to many current inter-institutional payment networks—often burdened by traditional infrastructure, closed ecosystems, and slow or expensive settlements—CPN is also designed as a modern payment orchestration layer based on stablecoins and blockchain, enabling scalable expansion.

Although blockchain-based payments have gained traction, they are not inherently frictionless or trustworthy—especially in institutional environments, where settlement guarantees, reversibility, compliance, standardized protocols, and robust security are fundamental requirements. CPN further reduces technical complexity and minimizes operational and financial challenges that have hindered stablecoin adoption in mainstream payments and commerce, paving the way for a more efficient, inclusive, innovative, and transparent financial ecosystem.

C. Cost Reduction and Efficiency Gains

From a cost and efficiency standpoint, CPN is a powerful alternative to traditional cross-border payments. While there are costs associated with purchasing stablecoins and converting them back to fiat, in many markets outside the U.S., these “onboarding and offboarding” currency conversion costs are declining and may be lower than acquiring USD through banks.

Traditional USD transfers can be both expensive and slow for both senders and receivers, making both parties more reliant on short-term working capital financing (as previously noted). By enabling near-instant settlement and reducing dependency on intermediaries, CPN can unlock significant cost efficiencies.

Additionally, as an open platform, CPN has the potential to foster a competitive market for onboarding/offboarding currency conversions, foreign exchange, and other services, further lowering costs and improving access conditions.

D. Transparent, Secure, and Scalable

CPN is a transparent, secure, and scalable infrastructure designed to help financial institutions better serve their corporate and individual clients. Crucially, CPN can unlock these efficiencies without compromising compliance. Circle has established a strict governance framework requiring participating financial institutions to meet global anti-money laundering and anti-terrorism financing (AML/CFT) standards and economic sanctions requirements.

E. Open Infrastructure Fuels Innovation

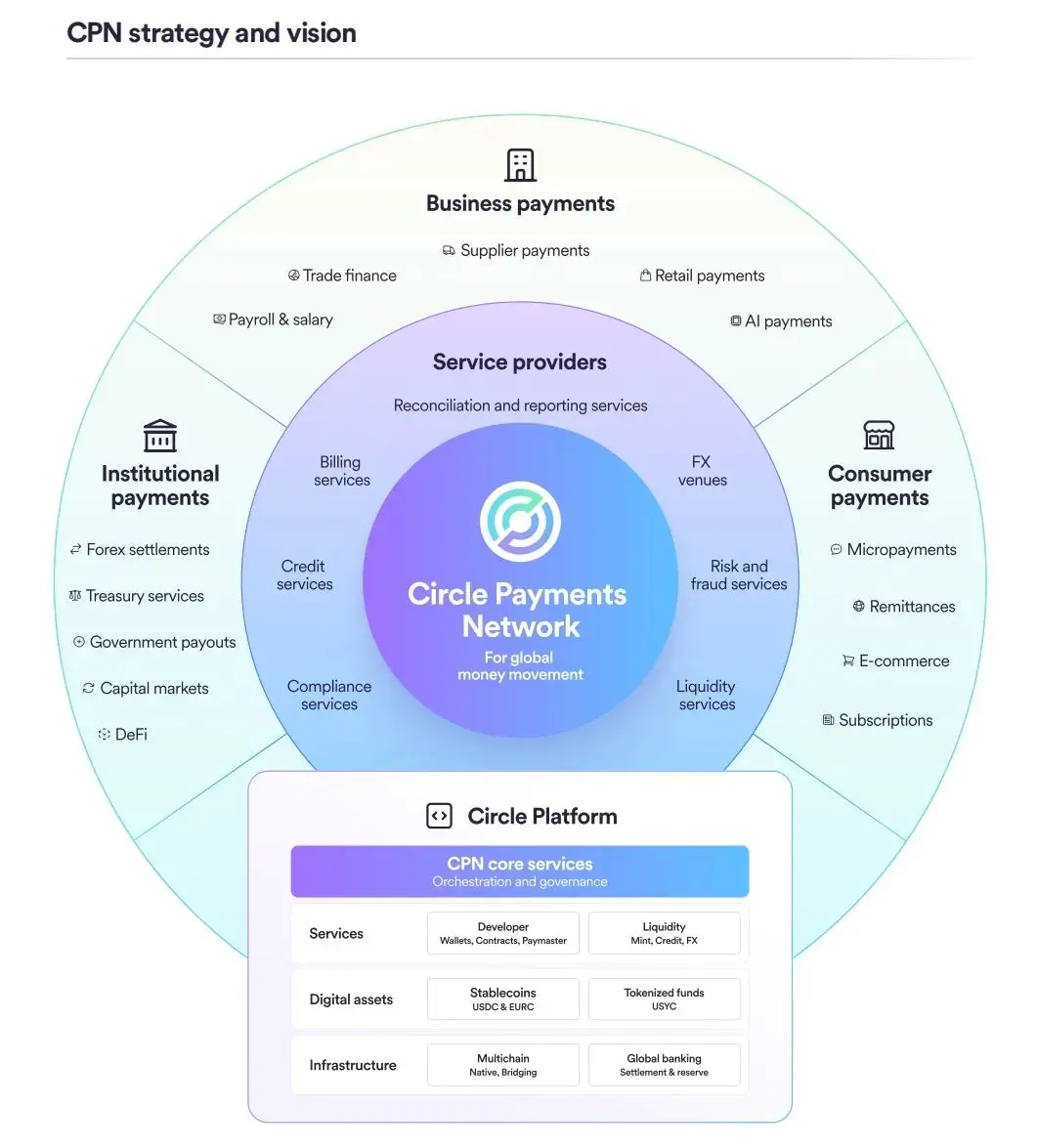

Crucially, CPN does not directly transfer funds; instead, it functions as a marketplace for financial institutions and acts as a coordination protocol to orchestrate global capital flows and seamless information exchange. As the network operator, Circle defines the CPN protocol and provides APIs, developer SDKs, and public smart contracts to coordinate global capital movements.

The growth and success of CPN extend beyond Circle’s ecosystem and depend on participants outside Circle to collectively unlock economic value. The network will provide fertile ground for banks, payment companies, currency conversion providers, app developers, and other regulated stablecoin issuers to co-innovate, delivering greater value and better experiences to their own customers.

It is precisely on this open public blockchain infrastructure that CPN and regulated payment stablecoins provide builders with a powerful foundation to launch on-chain applications that seamlessly transfer funds across these networks.

CPN provides innovators and builders with modular components to develop new user experiences and support diverse payment use cases. Over time, builders will create a vibrant ecosystem of modules and application services on top of CPN—a third-party feature marketplace for CPN participants and end-users to benefit from, and a brand-new, powerful distribution platform unlocked for fintech developers.

III. Circle’s Vision

Through Circle Payments Network (CPN), Circle is building a new platform and network ecosystem that creates value for every stakeholder in the global economy, accelerating the societal benefits brought by this new internet-based financial system:

Enterprises:

Importers, exporters, merchants, and large enterprises: Can leverage financial institutions supported by CPN to eliminate significant costs and friction, strengthen global supply chains, optimize capital management operations, and reduce dependence on expensive short-term working capital financing.

Individuals:

Remittance senders and recipients, content creators, and other individuals who frequently send or receive small payments: Will gain greater value, as financial institutions using CPN can provide these improved services faster, cheaper, and simpler.

Ecological Builders:

Banks, payment companies, and other providers: Can leverage CPN’s platform services to develop innovative payment use cases, harness the programmability of stablecoins, SDKs, and smart contracts to build a thriving ecosystem. Over time, this will fully unlock the potential of stablecoin payments for both businesses and individuals. Additionally, third-party developers and enterprises can introduce value-added services, further expanding the network’s capabilities.

All participants and end-users of the CPN network will benefit from an open, continuously upgradable capital flow infrastructure—lowering cross-border payment costs, increasing speed, and ensuring the technological readiness of the internet-based financial system.

(www.circle.com/cpn)

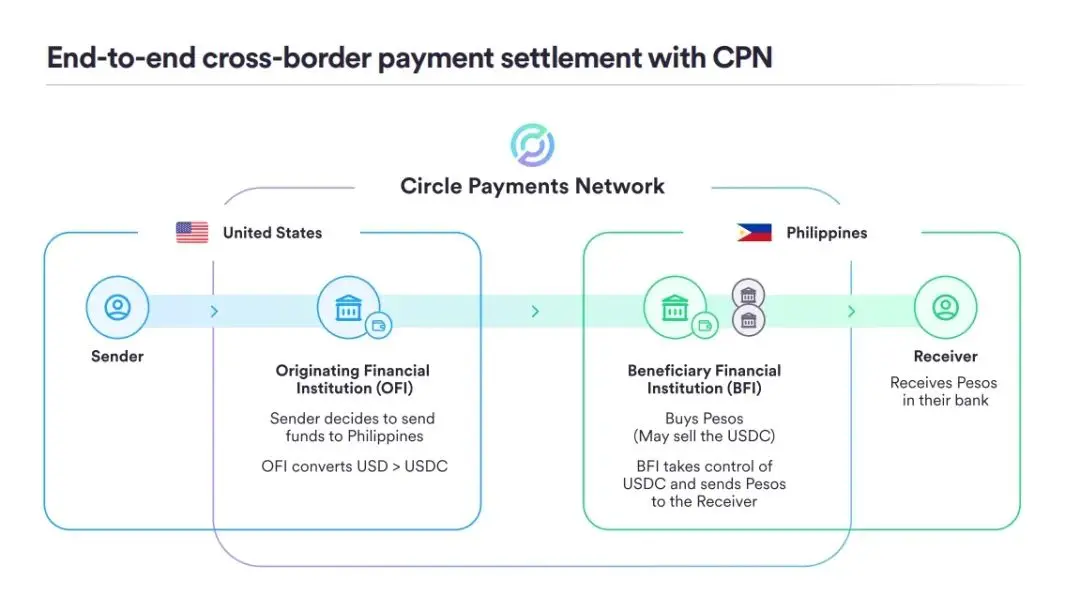

IV. Use Cases

Circle Payments Network (CPN) aims to support a wide range of payment and value transfer use cases by enabling seamless, efficient, and secure transactions using regulated stablecoins on supported blockchain networks.

Its compliance-oriented architecture allows Originating Financial Institutions (OFIs) to discover and connect with Beneficiary Financial Institutions (BFIs) via CPN, while empowering ecosystem builders to develop innovative solutions for individuals, businesses, and institutions.

(www.circle.com/cpn)

4.1 Business Payments (Business Payments)

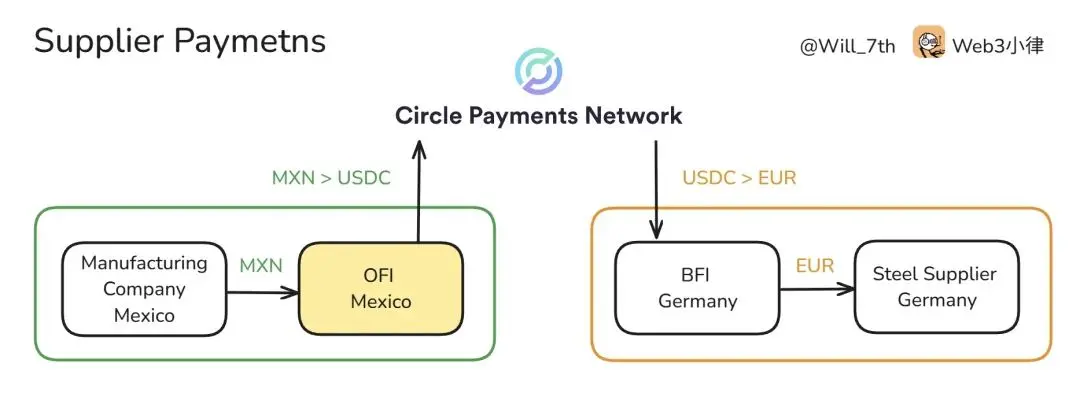

A. Supplier Payments (Supplier Payments)

Accelerate and simplify cross-border payments between companies by shortening settlement times and eliminating intermediaries.

A manufacturing company in Mexico needs to pay a steel supplier in Germany but wants to avoid high foreign exchange fees and multi-day bank transfers. The company’s originating financial institution (OFI) converts Mexican pesos (MXN) into USDC, connects via CPN to the beneficiary financial institution (BFI) in Germany, and sends the USDC. The BFI then seamlessly converts the USDC into euros and settles the payment into the supplier’s account instantly.

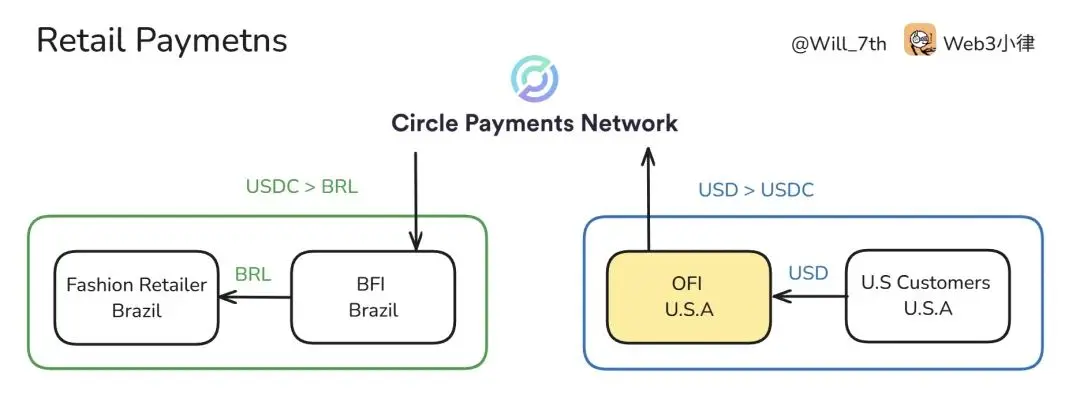

B. Retail Payments (Retail Payments)

Enhance global e-commerce with secure, efficient, and flexible payment options.

A Brazilian fashion retailer sells goods to a U.S. customer. The retailer’s BFI connects via CPN to an OFI to receive a dollar payment. The OFI converts the USD into USDC and sends it to the BFI, which then seamlessly converts the USDC into Brazilian reais (BRL), or holds it as USDC in a digital asset custodian on behalf of the retailer. The retailer receives funds instantly, with faster settlement than traditional payment processors, and can choose to keep working capital in digital dollars.

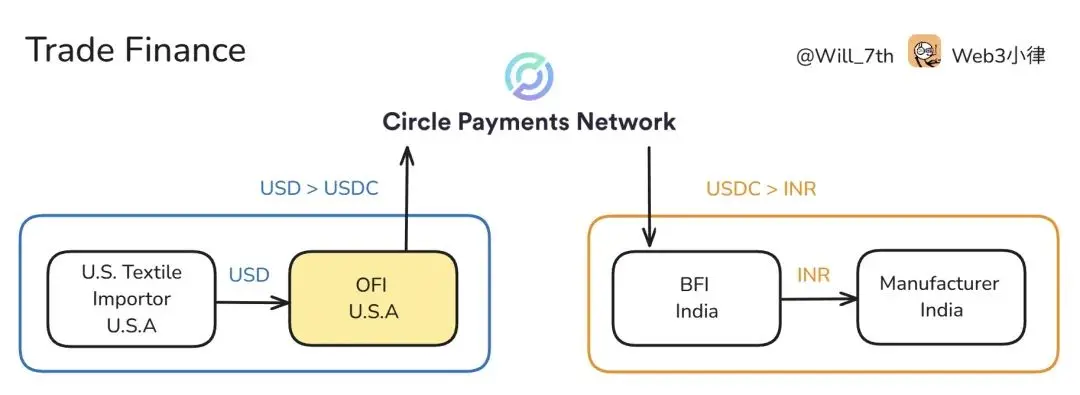

C. Trade Finance (Trade Finance)

Simplify and secure international trade payments.

A U.S. textile importer places an order with an Indian manufacturer, aiming to reduce the time and cost of traditional trade financing. The importer’s OFI converts U.S. dollars (USD) into USDC and connects via CPN with an Indian BFI to transfer funds. The BFI manages the USDC custody via smart contract and disburses Indian rupees (INR) to the manufacturer after verifying shipping documents. This method enables faster settlement, reduces counterparty risk, and innovatively leverages smart contracts for custody services.

D. Payroll and Salary Disbursements (Payroll and Salary Disbursements)

Enable companies to process global payroll payments at minimal cost and with instant settlement.

A multinational corporation pays remote employees across multiple countries. Instead of relying on traditional banking channels, the company uses its OFI to convert local currency into USDC and immediately distributes salaries to employees via multiple BFIs discovered through CPN. These BFIs receive USDC from the OFI and complete final payments in each employee’s local currency.

E. AI Payments (AI Payments)

In the future, CPN will support autonomous AI agents representing users or systems to send and receive payments, enabling real-time value exchange.

A logistics company uses an AI agent to book cross-border freight services. When the agent selects a service provider in Singapore, it uses an OFI integrated with CPN to convert U.S. dollars (USD) into USDC and automatically sends the payment to the Singaporean BFI, which then converts it into Singapore dollars (SGD). The entire payment process is executed programmatically via smart contracts, minimizing manual steps and enabling intelligent, cross-border machine-to-machine payments.

4.2 Consumer Payments (Consumer Payments)

A. Remittances (Remittances)

Empower individuals with fast and cost-effective remittance services, avoiding high fees and delays.

A user residing in the U.S. wishes to send money to family in the Philippines. As a remittance company acting as the U.S.-based originating financial institution (OFI), it converts U.S. dollars (USD) into USDC and simultaneously routes the USDC through a dynamically discovered Philippine beneficiary financial institution (BFI) via CPN, converting it into Philippine pesos (PHP), delivering funds to the family nearly in real time, at a fraction of traditional remittance fees.

B. Subscription Services (Subscriptions)

Support recurring payments for digital services via programmable stablecoin billing.

A digital media platform offers premium subscription services to global users. Each month, users' digital wallets initiate a USDC payment via their originating financial institution (OFI), which is routed through a platform beneficiary financial institution (BFI) discovered via CPN. The BFI receives the funds, holds them as USDC in a digital asset custodian on behalf of the media platform, or converts them into local fiat currency as needed and credits them to the media platform's account.

C. Micropayments and Content Monetization

Enables instant, low-cost micropayments for content creators and digital service providers.

A Brazilian content creator receives micro-donations from global fans via CPN, using a local Originating Financial Institution (OFI) and a Beneficiary Financial Institution (BFI) supporting CPN. Fans avoid long delays and high platform fees, instead sending stablecoins instantly—achieving fast and low-cost monetization.

D. E-commerce

Expands consumer access to global online markets through rapid payment experiences.

A UK customer purchases electronics from a Korean seller via an international e-commerce platform. At checkout, the customer pays in GBP through their local OFI, which converts funds into USDC and transfers them to the Korean BFI. The BFI converts USDC into KRW and deposits it into the seller’s account.

4.3 Institutional Payments

A. Capital Markets Settlement

Enhances transaction efficiency by enabling faster, more transparent settlement between financial institutions, reducing counterparty risk and operational costs.

An American asset management firm executes an over-the-counter (OTC) bond trade with a European investment bank but seeks to avoid T+2 settlement delays and the resulting capital inefficiency and counterparty risk. The asset manager’s OFI converts USD into USDC and connects via CPN to the European BFI, which settles the transaction in EUR instantly.

B. Foreign Exchange (FX)

Improves multi-currency operations by simplifying currency conversion, addressing high foreign exchange rates and complexity/latency issues associated with traditional providers.

A European investment firm wishes to fund a real estate acquisition in Japan but aims to avoid high FX fees and delays. The firm’s OFI converts EUR into EURC, and the Japanese BFI seamlessly exchanges it on-chain at competitive FX rates and settles instantly.

C. Treasury Services

Simplifies repatriation of overseas revenue back to the home market through efficient conversion.

A U.S.-based enterprise software provider delivers cloud-based solutions to numerous clients across Southeast Asia. To repatriate regional revenues to the U.S., the company’s BFI in the U.S. discovers a local OFI in the Philippines via CPN. The OFI collects PHP payments from corporate clients, converts them into USDC, and transmits them to the U.S. BFI. Subsequently, the BFI converts USDC into USD and deposits it into the company’s treasury account, enabling faster and compliant global revenue consolidation.

D. Government and Humanitarian Payments

Provides secure, reliable, and efficient channels for large-scale disbursements—from disaster relief funds to institutional transfers.

An international non-governmental organization (NGO) uses stablecoins to distribute disaster relief funds. The NGO initiates the payment through its OFI, which converts local fiat into USDC and transfers it to the BFI operating in the recipient region. The BFI then either delivers funds directly to beneficiaries’ digital wallets or converts USDC into local fiat and deposits it into their bank accounts, ensuring transparency, accelerating disbursement, and enhancing accountability in aid delivery.

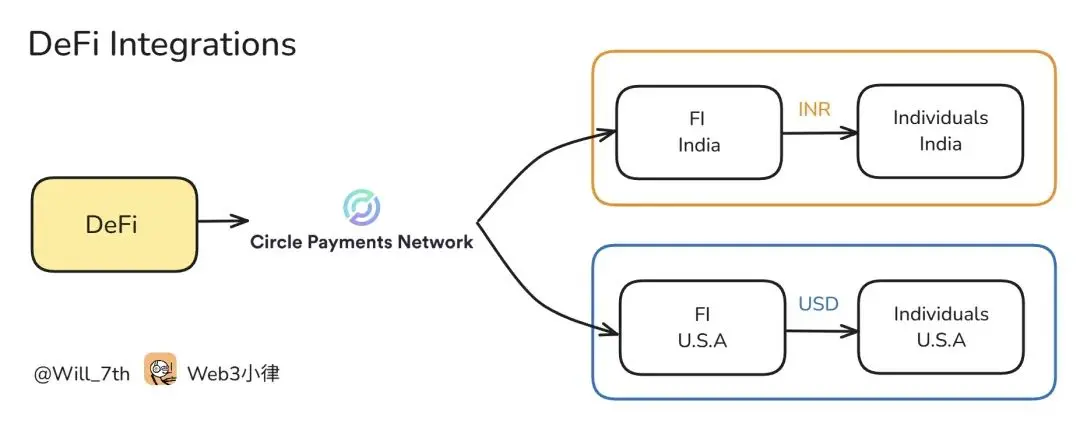

E. DeFi Integrations

Supports DeFi innovators by providing foundational infrastructure for lending, borrowing, saving, and unlocking the potential of mainstream on-chain finance at scale.

A licensed and regulated DeFi lending platform integrates USDC and EURC to offer loan and savings products. Leveraging CPN’s infrastructure, the platform facilitates seamless cross-border transactions, reduces volatility, supports compliant institutional client flows, and builds trust across diverse user groups.

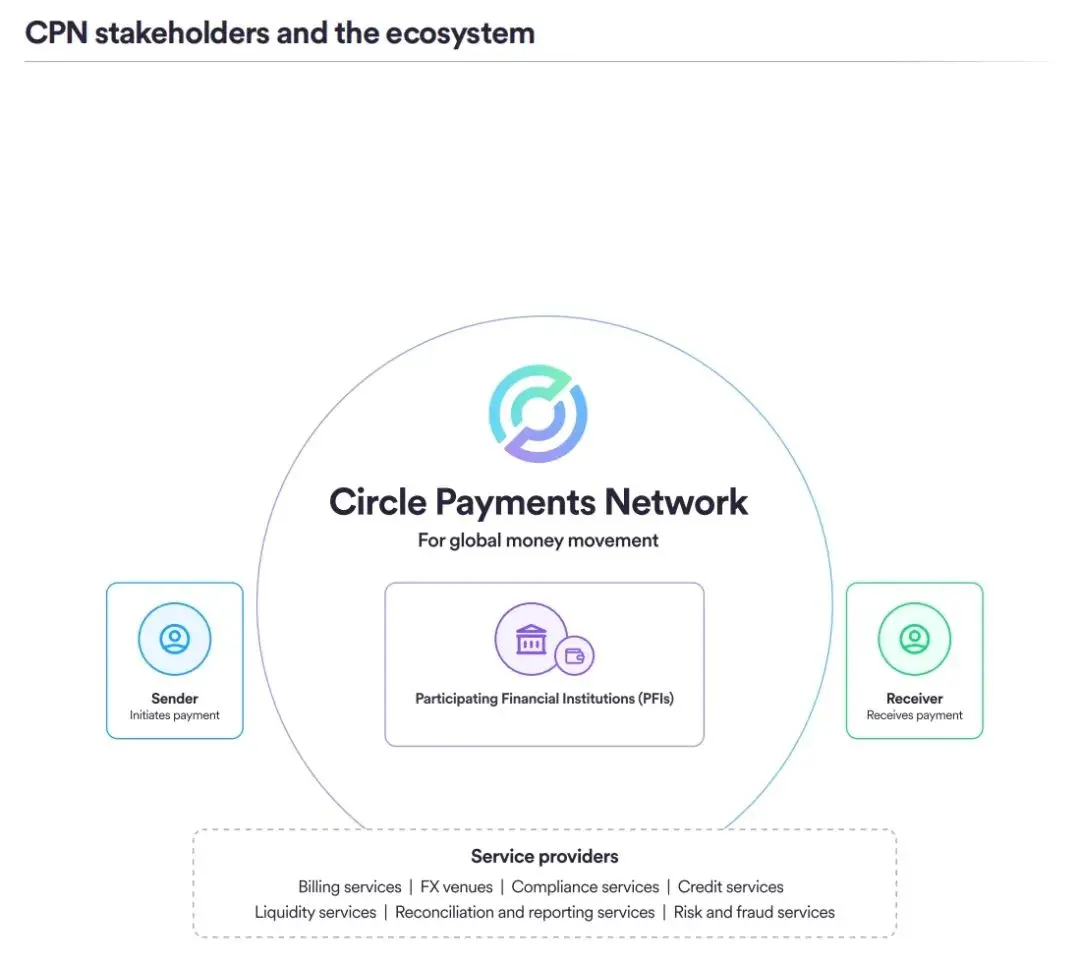

V. CPN Ecosystem Stakeholders and Roles

The CPN ecosystem comprises stakeholders and participants who play pivotal roles in advancing global payments, driving technological innovation, and fostering network governance, economic value creation, and network adoption.

5.1 CPN Governance Bodies

Circle serves as the primary governance and standard-setting body for CPN, as well as the network operator.

Circle’s core responsibilities include:

-

Establishing and maintaining the Circle Payments Network Rules (“CPN Rules”), which govern the eligibility, operations, and compliance of all participants.

-

Developing and maintaining core infrastructure—smart contracts, APIs, and SDKs—to enable seamless cross-blockchain payment settlement (send/receive transactions).

-

Operating the coordination protocol used for member onboarding, price discovery, payment routing, and settlement among counterparties.

-

Facilitating standardized and automated information sharing among members to ensure compliance with the Travel Rule.

-

Validating institutional eligibility, approving network participation, and issuing credentials certifying compliance with CPN standards related to licensing, anti-money laundering and counter-terrorism financing (AML/CFT), sanctions compliance, and financial strength.

-

Monitoring member compliance with regulatory requirements—including AML/CFT and sanctions—through continuous risk-based reviews.

-

Planning and managing cybersecurity, incident response, and infrastructure to ensure operational integrity and resilience.

-

Introducing pre-vetted third-party service providers and modular applications that meet CPN’s compliance, security, and performance standards.

5.2 CPN Members

Members, also known as Participating Financial Institutions (PFIs), are the backbone of CPN. They act as counterparties, initiating, facilitating, or receiving payments within the network and executing transactions in accordance with CPN rules and governance standards.

PFIs include Virtual Asset Service Providers (VASPs), traditional and crypto-native payment service providers (PSPs), and financial institutions such as traditional or digital banks. Depending on their role in a transaction, PFIs may act as Originating Financial Institutions (OFIs), initiating payments on behalf of senders; or as Beneficiary Financial Institutions (BFIs), receiving stablecoin payments and facilitating last-mile fiat disbursement via local payment systems, or providing stablecoin custody services on behalf of recipients.

Core responsibilities of CPN members include:

-

Maintaining appropriate licenses and ensuring ongoing compliance with applicable regulations in all relevant jurisdictions, including anti-money laundering and counter-terrorism financing (AML/CFT) and sanctions requirements, while adhering to CPN Rules.

-

Participating in Circle’s qualification process and maintaining up-to-date verification of legal entity information, compliance status, jurisdictional scope, and risk profile.

-

Conducting risk-based assessments of counterparties and transactions based on compliance obligations, leveraging information collected via CPN and supervision performed.

-

Executing payments according to a series of technical services and protocols detailed in the CPN Rules, based on their role as OFI or BFI.

-

Complying with CPN’s technical and infrastructure requirements, including secure integration, service level agreement (SLA) performance, transaction monitoring, and data protection protocols.

-

Sharing necessary sender and beneficiary information in accordance with CPN’s Travel Rule compliance framework, request for information (RFIs), and other supervisory requests.

-

Monitoring transactions to detect and report suspicious activity in accordance with applicable regulations.

-

Participating in CPN governance through structured feedback, operational reviews, and member reputation scoring to enhance transparency and support continuous improvement.

-

Providing timely support and solutions to other members or end users regarding network inquiries.

-

Leveraging CPN’s developer SDK, regulated stablecoins, and smart contract infrastructure to develop and deliver innovative payment use cases.

5.3 CPN End Users (Businesses and Individuals)

End users are the ultimate initiators and beneficiaries of payment transactions—though they do not interact directly with CPN—they benefit from lower costs, faster settlement, higher transparency, and continuous innovation. Senders initiate payments through their OFI, while beneficiaries receive payments via their BFI.

5.4 CPN Service Providers

These entities include financial institutions (FIs) and non-financial institutions (non-FIs) that provide value-added technical solutions and financial services to CPN members and end users.

They include:

-

Liquidity Providers and FX Venues: These entities provide efficient market-making, price discovery, and currency conversion services for stablecoin transactions within CPN. They supply liquidity for cross-border stablecoin settlements and ensure competitive foreign exchange rates.

-

Stablecoin Issuers: These institutions issue regulated payment stablecoins, which serve as the primary medium of exchange within CPN. Stablecoin issuers ensure transparent reserves, regulatory compliance, and underlying fiat liquidity to support seamless cross-border transactions.

-

Technology Solutions and Financial Services Providers: These providers offer a range of services to CPN members, including fraud and risk management, wallet infrastructure, custody solutions, billing and invoicing, and compliance and transaction monitoring solutions to support their business and operational needs.

(www.circle.com/cpn)

VI. CPN Governance, Qualification, and Network Operations

CPN operates under a collaborative and transparent governance framework designed to prioritize compliance, security, and trust within the network. This framework encompasses three key aspects of governance:

-

Qualification and Oversight: Circle, as the primary governance body, establishes rigorous qualification standards documented in the Circle Payments Network Rules and drives the integration of regulated payment stablecoins into the network.

-

Network Functionality and Operations: Core functionalities support seamless and compliant transactions while ensuring operational rigor and continuous improvement.

-

Transparency and Stakeholder Engagement: By actively engaging with diverse stakeholders—including financial institutions, regulators, enterprises, and builders—CPN aligns with global standards to build trust, accelerate adoption, and foster sustainable ecosystem growth.

Network Operations:

-

Restricted to legally authorized financial institutions;

-

Mandatory AML/CFT and sanctions compliance;

-

Secure transaction data sharing, including Travel Rule;

-

Continuous auditing and oversight.

6.1 Qualification and Oversight

The CPN governance framework defines qualification criteria, certification protocols, and integration procedures for regulated stablecoins to ensure trustworthy participation by financial institutions, regulated stablecoin issuers, and service providers within the network.

A. Strict Qualification Standards

Members must meet comprehensive qualification requirements before gaining network access. This includes holding all necessary licenses, implementing sanctions and AML programs aligned with local regulations and global standards, maintaining reasonable security controls, and demonstrating sufficient financial strength. As the network operator, Circle evaluates all prospective members prior to granting access and reassesses them periodically based on risk. Members licensed under robust regulatory frameworks established by international compliance standards bodies (such as the Financial Action Task Force (FATF)) undergo standard review, while others face deeper assessment. Qualification standards are published, and Circle’s evaluation can serve as input for members’ own counterparty due diligence processes.

B. Member Certification and Access

Upon successful completion of qualification verification and approval, CPN issues unique network certifications to qualified members. These certifications enable counterparties to securely identify one another and retrieve counterparty information, promoting transparency, enabling informed risk assessment, and improving the efficiency of counterparty due diligence. The certification contains a defined set of attributes—including membership status, jurisdictional scope, and qualification details—that are continuously monitored and updated to reflect changes in the risk landscape.

C. Integration of Regulated Payment Stablecoins

The CPN governance framework outlines a structured assessment and approval process for integrating new regulated payment stablecoins into CPN. Potential stablecoins must undergo rigorous evaluation against CPN’s strict qualification standards, including regulatory compliance, transparent reserve and audit proof, availability of banking payment channels, underlying fiat liquidity, risk management standards, information and cybersecurity capabilities, and reporting practices. Only stablecoins fully meeting these standards and approved by the governance body may operate within the network, ensuring they contribute to a stable, secure, and efficient network ecosystem.

6.2 Network Functionality and Operations

CPN enables secure, real-time transactions for members through a robust operational framework that ensures consistency, scalability, and resilience. The framework includes transaction coordination, operational support, incident response, and infrastructure management.

A. Transaction Coordination and Risk Management

Transactions within CPN are coordinated through a suite of technical services and protocols, ensuring seamless execution among participating members. Additionally, network members leverage CPN-provided automated alerts and regular risk assessments to continuously monitor transaction flows, focusing on anomalies and partner performance—such as evaluating failed transaction rates and SLA violations. These measures collectively proactively mitigate operational risks, helping maintain network reliability and efficiency.

B. Member Operational Support

CPN provides clear operational guidelines, including service level agreements (SLAs) defined in the CPN Rules, covering expectations for uptime, transaction speed, dispute resolution, and timely information sharing. The network also standardizes the exchange of transactions and counterparty data, simplifying operations by reducing the need for custom coordination.

C. Incident and Crisis Management

CPN has established detailed protocols for managing security incidents, regulatory compliance issues, and system outages. These protocols include pre-defined communication channels with members and transparent, fair resolution processes to ensure swift action and effective dispute management, regardless of whether the issue involves compliance or transactions.

D. Infrastructure Scalability and Planning

CPN infrastructure is continuously monitored using observability tools that track throughput, latency, and error rates. Automated performance monitoring and regular load testing enable the network to scale according to demand. Circle collaborates with vetted infrastructure and cloud partners to ensure resilient computing and storage resource provisioning. Scalability reviews and corridor-level stress tests validate the network’s readiness for increased transaction volume and network expansion.

6.3 Transparency and Stakeholder Engagement

CPN governance is built on transparency, fostering trust and confidence among all participants. As the governance body, Circle, guided by advisory council recommendations, adopts strategic initiatives to strengthen the governance framework. CPN conducts regular surveys, focus groups, and structured reviews to gather member feedback and assess service quality. These inputs drive continuous improvement and help ensure network development meets participant needs. Independent audits and periodic public reports on transaction volume, system uptime, and member compliance further reinforce operational integrity and accountability.

Representatives of CPN members and end users, along with interactions with regulators, play a crucial role in network evolution. CPN members are encouraged to actively participate in shaping network rules and technical standards by providing insights and operational feedback that inform network strategy and growth. Furthermore, Circle’s financial services division maintains ongoing engagement with global regulators, building a strong track record that can be leveraged to ensure CPN remains aligned with international standards—particularly international AML/CFT and FATF Travel Rule standards—and operates in a safe, trustworthy, and compliant environment.

VII. CPN Core Services

CPN functions as a coordination protocol specifically designed for stablecoins, enabling seamless, compliant, and programmable global transactions.

CPN leverages public blockchain networks for final settlement while optimizing payment coordination, compliance-related data exchange, and intelligent routing between payment stablecoins and network members. Stablecoins are the foundational digital asset class within CPN, providing the stability, interoperability, and programmability required for high-trust financial applications.

At launch, the network supports USDC and EURC and plans to expand to other regulated payment stablecoins meeting CPN’s stringent governance and qualification standards. Over time, CPN will become a foundation for builders to develop interoperable modules and application services, extending the network’s utility and unlocking new use cases for global payments and financial innovation.

7.1 Payment via Intelligent Coordination

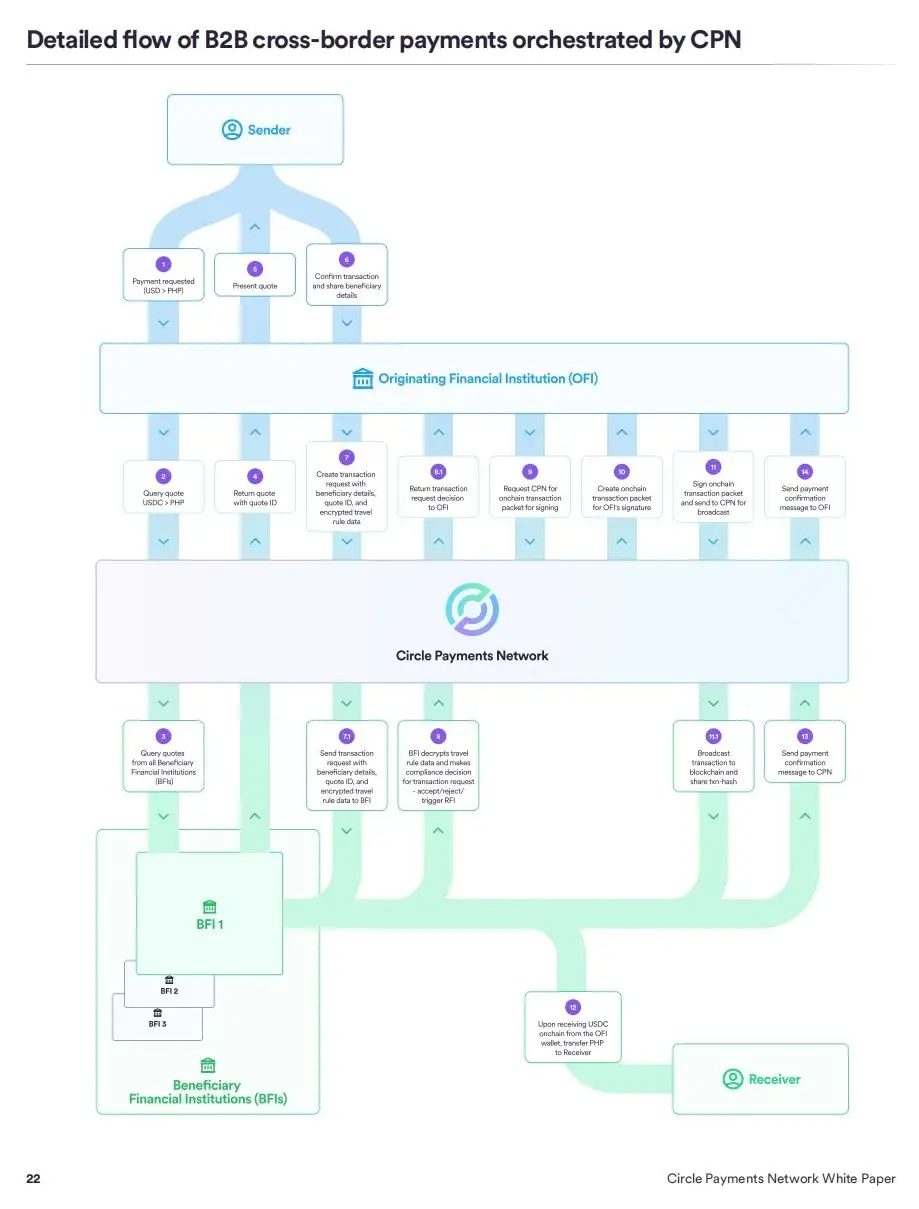

CPN’s payment protocol is built on a hybrid architecture combining off-chain and on-chain systems, helping aggregate liquidity and facilitate price discovery among network members. As more payment stablecoins join the network, CPN will evolve into a on-chain foreign exchange (FX) routing infrastructure, enabling efficient and instant stablecoin-to-stablecoin exchange while still coordinating settlement between Originating Financial Institutions (OFIs) and Beneficiary Financial Institutions (BFIs).

In CPN’s initial version, coordination occurs via an off-chain API system generating transaction requests. OFIs sign these requests to initiate transfers of USDC or EURC to designated BFI wallets. At this stage, Circle (as network operator and governance body) broadcasts the transaction to the appropriate blockchain. This process validates payment details, ensures the correct amount and token are delivered to the BFI, and confirms that all relevant fees are covered within the agreed settlement window.

Subsequently, CPN will transition to a smart contract protocol architecture, enhancing network composability and introducing more efficient, value-added features. The CPN smart contract payment protocol is designed for seamless on-chain payments between members using stablecoins—including USDC and EURC. By leveraging smart contracts, the protocol achieves minimal error risk, automated reconciliation, and efficient fee collection while maintaining a non-custodial design.

Under this protocol, the OFI initiates the payment by deploying a smart contract on the public blockchain network supported by CPN. The contract verifies critical transaction parameters (such as token type, amount, recipient address, and deadline) before executing the payment. Unlike traditional transfers prone to errors and requiring separate invoice generation for fees, smart contracts enforce precise payments and efficiently route transactions to different BFIs in scenarios involving multiple bids and quotes.

To enhance transparency and security, each transaction is uniquely identified and timestamped, ensuring clear auditability for compliance and reconciliation purposes. Additionally, the protocol will include an optional “revoke” function in the future, allowing senders to cancel erroneous transactions during a brief window before final confirmation.

(www.circle.com/cpn)

7.2 Intelligent Discovery and Routing Optimization for Foreign Exchange (FX)

CPN enables participating Originating Financial Institutions (OFIs) to discover Beneficiary Financial Institutions (BFIs) and send stablecoins for payment settlement. During discovery, CPN allows OFIs to query the network for specific stablecoin or fiat currency pairs. The system enables OFIs to discover network participants and request corresponding exchange rates and liquidity. Initially, the platform integrates USDC and EURC with local fiat liquidity order books and private liquidity sources. Over time, the system will transition to a fully on-chain foreign exchange (FX) routing, aggregation, and settlement architecture—providing direct access to on-chain FX pools, order books, and private liquidity. The network’s discovery capability will include order routing, while the Request-for-Quote (RFQ) system will further optimize FX execution to meet performance standards of traditional payment systems.

While the network initially focuses on discovering liquidity among BFIs, it will gradually extend to include whitelisted on-chain venues—such as automated market makers (AMMs), on-chain order books, and other liquidity providers—to broaden access to stablecoin liquidity. Once discovered, CPN will intelligently match orders from these sources, enabling direct stablecoin FX exchange with built-in security measures and transparent execution, coordinated by Circle as the network operator.

7.3 Cross-Chain Seamless Settlement Payments

CPN supports native settlement of stablecoins across multiple blockchains, offering a seamless cross-chain payment transfer mechanism. Participating Financial Institutions (PFIs) bring their preferred blockchain into the network, while CPN coordinates transactions between selected source and target blockchains for efficient payment settlement. Leveraging Circle’s Cross-Chain Transfer Protocol (CCTP v2), CPN provides fast and secure cross-chain transfers for approved stablecoins, ensuring transaction speed and integrity across blockchain networks. Initially, the platform will support a limited number of blockchains at launch, expanding to additional blockchains based on member preferences over time.

7.4 Privacy Protection via Selective Transparency

CPN introduces advanced privacy-enhancing features on public blockchains to protect transaction data, helping members fulfill privacy and operational obligations. These mechanisms allow users to designate certain transactions as confidential, ensuring sensitive payment information is not permanently exposed on public blockchains. This capability supports a wide range of use cases, enabling enterprises to maintain confidentiality through CPN for critical activities such as corporate payments, trade financing, and payroll distribution.

Additionally, CPN will adopt a confidential protocol (to be defined separately, not included in this whitepaper) to enable selective disclosure. Under this protocol, transaction details will be visible only to authorized parties—including counterparties, law enforcement, regulators, and auditors—when required for compliance or legal purposes.

7.5 Extending Capability via Composability and Trustworthy Interoperability

To extend the ecosystem’s value, CPN allows pre-vetted third-party protocols to integrate with and interoperate with its core infrastructure, enhancing the practicality and versatility of its payment capabilities. Circle envisions a diverse set of integrations—including lending and credit, liquidity aggregation, institutional yield, custody, subscription services, and more. Participation is restricted to protocols on Circle’s whitelist that have undergone auditing and rigorous review, meeting strict regulatory compliance, security, and liquidity management standards. Through this composable architecture, CPN aims to unlock a secure, programmable foundation and a third-party ecosystem for global payments, financial services, and technology-driven solutions.

VIII. CPN Economic Model

CPN’s economic model and incentive mechanisms are designed to drive early rapid adoption while establishing a sustainable long-term revenue strategy for all network participants. It aligns incentives across all network members, end users, builders, and service providers to promote network growth and sustainability.

Transactions processed via CPN generate three primary fees:

-

Payout Fees: Compensate Beneficiary Financial Institutions (BFIs) for local fiat disbursement and processing.

-

FX Spreads: Reflect liquidity risk and currency conversion costs.

-

CPN Network Fee: A tiered variable basis point fee based on country grouping, used to support core network functions, including compliance, security, infrastructure, and development.

As CPN grows and Circle and third-party developers introduce new value-added services through curated markets, additional usage-based fees will be implemented to support and sustain these services. These services may include fraud detection tools, risk management, wallet infrastructure, custody, billing, and advanced compliance capabilities. First-party (1P) and third-party (3P) service fees will create revenue opportunities for providers and enable financial institutions to customize payment experiences through modular, plug-and-play solutions.

A portion of network and market fees will be strategically reinvested into core priorities, such as infrastructure upgrades, research and development, network operations, user acquisition incentives, and developer ecosystem growth—including funding for CPN integrations and new applications. This reinvestment approach aims to enhance platform resilience, drive innovation, and accelerate long-term network expansion.

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

4 days ago

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

4 days agoAmazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

4 days agoBinance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

4 days agoBinance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

4 days ago

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

4 days agoSlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

4 days ago