The market is accelerating its decline, will MicroStrategy sell BTC?

The market is accelerating its decline, will MicroStrategy sell BTC?

Since October, the cryptocurrency market has been in a correction phase, with Bitcoin prices continuously declining, and the stock price of MicroStrategy, as the "leveraged Bitcoin exposure for U.S. stocks," has also faced pressure. Under this dual decline, whether this global largest corporate BTC holder is at risk of default, and whether it will sell its core holdings in the future, has become the focal point of market attention.

Recent Market Dynamics

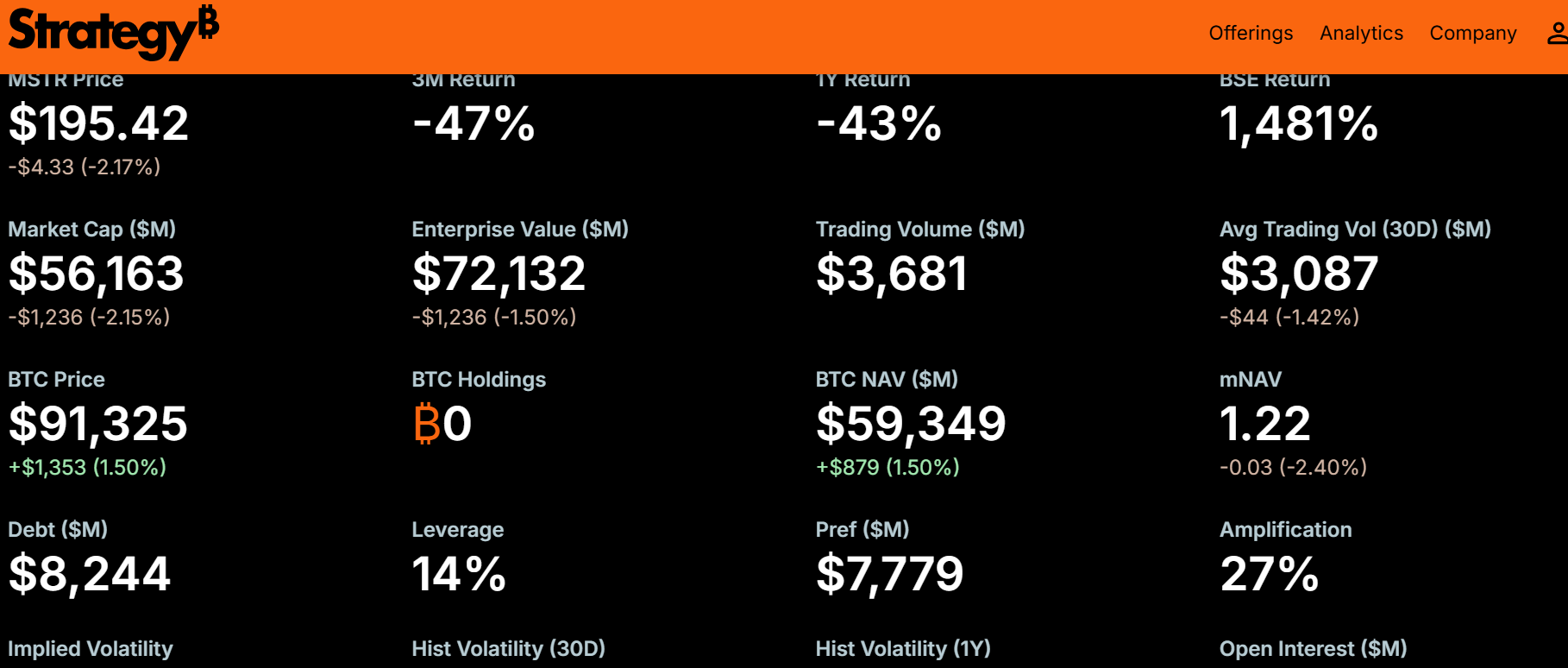

Entering November, Bitcoin prices ended the previous high-level consolidation, falling below $90,000 today, reaching as low as $89,200, representing a near 30% pullback from the October peak. Affected by this, crypto-related stocks have generally faced pressure, and MicroStrategy has also weakened. The company's stock has declined by 43% year-to-date, and today it fell below $200, marking a nearly 60% drop from its annual high of $460, twice the decline of BTC.

The market interconnectivity has been particularly significant during this adjustment: MicroStrategy's market capitalization has dropped to approximately $56.1 billion, while its held 649,870 BTC, valued at approximately $59.4 billion at current prices, making the market capitalization lower than the book value of BTC holdings for the first time, indicating that the long-standing valuation premium is beginning to shrink. This change has raised market concerns, as the investment appeal of MicroStrategy, originally an "indirect Bitcoin holding tool," is being undermined by direct Bitcoin holding channels.

Facing market volatility and speculation about selling, MicroStrategy's Executive Chairman Michael Saylor has repeatedly publicly stated his firm commitment to the company's Bitcoin strategy.

Saylor further revealed that the company will not sell BTC, but instead is "accelerating purchases" and plans to announce a new batch of purchases in mid-November. He maintains that the current BTC price is at a "strong support level" and predicts that by the end of 2025, Bitcoin will surpass gold and the S&P 500 index, with the long-term growth logic remaining unchanged. This statement continues his past style — viewing BTC corrections as buying opportunities rather than signals of strategic adjustments.

Company Financial Condition

From the perspective of asset size, MicroStrategy's current financial condition has a certain safety cushion. As of November 2025, the average cost of the company's BTC holdings was approximately $74,057, and the current market price is still higher than the cost line, maintaining an overall floating profit status. From the leverage perspective, its current leverage ratio is approximately 20%, far lower than the leveraged companies like FTX that previously collapsed, with asset size five times its liabilities, theoretically requiring BTC to drop by 80% to $18,800 before assets fall below liabilities.

However, the debt structure harbors hidden risks: the company still has $1.01 billion in convertible bonds due in 2027, with an annual payment of approximately $689 million in 10.5% preferred dividends, constituting continuous cash flow pressure. If including preferred shares and debt, the company's enterprise value has reached $7.54 billion, exceeding the BTC holding value corresponding to the current market capitalization, meaning actual valuation premium still exists but has significantly shrunk. Additionally, the company's net working capital in 2024 has turned negative, and if BTC prices remain low, it may trigger liability reclassification under accounting standards, further deteriorating financial indicators.

Three Core Challenges Highlight Operating Pressure

- The Valuation Premium Myth Fails: MicroStrategy's mNAV (market capitalization divided by total debt and BTC holding value) has fallen from over 2 times its peak to around 1.22 times, with investment banks downgrading target prices, believing that the contraction of the premium has weakened its potential for capital market profits.

- Decreased Financing Attractiveness: With the popularity of direct Bitcoin holding tools such as Grayscale BTC Trust, the uniqueness of MicroStrategy as a "U.S. stock Bitcoin leveraged tool" is being eroded, reducing investor motivation to buy.

- Over-Reliance on BTC for Performance: The company's main business contributes little, and its stock price is highly tied to BTC trends. Analysts estimate that to achieve a $20 billion revenue goal for the fourth quarter of 2025, BTC needs to rise to $150,000 by the end of the year, with a significant gap between current prices and targets.

No Immediate Risk of Default, Low Probability of Selling BTC

From the current financial structure, the probability of MicroStrategy experiencing debt default in the short term is low. Core supporting factors include: first, the current BTC price is still higher than the average cost, and the holdings have not suffered any substantial floating losses, ensuring sufficient coverage of debt by assets; second, the main debt is concentrated in 2027-2029, with no rigid repayment pressure in 2025-2026, so there is no need to sell BTC to alleviate liquidity crises in the short term; third, the leverage ratio is at a relatively safe level, with no strong risk exposures such as BTC collateralized loans, maintaining financial flexibility.

Market institutions have also given relatively optimistic expectations: 13 analysts maintain a "buy" rating for MicroStrategy, with an average target price of $526.08, offering more than 169% upside from the current stock price. Even if BTC prices continue to decline, as long as they do not fall below $50,000 and the duration does not exceed six months, the probability of the company selling large amounts of BTC is less than 20%.

MicroStrategy's long-term fate remains highly tied to the Bitcoin market: if BTC regains its upward trend, the company can continue its purchase strategy through stock issuance and debt refinancing, and the valuation premium is expected to recover; however, if BTC enters a prolonged bear market and falls below the cost line, it could trigger a chain reaction of liability reclassification and refinancing difficulties, potentially facing liquidity pressure when debts mature in 2027.

Notably, the company's SEC filings indicate that if it cannot generate sufficient cash flow to repay debt or maintain operations in the future, "it may need to sell Bitcoin," leaving legal space for strategic adjustments in extreme scenarios. However, based on current statements and strategic inertia, the Saylor team will not deviate from the core position of "accumulating and holding BTC long-term" in the short term, and selling the holdings would likely be a last resort in case of a debt crisis, not an active strategic adjustment.

In summary, although MicroStrategy currently faces multiple challenges such as stock price declines, premium contraction, and debt pressure, its financial safety margin still exists, and there is no immediate risk of default in the short term. Whether or not it sells BTC in the future depends on Bitcoin price movements and progress in debt refinancing: it is highly probable that it will maintain its holding strategy, and only in extreme scenarios where BTC drops significantly and debt cannot be refinanced, it may consider small-scale sales of BTC to alleviate liquidity pressure.

Disclaimer: Contains third-party opinions, does not constitute financial advice

BTC OG Insider Whales Representative: Cryptocurrency is still enduring a long winter, while other assets have shown signs of improvement

15 mins ago

Analysis: After recent pullbacks, whale activity on Binance has surged, with an average daily inflow of 3,200 BTC over the past month.

23 mins ago

US futures rally extends gains

34 mins agoJapan and South Korea stock markets opened and closed higher, with the Nikkei 225 reaching a new all-time high, while Samsung Electronics and SK Hynix posted substantial gains.

35 mins agoAnalysis: The options mechanism breaking through Bitcoin's $70,000 support is reversing, and the market may be poised for a rebound

40 mins agoJupiter Litterbox Trust has cumulatively purchased over 7.9 million JUP tokens this month, valued at approximately $1.49 million

1 hour agoCybersecurity Leaders Unite in Call to Lift Restrictions on Anthropic Mythos Model

1 hour ago