ChainThink

Stay ahead, master crypto insights

is rated grade, is company still worth exploring and investing in?

is rated grade, is company still worth exploring and investing in?

2025-10-29 09:59

Editor's Note:

In the same week that S&P Global issued its first credit rating for Strategy (formerly MicroStrategy), labeling it as 'B-', discussions around Digital Asset Treasuries (DATs) entered a new phase. The symbolic significance of this rating goes beyond a single company, marking the first time the Bitcoin treasury model has been incorporated into the mainstream credit evaluation framework.

This is both an acknowledgment and a collision. S&P evaluates Strategy through traditional finance logic, considering its structure of "assets are Bitcoin, liabilities are USD" to have fundamental currency mismatch; however, proponents of the crypto world insist that this is the paradigm shift of the new generation of "asset-oriented companies."

The DAT model connects risk, but also the future. It represents a middle ground between crypto and capital markets—neither entirely part of the "coin circle," nor entirely part of the "stock market." Strategy was rated as "junk," but in a way, this was the first time a digital asset treasury received the qualification for rating. In the future, how traditional rating agencies quantify Bitcoin risk, and how investors view the "crypto version of Berkshire Hathaway," will determine whether DAT can transition from speculative narratives to a part of the financial structure.

Below is the original text:

Introduction

Digital Asset Treasuries (DATs) are increasingly becoming a mechanism that attracts Traditional Finance (TradFi) attention to blue-chip crypto assets such as $BTC and $ETH. We are currently experiencing a wave of DAT projects, with the core idea being the accumulation of digital assets as the core assets of a company's treasury.

The DAT model provides investors with a way to gain exposure to crypto assets similar to stocks—investors do not directly purchase cryptocurrencies, but rather purchase the stock of companies that hold crypto assets. This model can also be understood as a "crypto asset wrapper," allowing investors to avoid the complexities of self-custody or face data breaches and social engineering attack risks from exchanges.

The most representative DAT is Strategy (formerly @MicroStrategy), which holds approximately 640,000 BTC, representing 3% of the total Bitcoin supply. As Strategy's success and its stock ($MSTR) price surged, this model became highly attractive to other companies—they could raise funds to purchase crypto assets, thereby changing the asset backing per share, triggering speculative behavior around net asset value multiples (mNAV) and premiums/discounts.

This article aims to deeply analyze the operational mechanisms of DAT, key indicators, current market landscape, participating companies, potential risks, and ultimately assess its long-term sustainability.

What is a DAT? How do they work?

The term DAT emerged with Strategy's transformation. Strategy was originally a software company providing business analytics services, and in August 2020, it transformed into a DAT, after which its stock price increased by over 2000%. While part of this was due to its status as the first publicly listed company to significantly purchase Bitcoin, it also validated the feasibility of the DAT model as a business opportunity.

The core of DAT is as an "asset accumulation tool for equity financing," raising funds through stock issuance, purchasing crypto assets, thereby increasing the crypto asset exposure on the company's balance sheet. Its valuation and operating metrics (such as NAV, mNAV, premium/discount) are highly dependent on the price fluctuations of the assets it holds.

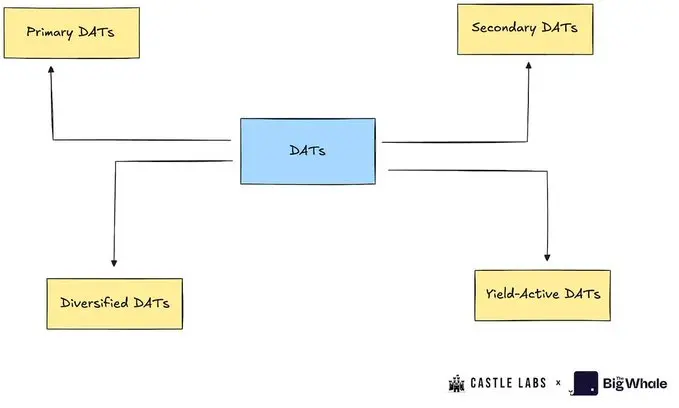

Digital Treasury Companies can be divided into the following categories:

1. Primary DATs: These are the most typical digital treasury companies, accumulating specific assets (such as BTC or ETH) through equity financing. Representative companies include Strategy and BitMine.

2. Secondary DATs: These companies do not fully adopt the digital treasury company model, but instead support their stock prices through other businesses, using digital assets to achieve diversified exposure. These companies generate income through their main operations and use part of the income to accumulate crypto assets. Representative companies include Tesla, Galaxy, and MARA.

3. Yield-Active DATs: These companies aim to generate income from their crypto assets. For example, Sharplink stakes most of its ETH and earns staking rewards.

4. Diversified DATs: These companies are still accumulating crypto assets, but are not focused on a single asset, but hold multiple assets. Representative companies include Nepute Digital Assets Corp (holding BTC, ETH, SOL) and BTCS Inc (holding ETH, ADA, SOL).

Although this report will not strictly distinguish between these different types of digital treasury companies, it will select several as case studies for in-depth analysis.

Key Terminology of DATs

To better understand the operation mechanism of DATs, this section introduces a series of key terms, which are important indicators for assessing the health of a DAT.

Net Asset Value (NAV): Refers to the net value of the DAT's treasury, calculated as the number of assets in the treasury multiplied by their dollar price. For example, a DAT holding 10,000 BTC (each BTC priced at $114,000) would have a NAV of $1.14 billion.

Net Asset Value per Share (NAVps): NAV divided by the total number of diluted shares outstanding. This indicator reflects the value each share should have. If the market price is higher than NAVps, the company's stock is trading at a premium; otherwise, it is trading at a discount.

Crypto Per Share (CPS): The amount of crypto assets represented by each share. It measures the quantity of BTC, ETH, or other assets per share.

Market Value to Net Asset Value Ratio (mNAV): The ratio of the company's market value to its NAV. If mNAV is greater than 1.0, it means the stock is trading at a premium over the treasury value (investors pay a premium to gain crypto exposure, leverage, or options); if mNAV is less than 1.0, it indicates skepticism in the market, governance risks, or lack of information disclosure, leading to a discount.

Accretion/Dilution Test: Only when the number of crypto assets purchased by newly issued shares is higher than the current CPS, the issuance is beneficial to investors (accretion). The formula is as follows: ΔUΔS>US\frac{ΔU}{ΔS} > \frac{U}{S}ΔSΔU>SU

Where:

ΔU: The number of crypto assets newly purchased

ΔS: The number of newly issued shares

U: The current number of crypto assets held

S: The current number of shares outstanding

For example: A company plans to raise $1 billion, currently trading at a 40% premium (mNAV=1.4), the treasury holds 200,000 BTC (NAV=$22 billion), there are 20 million shares outstanding, the total market cap is $30.8 billion. The share price is $1540, so the company needs to issue about 650,000 shares to complete the fundraising.

After fundraising, the company purchases 9000 BTC at a price of $110,000 per BTC, the total holdings in the treasury become 209,000 BTC. The original CPS is 200,000 / 20,000,000 = 0.01, the new CPS is 209,000 / 20,650,000 ≈ 0.0101, indicating that this fundraising is slightly accretive to investors.

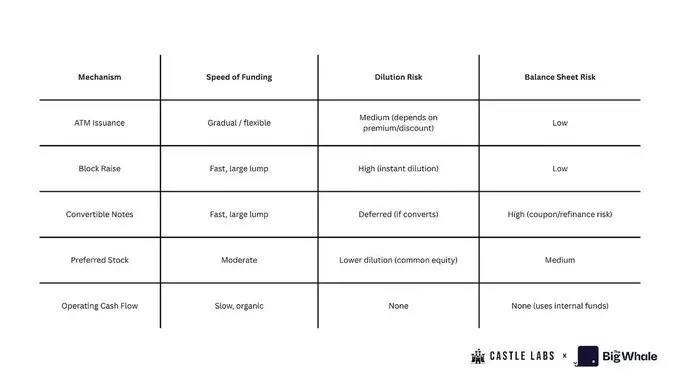

DAT Financing Mechanisms

DATs can raise funds for their treasuries through various methods, mainly including:

1. ATM Issuance

Companies establish an ATM issuance program with investment banks, gradually selling shares in the market, and using the proceeds to purchase crypto assets. This method is suitable when the stock trading price is higher than NAV, and is a flexible, low-friction financing tool, but excessive use may lead to dilution of shareholder equity.

2. Block Raises / Secondaries

Companies issue a large number of shares at once and sell them to investors at a slightly lower price than the market price, used to execute large-scale crypto asset purchases. This method can quickly replenish the treasury, but may cause short-term dilution.

3. Convertible Notes

Companies issue bonds with fixed interest rates, maturity dates, and conversion clauses (can be converted into shares at a set price in the future). This method allows fundraising without immediately diluting shareholders, but if the stock price rises and remains above the conversion price for a long time, the company may require debt to be converted into equity, causing dilution; if the stock price falls, the debt remains as debt, facing repayment or refinancing risks.

4. Preferred Stock

Companies issue preferred stock to raise funds, preferred stock has priority in dividend rights and liquidation rights compared to common stock, and may come with fixed dividends, conversion rights, or special rights. This method has a lower financing cost compared to common stock, but creates a "senior equity" structure, compressing the upside potential for common stock shareholders.

5. Operating Cash Flow (OCF)

Companies do not raise new shares or bonds, but use part of their operating profits to purchase crypto assets. This is the most sustainable and least dilutive way to build a treasury, but the accumulation speed is slower.

Current DAT Landscape

Growing institutional interest in digital assets has given rise to a diverse range of DAT companies, all trying to capture one of the most important market narratives of 2025. Starting from Strategy, which initially focused on BTC, the DAT model has rapidly evolved to cover other major public chain assets such as Ethereum and Solana. Almost all DAT companies' management teams focus on improving the key metric of "cryptocurrency units per share."

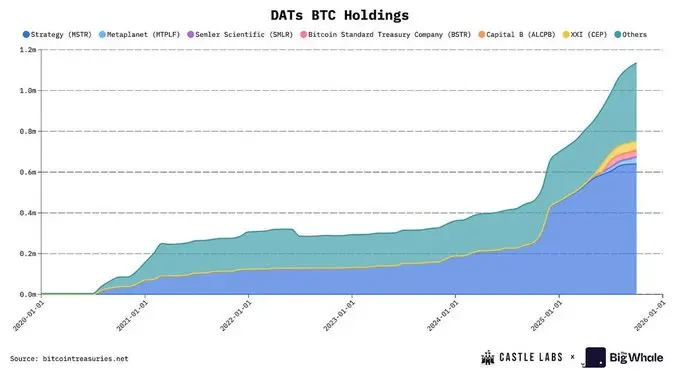

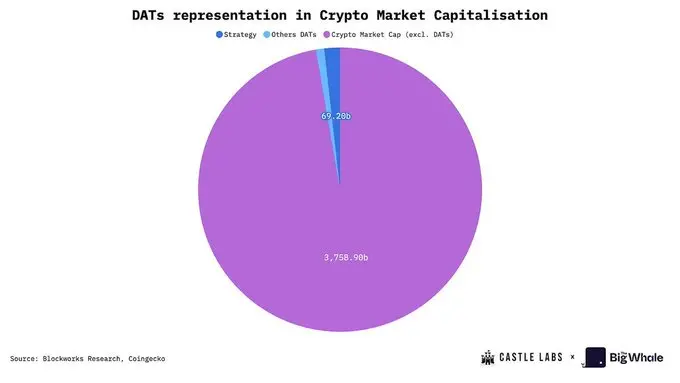

The DAT companies analyzed in this section represent the highest market capitalization listed companies in various types of crypto assets. Among them, Strategy and Metaplanet together hold 64% of the total assets under management (AUM) of all BTC DAT companies, with Strategy alone accounting for 61.22%.

Regarding ETH DAT companies, @BitMNR holds 49.66% of the total AUM of ETH DATs, while Sharplink holds 14.72%. It can be seen that early participants dominate both the BTC and ETH markets.

Strategy pioneered the DAT concept in 2020, and it took four and a half years for the market to gradually enter the mainstream stage. Now, new competitors have emerged in the BTC (Metaplanet) and ETH (Bitmine and Sharplink) sectors.

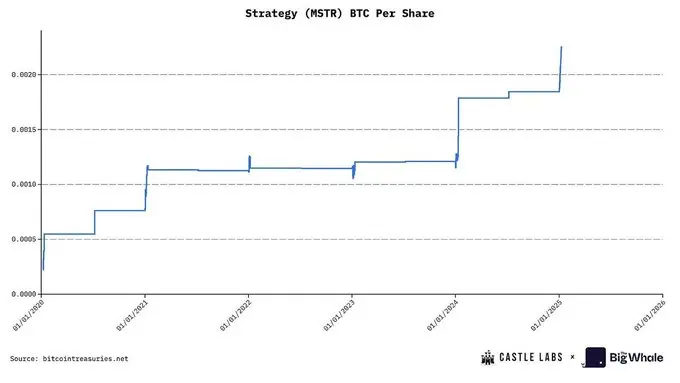

Strategy is the pioneer in this field, continuously accumulating Bitcoin. Over the past five years, the company has held 640,250 BTC, with a NAV of approximately $70 billion based on current prices. In 2025 alone, the company purchased 116,554 BTC, achieving a 26% increase in BTC holdings.

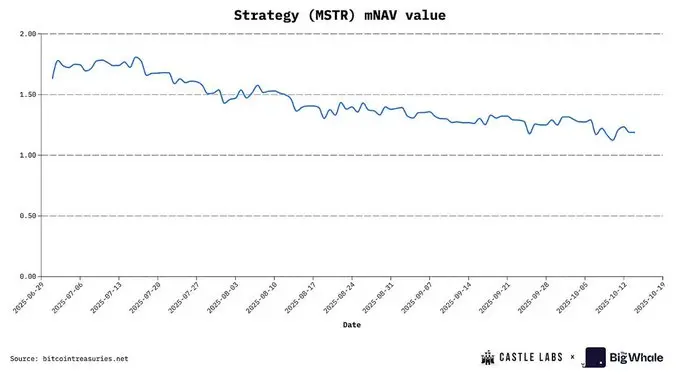

Looking at the timeline, Strategy primarily uses the ATM model to purchase Bitcoin, and in the early stages, it sold shares at a high premium of up to 6 times, then gradually declined to the range of 2.5x–3x, and now stabilizes below 1.5x mNAV, currently at 1.16x base NAV, 1.293x diluted mNAV.

MSTR's mNAV premium data source: BITCOINTREASURIES.NET

The most mainstream financing tools are preferred stock and convertible bonds, favored by hedge funds and institutional investors to hedge against the impact of ongoing equity dilution, while maintaining continuous Bitcoin accumulation.

Due to its first-mover advantage and high recognition from global stock market investors (nearly entering the S&P 500 index), Strategy has become an industry benchmark, even "too big to fail." This also means it bears great responsibility: if it fails, it could cause a structural shock to the stock market and digital asset confidence.

Another important BTC DAT company is @Metaplanet_JP from Japan. Originally operating a hotel business, it now holds over 30,823 BTC. It purchases BTC at extremely high NAV premiums, with a certain point in the year reaching an 8-fold premium, meaning that for every $1 of BTC held, $8 can be raised. One reason for such a high premium is that it is listed on the Tokyo Stock Exchange. Compared to the Nikkei Index, Metaplanet has higher volatility, providing Japanese retail investors with BTC exposure.

Now let's look at the development of ETH DATs.

BitMine was originally a Bitcoin mining company focusing on immersion cooling data centers, and in July 2025, it transformed into an ETH treasury company. Following closely was Sharplink, a company specializing in sports betting marketing technology, currently the second-largest ETH DAT. Together, these two companies hold over 3.87 million ETH, valued at over $15 billion. Their earnings per share (EPS) are 189.1% for BitMine and 98.5% for Sharplink.

Similar to Metaplanet, these two companies also prefer to use the ATM equity financing strategy, selling shares when there is a premium to effectively raise funds, without relying on dilutive block raises or debt financing, thus achieving an increase in the number of crypto assets per share. Once the premium disappears, mNAV falls below 1, causing dilution and reducing the number of crypto assets per share. Currently, Sharplink's mNAV is 0.92x, slightly discounted; BitMine's mNAV is 1.18, with an 18% premium.

A major advantage of ETH DATs is the ability to earn native yield through staking ETH. This is an automated mechanism that increases the number of ETH per share. Additionally, staking rewards can be used to enhance the annual percentage yield (APY), such as investing in DeFi protocols or repurchasing shares, and Sharplink is employing this strategy to offset the dilution effect from the ATM strategy.

Besides MSTR, most DAT companies are still in the early stage. Aggressive capital raising behavior reflects their desire to act quickly during bull markets and seize the opportunities brought by the convergence of the equity market and the digital asset market.

Risks of the DAT Model

The core feature attracting capital inflows into DAT stocks is their "net asset value multiple" (mNAV). Speculators flood into these stocks, hoping to buy before the price of crypto assets rises, thus achieving returns of 1.5 to 7 times per dollar invested. However, there is a critical issue here: investors are not directly buying Bitcoin or Ethereum through these companies, but rather purchasing a "volatility wrapper," whose entire value is determined by the mNAV at which the DAT is currently trading. Therefore, this type of investment comes with significant risks, and market participants must remain vigilant.

One of the main risks of the DAT model comes from the commercial mechanism used to accumulate BTC and ETH. The most direct factor affecting the stock price is continuous equity dilution. From 2022 to the end of 2024, Strategy averaged a 45.88% dilution of shareholders per year; Metaplanet's dilution rate is expected to reach 98% by the end of this year. In comparison, BitMine and Sharplink have very high dilution rates, 24.25% and 11.4%, respectively, mainly due to their use of the ATM model to purchase ETH. Sharplink's dilution rate is calculated quarterly (Q1 to Q2), and BitMine's dilution rate is based on a full dilution estimate of its $2.5 billion ATM plan at the current stock price.

Due to negative operating cash flow (MSTR's second quarter operating cash flow was -34 million USD, Sharplink was -1.62 million USD), DAT companies usually choose the ATM model to purchase crypto assets. However, this method is only effective when there is a premium in the market; once a discount occurs, the company cannot maintain the purchase pace, causing the number of crypto assets per share to stagnate, leading to further selling pressure from investors.

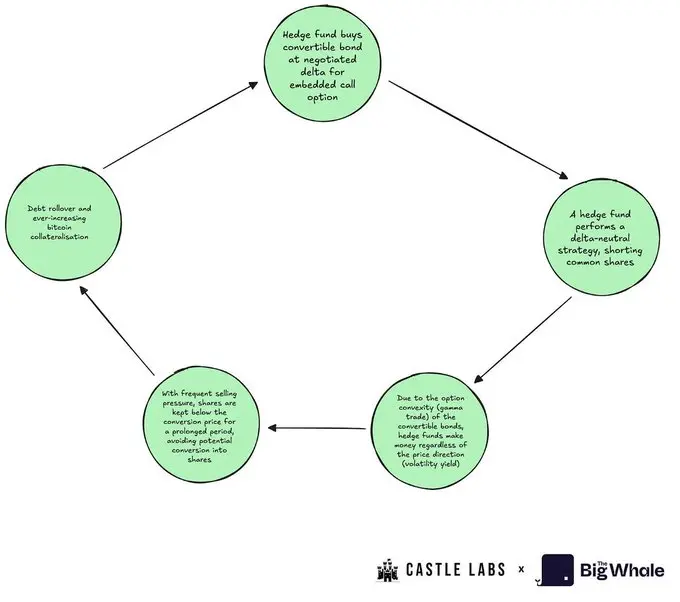

To avoid continuous dilution, MSTR and other companies choose to raise funds through convertible bonds. Convertible bonds are usually purchased by hedge funds, who use "delta-neutral strategies" because the bonds contain out-of-the-money (OTM) options. Funds establish short positions, creating continuous selling pressure.

At the same time, rising stock prices increase bond value, as OTM options appreciate. Bonds also come with small annual interest, further enhancing returns. When the stock price approaches the conversion price, the bond's delta increases, and its value rises accordingly.

Conversely, when the stock price declines, hedge funds can profit from the short position, and due to the excess collateral of BTC holdings and common stock, the bond value does not fall rapidly, forming "option protection," i.e., the convexity of the bond.

Ultimately, convertible bond holders often prefer not to convert into shares: they have maximum BTC allocation rights in the event of company bankruptcy and can utilize volatility gains for a long time. Hedge funds' ideal scenario is debt rollover — as long as the actual volatility of the common stock is sufficient to support sharp price fluctuations (requiring speculative buyers to participate), they will continue to hold convertible bonds.

The third financing method is issuing preferred stock. This strategy was pioneered by Strategy, aiming to hedge dilution without significantly increasing debt. Preferred stock typically offers annual dividends, but since DAT companies often have negative or very low cash flows, this further weakens their profitability.

In addition, there are other risks worth noting, including insufficient treasury transparency, stock buyback execution risks (lack of revenue or liquidity), liquidity risks during emergency sales, and continued selling of stocks by company insiders, all of which collectively put significant pressure on the stock price.

Recently, we have seen the market capitalization of these DAT stocks shrink significantly: MSTR fell by 44%, and Metaplanet dropped more than 70%. These risks have been fully priced in the market, showing that the DAT model may be losing momentum, which also explains why, in the current bull market, DATs are not performing as well as the crypto assets they hold.

Strategy vs BTC recent three months performance

BitMine vs ETH recent three months performance

Can DATs Exceed BTC and ETH?

Using Ethereum as a treasury asset allows DAT companies to earn an annualized yield of about 3.18%, which helps improve the EPS of ETH. However, even with the most mature DeFi protocols, without additional capital injection, DATs need a considerable amount of time to significantly increase the EPS of ETH, and also introduce counterparty risk. Although staking and yield farming can generate cash flow for ETH and other altcoin-type DATs, the current scale of these yields is still limited, making it difficult to provide substantial assistance. To truly build a self-sustaining ETH treasury flywheel, the company must accumulate enough capital to generate sufficient returns to cover all expenses and enhance shareholder value.

As for yield-oriented DATs (such as ETH DATs), whether they can outperform BTC DATs depends on the market's preference for the underlying assets they rely on. Currently, the market shows stronger preference for BTC DATs, especially MSTR's mNAV performance is more stable, compared to BMNR and SBET, it has more stickiness.

The market has already started pricing in risks for these assets, leading to noticeable differences in performance among various DATs compared to BTC or ETH, with the underlying assets outperforming their equity wrappers.

Since the core business model of DATs is to purchase underlying assets, their intrinsic value is difficult to exceed the net value of the assets they hold. Coupled with ongoing losses in operating cash flow, dividend pressures, and rising debt levels, these are the main reasons for the continued decline in most DAT multiples.

Before making investment decisions, investors often need to weigh the opportunity cost of fund allocation. Below is a simplified example showing the specific manifestation of this opportunity cost:

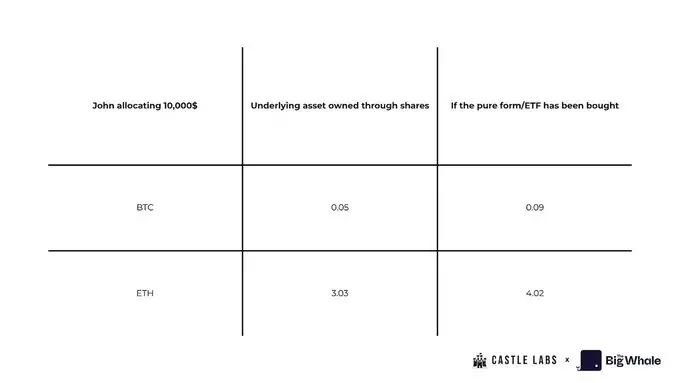

John plans to invest $10,000, choosing to directly purchase BTC and ETH spot or ETFs at the end of Q2, or to purchase MSTR or SBET stocks.

If John chooses to invest the entire $10,000 in spot, he will get: approximately 0.093 BTC (calculated at Q2 closing price); more than 4 ETH (calculated at Q2 closing price)

If he instead buys MSTR and SBET stocks, he will get: 24.61 shares of MSTR; 1,064.96 shares of SBET (calculated at June 30 price)

Multiplying the number of shares by the current number of BTC per share, John will hold about 0.04 fewer BTC than directly purchasing spot, the worst case is that he holds MSTR stock instead of Bitcoin. Similarly, if he buys SBET stock, he will hold 1 fewer ETH than directly purchasing spot.

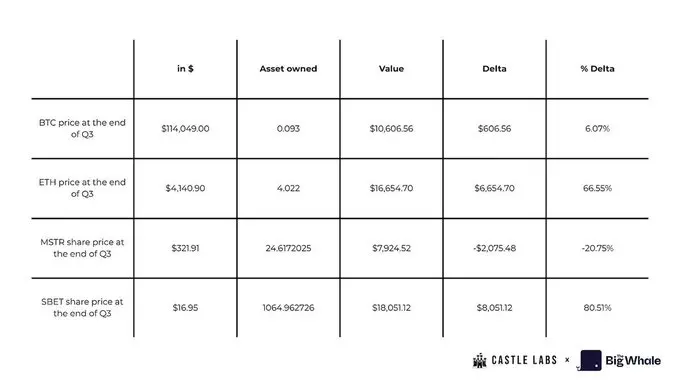

However, it is worth noting that if John does not sell any shares by the end of Q3, he will make approximately $8,000 in profit on Sharplink stock, as its stock price rose by 80%, outperforming spot and ETF returns. On the other hand, his loss on MSTR stock is approximately -20.75%, which is the loss of the original investment portfolio.

The opportunity cost of DATs is high, and retail investors ultimately cannot truly own the underlying assets. Once the company goes bankrupt, the claim rights to the underlying assets belong to creditors and preferred stockholders. This raises serious questions about the sustainability of DATs as long-term investment tools.

Nevertheless, there is one differentiating factor that attracts capital: DATs offer the possibility of amplifying returns, which is more speculative compared to holding spot or ETFs, as demonstrated by Sharplink's performance from Q2 to Q3.

Although the income statements of DATs may look good under FASB accounting standards (allowing unrealized gains to be counted in profits), these gains are still marked-to-market, and only become free cash flow when the assets are sold. In other words, these gains are just changes in asset values on paper, and unless realized, they cannot be converted into actual cash.

Theoretically, if the company can use excess cash to lend or create stable income through option contracts, these issues can be mitigated. However, each protocol integration adds counterparty risk, raising doubts about whether it is worth it. The market generally believes that once these companies start selling their holdings, it will be a fatal blow to shareholder confidence.

Sustainability Assessment

Although there is no perfect set of metrics to cope with the volatility of digital asset prices, this section will introduce several key indicators to comprehensively assess the performance of DATs.

We will take Strategy (MSTR) as an example to illustrate how to conduct the assessment and scoring. The score range for each indicator is 0–5 points:

· Score ≥ 4: The indicator performs well

· Score = 3: The indicator performs moderately

· Score ≤ 2: The indicator performs poorly

· Score = 0: The indicator performs extremely poorly

1. Dilution Risk

Dilution risk arises when the issuance of new shares affects the existing shareholders' crypto per share (CPS). If the CPS after the issuance is lower than the current CPS, it is dilution; otherwise, it is accretion.

The way to assess dilution risk is to track the change in CPS, comparing the CPS before and after the financing.

MSTR: Strategy frequently uses ATM equity issuance and convertible bonds to purchase BTC. Since MSTR usually issues equity when the stock trades at a premium (mNAV > 1), it can be considered as "accretive dilution." However, its reliance on continuous financing makes its dilution risk relatively moderate. Therefore, we give it 3 points.

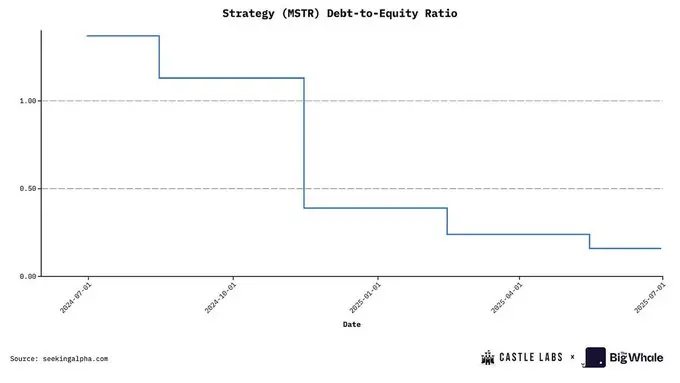

2. Leverage Level

Assessing the leverage level of DATs hinges on tracking the debt instruments used to purchase digital assets, including convertible bonds, mortgages, or other similar financing methods.

A commonly used indicator to measure leverage is the debt-to-equity ratio, used to determine the impact on the company's leverage level when the treasury assets experience a significant drawdown, and whether it could trigger a liquidity crisis.

MSTR: Strategy's current debt-to-equity ratio is 0.36, which is at a historical low, classified as low leverage, so we give it 4 points.

3. Choice of Underlying Asset

The quality of the crypto assets held by DATs is crucial to aligning with investor interests. Most DATs revolve around blue-chip assets, such as BTC, ETH, and SOL.

The advantage of ETH lies in its sustainable earning capacity, which can support company operations or expand the treasury. The crypto per share (CPS) is also an important indicator. For example, the current annualized staking yield of ETH is approximately 3%, if a DAT holds $1 billion in ETH, it can earn an additional $30 million in annual income just through staking. The company can also choose to participate in lending or liquidity provision, which are more attractive earning opportunities, but this also introduces counterparty risk, and Solana DATs face the same issue.

In contrast, BTC lacks active earning capacity, and its appeal mainly comes from its positioning as "digital gold"—limited supply and monetary attributes. More and more companies have included BTC in their balance sheets, reflecting the increasing importance of BTC as an asset.

MSTR: Strategy holds BTC, although its status as an asset is rising, it currently lacks a significant earning mechanism (which may improve in the future). Therefore, we classify it as medium, giving it 3 points.

4. Net Asset Value Multiplier (mNAV)

mNAV is one of the simplest and most effective indicators for assessing the state of a DAT, calculated as the company's market value divided by its treasury net asset value (NAV).

MSTR: Strategy's current market value is $82.3 billion, and its NAV is approximately $70 billion, with a base mNAV of 1.16 and a diluted mNAV of 1.25.

According to the base mNAV value, we can score as follows: mNAV > 1.2: score 4 or 5 (good performance); 1.0 < mNAV < 1.2: score 3 (moderate performance); 0.8 < mNAV < 1.0: score 1 or 2 (poor performance); mNAV < 0.8: score 0 (extremely poor performance)

Therefore, Strategy scores 3 points on this indicator.

5. Treasury Transparency and Governance

This is a somewhat qualitative indicator used to assess the quality and frequency of disclosures regarding the treasury, reserve proofs, and audit history of the company. Whether to provide public addresses for tracking is also an important reference.

Some companies avoid public addresses because they may trigger front-running: the purchase activities of DATs may push up asset prices, which can be exploited by the market.

MSTR: Strategy maintains limited transparency in reserve proofs, often criticized by the market. Additionally, its governance structure is relatively complex, involving various tools such as preferred shares and convertible bonds. Therefore, we give it 2 points.

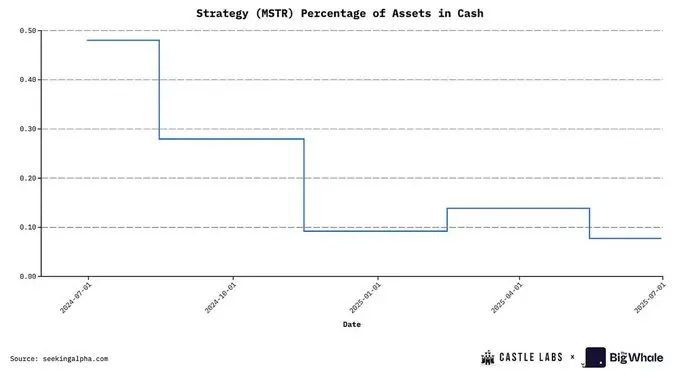

6. Liquidity and Cash Runway

This is a quantitative indicator used to analyze the company's current cash flow situation and whether it needs to sell crypto assets to maintain operations if problems arise.

The evaluation method is to divide the company's monthly operating expenses by its cash holdings to determine its runway. Having at least one year of cash runway is considered good practice.

MSTR: Strategy's current cash assets account for only 0.07% of the company's total assets, with a very low cash ratio, so we give it 1 point.

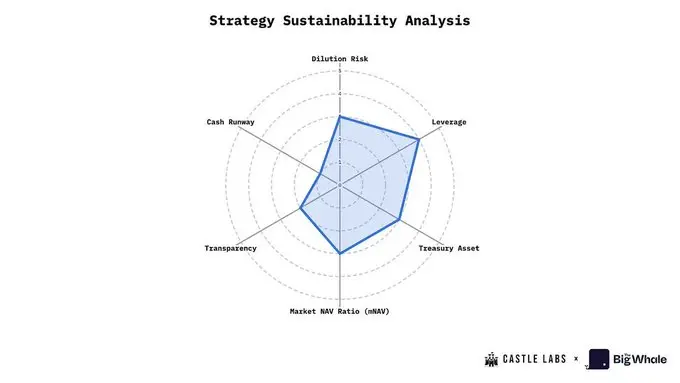

To help readers better understand the overall performance of DATs, we have included six key indicators in the assessment chart, including: dilution risk, leverage level, treasury asset quality, net asset value multiplier (mNAV), transparency and governance, and cash runway.

Remember: the higher the score, the better the performance of the DAT in that indicator (for example, the higher the leverage score, the lower the debt level, and the more robust the performance).

Taking Strategy as an example, its average score across the six dimensions is 2.83 points (out of 5 points).

Conclusion

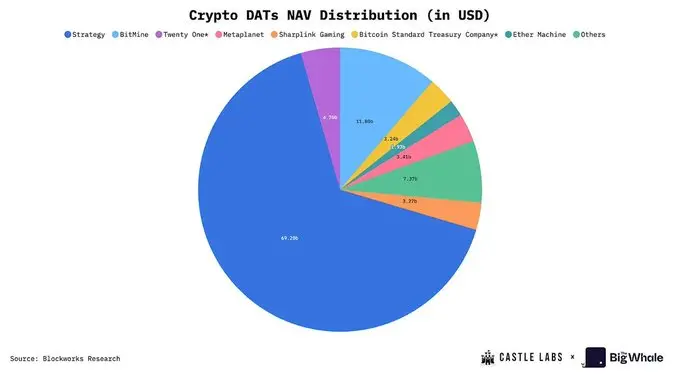

The development of DATs in the industry has been quite significant, with cumulative net asset value (NAV) of approximately $108 billion, accounting for about 2.5% of the total cryptocurrency market value. This figure itself is already very impressive, and the largest participant, Strategy, holds 3% of the global Bitcoin supply. In addition to these figures, the DAT model itself is highly attractive, as a "asset accumulation tool driven by equity financing," allowing traders and institutions to gain exposure without directly holding or trading crypto assets. Its core logic is to arbitrage through the premium or discount of company stocks.

Today, the scope of DATs has expanded from Bitcoin and Ethereum to other major public chain assets such as @Solana. These new assets provide DATs with more leverage space, such as earning income through DeFi. These earnings can be used for company operations or to improve business metrics. For example, staking ETH can increase the ETH holdings in the company's treasury, thereby increasing the value of ETH per share, which is a key metric that investors consider when evaluating stocks.

The growth of DATs and their key business metrics are highly dependent on the price performance of the digital assets they hold. In times of increased market volatility, their mNAV may drop significantly.

Ultimately, the surge in the number of DATs and their NAV also reflects the growing interest of institutions and retail investors in digital assets, which is a positive signal for the entire industry. However, any investor participating in such assets should fully understand the potential risks, as outlined in this report.

Original Title: narrative crypto vs usable crypto

Original Author: @0xnoveleader, Castle Labs; @BukovskiBuko3, The Big Whale

Translation: Peggy, BlockBeats

Disclaimer: Contains third-party opinions, does not constitute financial advice

OpenClaw Practical Guide

This column focuses on the real progress of Agents: technological evolution, application implementat

Crypto Weekly

Tracking on-chain movements of the smart money and institutions

Frontier Insights

Spotlight on Frontier, trending projects, and breaking events

Blowup Alert

As the 2026 crypto bear market deepens, exit scams and project blowups are becoming increasingly fre

Regulatory Watch

American Crypto Act – timely interpretations of policies worldwide

Popular Airdrop Tutorial

Selected potential airdrop opportunities to gain big with small investments

FusnChain

FusnChain