How Hyperliquid Rewrites Prediction Markets via HIP-4?

How Hyperliquid Rewrites Prediction Markets via HIP-4?

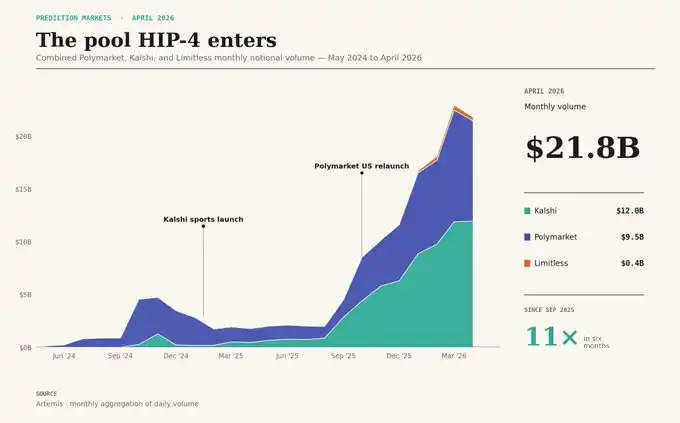

Introduction: Prediction markets are emerging as the latest hotspot in the crypto space. In April, Polymarket and Kalshi collectively achieved $22 billion in trading volume, marking an 11-fold increase in the category over the past six months. However, compared to centralized platforms, on-chain prediction markets remain significantly smaller—precisely the gap HIP-4 aims to fill.

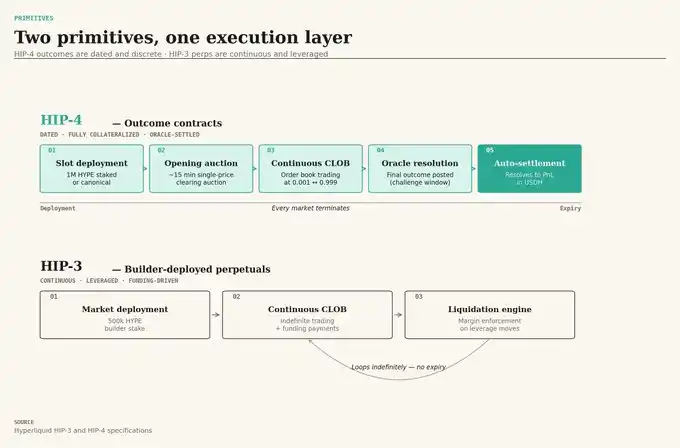

Hyperliquid’s HIP-4 is not merely a clone of Polymarket on-chain. Its core innovation lies in integrating prediction markets directly into Hyperliquid’s existing perpetual futures and spot trading infrastructure: leveraging the same CLOB matching engine, settling in USDH with full collateralization, and enabling future permissionless market creation via staking 1 million HYPE tokens.

What truly matters isn’t whether HIP-4 can replicate Polymarket—but whether it can pioneer a new trading paradigm: event contracts that share margin with BTC perpetuals and spot positions. For example, traders could simultaneously go long on BTC perpetuals while purchasing a result contract on “whether BTC breaks $80,000 this week.”

Certainly, HIP-4 still faces several unproven assumptions. Its oracle mechanism prioritizes speed, but the settlement process for complex scenarios like sports events, elections, or macroeconomic data remains unclear; the launch timeline for liquidation fees, portfolio margining, and permissionless market deployment also requires further validation.

Thus, HIP-4 represents Hyperliquid’s redefinition of prediction markets—not a direct competition with Polymarket, but a proof-of-concept that prediction markets can become integral components of leveraged trading systems. The mechanism is now live. What remains is whether the market actually needs it.

Below is the original text:

Hyperliquid activated HIP-4 on mainnet on May 2, 2026—just four days after Polymarket launched CLOB V2 and migrated to $pUSD.

These two upgrades were scheduled within the same week—not by coincidence.

HIP-4 is not a copy of Polymarket. It introduces a novel primitive atop the same execution layer powering Hyperliquid’s perpetuals and spot markets. Built around three constraints that existing prediction platforms struggle to meet simultaneously: unified margin across perpetuals and spot; end-to-end on-chain transparency; and permissionless deployment via staking 1 million $HYPE tokens.

This article dives deep into the mechanism: what each component does, why it must be a distinct contract type, and the cost of using it.

In April alone, Polymarket and Kalshi recorded $22 billion in trading volume.

The prediction markets category has grown 11x over the past six months.

Sports markets drove Kalshi’s monthly volume to $12 billion. Geopolitical markets fueled Polymarket’s growth. Limitless, the closest on-chain comparable, has also surpassed a notable scale.

On-chain prediction markets are two orders of magnitude smaller than their centralized counterparts—exactly the opportunity HIP-4 targets.

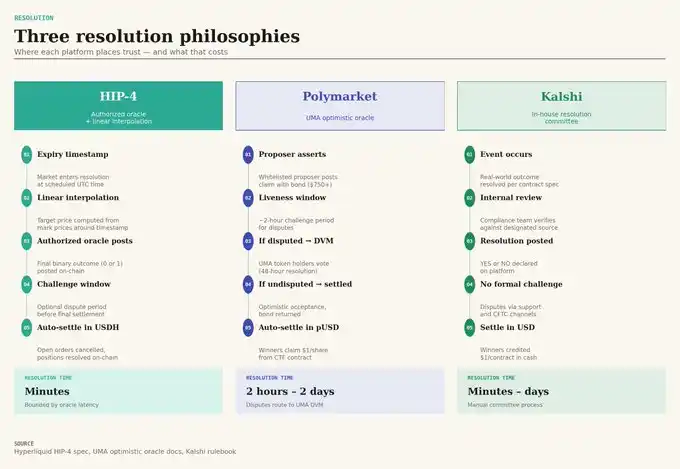

HIP-4 is a binary contract. Price ranges from 0.001 to 0.999, settles at either 0 or 1, and is fully collateralized in $USDH.

This aligns with the models used by @Polymarket and @Kalshi.

The real difference lies in all the surrounding mechanisms built around this contract.

HIP-4’s Lifecycle

HIP-4 markets have defined expiration times. Upon opening, they undergo a 15-minute liquidation auction—inspired by stock markets—to prevent the first trade from arbitrarily anchoring the market price.

Subsequently, the market runs on the same CLOB matching engine as Hyperliquid’s perpetuals and settles on-chain in USDH.

The first mainnet market was a daily-cycling BTC binary contract:

Staking 1 million $HYPE enables hundreds of daily-cycling contracts. By reusing market slots, capital costs are amortized across the entire contract series.

Why HIP-3 Can’t Do This

Hyperliquid already supports permissionless perpetuals via HIP-3. So why can’t result markets be deployed directly on HIP-3?

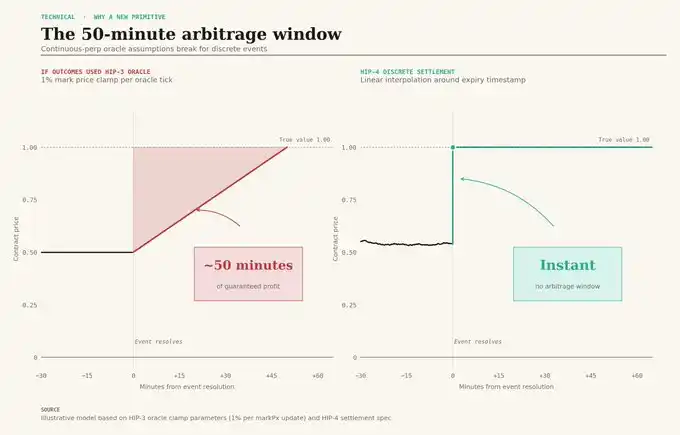

Because HIP-3’s oracle architecture would be catastrophic for binary contracts.

HIP-3 caps oracle tick updates to within 1% of the mark price. This works for perpetuals like $$WTIOIL or $$TSLA—but not for a contract requiring instantaneous settlement from 0.50 to 1.00 upon event resolution. That constraint creates a fatal flaw.

Under this limit, the mark price would require approximately 50 consecutive ticks to reach the true settlement value.

This means any observer watching the market gains nearly 50 minutes of near-risk-free arbitrage opportunity.

HIP-4 sidesteps this entirely. It uses linear interpolation based on the expiry timestamp, with authorized oracles submitting binary results and optional dispute windows, enabling instant settlement.

That’s why HIP-4 must be a standalone contract type: the mechanism itself is the product.

Three Things Only HIP-4 Can Do

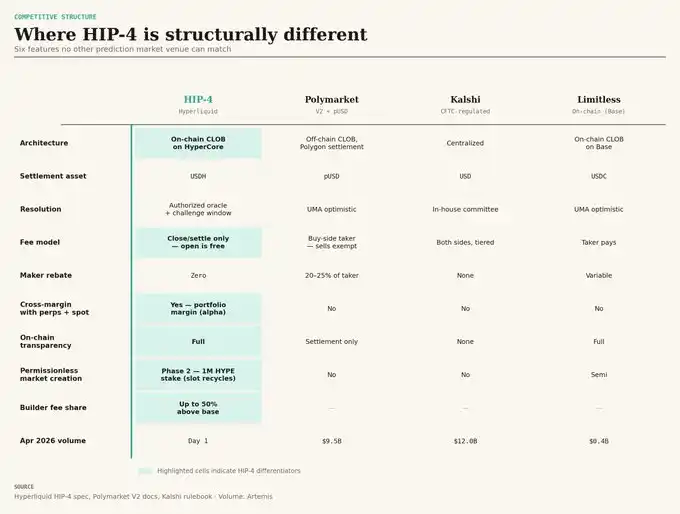

Shared margin with perpetuals and spot. A BTC perpetual long position can share the same $USDH collateral with a BTC “break above $80,000 this Friday” outcome contract. Polymarket operates on Polygon; Kalshi exists within broker accounts. No prediction market platform currently offers unified margin with leveraged perpetuals—none.

End-to-end on-chain operation. Polymarket V2 still uses off-chain matching. Kalshi lacks any on-chain structure entirely. Every step of HIP-4 runs on HyperCore: order submission, matching, settlement, oracle confirmation.

Permissionless deployment via confiscatable staking. Stake 1 million $HYPE, and your assets may be confiscated if misbehavior occurs—confiscated assets are destroyed. Beyond base fees, deployers can earn up to 50% of the builder fee. In Phase 2, market creation shifts from a manually curated listing function to a fully deployable, revenue-generating pipeline.

The cost? HIP-4 launched without maker rebates—unlike Polymarket, which pays makers 20–25% of taker fees. For HIP-4 makers, income comes solely from spread capture. Another asymmetry exists: fees are charged only upon liquidation, not upon opening.

Free entry, paid exit. No other platform does this.

Speed Comes at a Cost

HIP-4 prioritizes speed: authorized oracles, result confirmation within minutes. UMA’s optimistic oracle is slower but battle-tested across billions in dispute volume. Kalshi’s committee mechanism is fast under normal conditions but becomes opaque in edge cases.

A more honest assessment: in current documentation, HIP-4’s oracle architecture is the least thoroughly described part of the spec. (It’s possible deployers could choose different oracles, as in HIP-3.)

For daily BTC binary contracts, the oracle is HyperCore’s mark price—backed by years of operational data and relatively reliable stability.

But what about sports, elections, or macroeconomic data releases? This oracle infrastructure hasn’t been publicly designed yet.

1. Liquidation-side fee basis points. Documentation confirms zero fees on opening, non-zero fees on closing—but exact rates remain unpublished. Polymarket’s effective take rate is ~35 bps of volume; April’s $8.1 billion volume generated ~$28 million in fees. HIP-4’s fee range likely falls between 5 and 50 bps. Until these numbers are revealed, all revenue projections are speculative.

2. Portfolio margin officially launched. Cross-margining is HIP-4’s core differentiator.

3. First non-curated builder. Phase 1 still involves validator curation. Phase 2 opens deployment to anyone willing to stake 1 million $HYPE and hold conviction on a specific market. The first independent builder’s market and chosen asset class will reveal whether HIP-4 becomes a standalone product—or just a feature module within Hyperliquid.

Can daily BTC binary volume rival Polymarket’s BTC 24-hour price market? When will Phase 2 launch? When will the first builder emerge? When will the portfolio margin milestone be reached? When will the liquidation fee schedule be published?

HIP-4 doesn’t aim to defeat Polymarket on its home turf.

It seeks to become a venue where event contracts share collateral with leveraged perpetuals; a system where market creation becomes a permissionless revenue stream; a platform where every step—from order placement to settlement—is fully on-chain.

This is a different product.

The mechanism is viable. The real question is: does the market need it?

The next 90 days will tell.

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

06-16

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

06-16Amazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

06-16Binance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

06-16Binance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

06-16

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

06-16SlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

06-15