Distribution is King: Robinhood Is Eating the Prediction Market

Distribution is King: Robinhood Is Eating the Prediction Market

Fidelity, Schwab, and Interactive Brokers grew up in an era before prediction markets existed. Even spot cryptocurrencies represent only a minor fraction of their overall product offerings. In contrast, Robinhood serves a younger demographic that may want to bet on sports events, go long on semiconductor stocks, trade Solana frequently, and hold crude oil futures positions—all within the same platform. A generation raised on monitoring market sentiment will gravitate toward platforms like Polymarket or Kalshi if Robinhood fails to offer comparable risk assets.

One way to mitigate this risk is by offering event contracts—binary instruments that settle with a “yes” or “no” outcome. Each contract trades between $0 and $1, reflecting the real-time market probability of an event occurring. If your prediction is correct, the contract settles at $1; otherwise, it settles at $0. The entry cost for users is precisely the implied probability of the event. For example, a $0.60 contract on the Strait of Hormuz reopening before May 30 signals the market’s collective belief. When most participants are confident an event will happen, the profit potential from betting on it becomes minimal.

On Robinhood, these tools serve as hedging instruments. You can go long on the Strait of Hormuz reopening while simultaneously going long on crude oil prices, assuming oil prices will remain elevated if the strait remains closed.

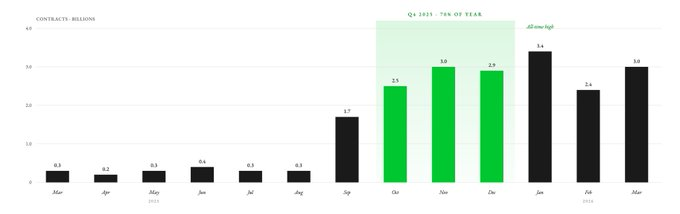

Robinhood launched its prediction market business in March 2025, routing client orders through KalshiEX. Within nine months, users had traded 12 billion contracts. Approximately 70% of the annual trading volume was concentrated in the fourth quarter. In Q1 2026, Robinhood recorded 880 million event contracts.

Over 1 million Robinhood customers traded event contracts in 2025. Rather than launching its own markets or building liquidity, Robinhood directly integrated Kalshi’s prediction market infrastructure. It acts as a distribution layer by providing clients with a dashboard. The entire backend infrastructure remains under Kalshi’s control—at least for now (details to follow).

Kalshi and Polymarket dominate the space, capturing over 90% of total prediction market volume. Robinhood distributes Kalshi’s contracts to its 27.4 million paid users, who invest across equities, crypto, futures, options, and other asset classes. Kalshi is merely a prediction market platform and lacks the scale of distribution that Robinhood provides.

In fact, Robinhood accounted for 50% of Kalshi’s trading volume during Kalshi’s first year.

While Coinbase allows users to trade equities, crypto, futures, and options (via its acquisition of Deribit), it only launched its prediction market in January 2026. By comparison, Robinhood has operated its prediction market business for over a year, generating annualized revenue exceeding $415 million. Robinhood also boasts significantly higher monthly active users—13.5 million versus Coinbase’s 9.2 million.

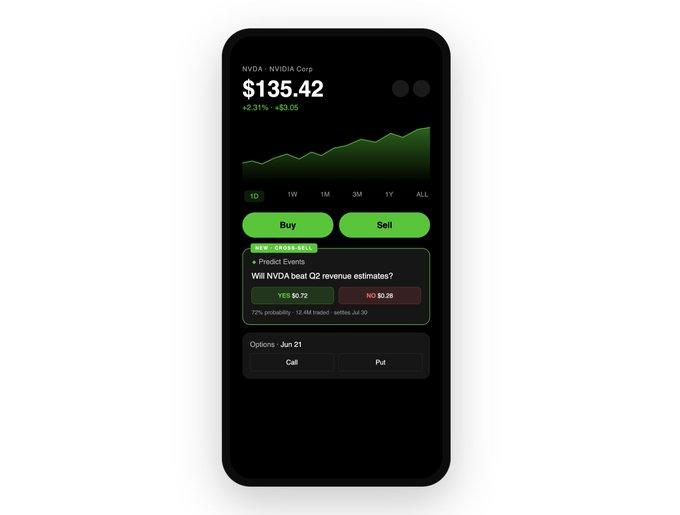

Prediction markets on Robinhood have further potential to evolve. Currently, they exist as a standalone Hub disconnected from the rest of the platform. But soon, they will be cross-linked with equities, options, and crypto—allowing stock traders on Robinhood to directly purchase event contracts.

Imagine opening Nvidia’s stock page ahead of its earnings report. You see standard information: stock price and option chain. Now, you also see a nearby event contract: “Will Nvidia exceed Q2 revenue expectations?” This contract trades at $0.72, indicating the market assigns a 72% probability to the event. You believe the market underestimates demand for Nvidia’s products.

In this scenario, Robinhood lets you buy shares, buy call options, or purchase 500 “Yes” contracts for $360. If correct, you earn $140 (0.28 × 500). All three tools appear on the same screen—no tab switching required.

As illustrated with crude oil earlier, you can use these tools to hedge positions. Bet on Nvidia beating expectations while shorting the stock to hedge your exposure in the prediction market. Thus, Robinhood enables users to build cross-asset hedging strategies in under a minute, all on one screen.

So far, this integration into the stock trading interface has worked well for Robinhood—but it still leaves money on the table. That’s about to change, as Robinhood prepares its next strategic move.

Richer Context for Information Pricing

Robinhood’s moat lies in delivering all relevant information at the precise time and place users need it. The era of buying Bitcoin on Coinbase, trading options on Deribit, holding stocks on Robinhood, and trading crude oil futures via IBKR is over. Users now seek to avoid context switching and platform hopping.

Once Robinhood embeds prediction markets across all asset pages, it evolves from a passive broker into an information pricing platform. Beyond price and analyst ratings, Robinhood will provide real-time probability markets tied to relevant events for each stock. Event contracts reflect the live consensus of participants putting real capital at stake. These contracts empower users to make better decisions—even if they’ve never traded a prediction market contract before.

Taking Nvidia again as an example: stock prices at any moment reflect the sentiment of equity holders. Alongside ownership come legal rights, shareholder reports, analyst Q&A sessions, and a 400-year-old framework protecting investors. Yet most traders don’t care about these. What they really want priced is “Will Nvidia exceed revenue expectations?” In such cases, prediction markets may actually serve as a superior pricing signal compared to stock prices. Robinhood’s effort to integrate derivatives, event contracts, and equities under one roof aims to capture value from every user potentially interested in trading that event.

But Polymarket and Kalshi have been doing this for years. Where, then, is Robinhood’s moat? Why not simply integrate third-party markets into its interface to boost revenue, instead of owning them outright? Cross-selling and trading volume reveal the true incentive structure.

Cross-Selling as a Regulatory Moat

In March 2026, two bipartisan bills were introduced aiming to ban sport-related event contracts at the federal level. State-level legal barriers also exist. For platforms like Kalshi, this poses an existential threat—their 2025 revenue was 89% derived from sport-related contracts. Polymarket’s unexpired interest shows around 60% tied to sports-related events.

If sport contracts face regulatory setbacks, Kalshi and Polymarket will suffer the worst impact. Without this dominant category, they cannot sustain valuations above $20 billion. While Robinhood began with a heavy focus on sports, its cross-selling capability allows revenue diversification into equities and macro events (earnings, Fed decisions, CPI data, employment reports).

For Robinhood, sports are just one revenue stream. For Kalshi, the sports category is nearly everything. Any regulatory crackdown on sports-related markets could undermine Kalshi and Polymarket’s ability to justify valuations exceeding $20 billion. Robinhood now occupies a stronger position in its value chain through Rothera, a joint venture.

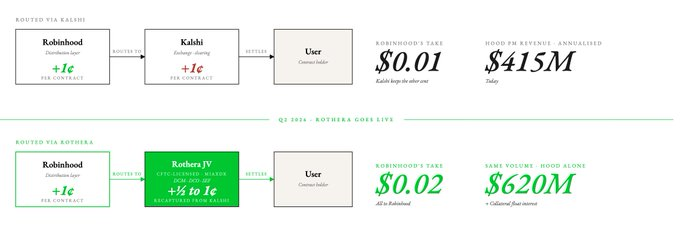

In November 2025, Robinhood established Rothera LLC, a joint venture that subsequently acquired MIAXdx—a CFTC-licensed Designated Contract Market (DCM), Derivatives Clearing Organization (DCO), and Swap Execution Facility (SEF). This fundamentally reshapes the economics, control, ownership, and clearing/settlement processes of event contracts.

Reliance on Kalshi to supply prediction markets limited the types of contracts Robinhood could list. Rothera enables Robinhood to launch any event contract at any time.

Economically, this could mean Robinhood captures the current one-cent fee currently flowing to Kalshi—and doubles the event contract revenue. If Robinhood redirects half of this income into its core entity, using current contract fees, its prediction market revenue could increase by 50%, reaching $620 million.

We have reason to be optimistic about this joint venture, as its latest quarterly results show Robinhood beginning to invest in Rothera. Q1 2026 includes $14 million in JV-related costs. There’s also a secondary benefit: once prediction market contracts route through Rothera, the collateral supporting open positions will be included on Robinhood’s balance sheet, adding interest income. When collateral size reaches approximately $100 million, this could generate an additional $4–5 million in annual revenue.

Every trading platform has a simple mission: get traders to move funds as frequently as possible, charging small fees per transaction—or encourage them to park large amounts of idle capital, retaining interest income. For Robinhood, the latter strategy appears to be the prevailing approach.

Robinhood’s cross-selling moat in prediction markets mirrors what we previously identified for Hyperliquid’s HIP-4 event contracts. Hyperliquid’s unified risk engine integrates spot, perpetuals, deployment markets, and prediction markets into a single primitive, ensuring efficient capital utilization in decentralized markets. The same logic applies to Robinhood—but within a centralized environment.

Kalshi lacks Robinhood’s cross-asset distribution moat. A standalone prediction market product holds far less value than one embedded within every other trading instrument. Coinbase has just entered the prediction market space, whereas Robinhood’s full-stack asset integration with event contracts on one screen gives it a clear lead.

Numbers Speak Louder

Any discussion comparing Coinbase, Kalshi, and Robinhood valuations ultimately seeks to answer one question: what is the lifetime value per user on each platform? Kalshi users may be fewer, but they pay significantly higher fees. A single user, if Robinhood matches Kalshi’s liquidity at lower fees, would fully migrate to Robinhood.

The market already sees this difference. Kalshi and Robinhood share similar valuation multiples (both ~15x), while Coinbase trades at a lower multiple of 7.5x. For Kalshi, prediction markets constitute all revenue. For Robinhood, they account for only 7%. For Coinbase, this figure is negligible.

Once Rothera goes live, Robinhood can price its prediction markets more competitively than any independent platform. It can undercut Kalshi’s fees, absorb margin pressure, yet still grow—because every prediction market user might also be a potential customer for equities, options, or crypto. Kalshi isn’t silent: it reportedly plans to launch crypto trading, starting with perpetuals. But transitioning from a pure prediction market to a multi-asset platform is far harder than integrating prediction markets into an existing multi-asset platform.

Robinhood has spent over a decade acquiring 27.4 million paid users and establishing deep liquidity, market maker networks, compliance infrastructure, and user trust. Kalshi must start from zero.

One way to assess the business’s value is to consider spinning off Robinhood’s prediction market segment and listing it independently. If it has $415 million ARR and the same growth trajectory, how much would it be worth? The simplest answer: 15x Kalshi’s multiple, or $6.2 billion. But under identical conditions, a Kalshi with Robinhood’s revenue stream would command a much higher valuation.

We built a three-year forecast model using the following assumptions:

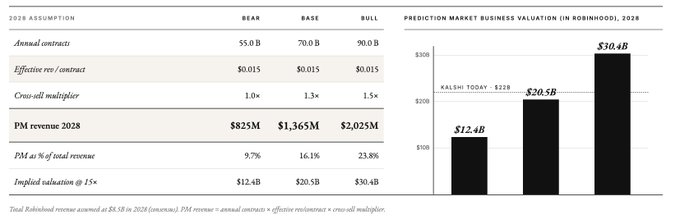

Contract Volume: Baseline scenario projects 7 billion event contracts by 2028, implying a ~40% CAGR over the next two years. Based on Robinhood’s Q1 2026 volume of 880 million (annualized ~3.5 billion).

Rothera Economics: We expect effective per-contract revenue to rise from $0.01 to $0.015 in bear case, or $0.02 in baseline/bull case (by 2028).

Cross-Selling Lift: 1.0x multiplier in 2026 (cross-linking not yet live), 1.1x in 2027 (equity page rollout), 1.2x in 2028 (mature adoption). Assumes cross-selling adds 10–20% incremental volume beyond organic prediction market growth.

Robinhood Total Revenue: Using consensus estimates—$5.4 billion in 2026, $6.4 billion in 2027, $7.2 billion in 2028.

We then stress-tested 2028 under bear, baseline, and bull scenarios.

Even in the bear case, Robinhood’s prediction market revenue alone in 2028 reaches $825 million—over three times Kalshi’s 2025 revenue ($260 million). Applying Kalshi’s current revenue multiple (15x), Robinhood’s prediction market business would be valued at $1.2 billion under this scenario. In the most optimistic case, it could reach $3 billion by 2028.

We’re likely witnessing: a distribution-moat company entering a new market and capturing most of the value for itself. The unresolved question is whether Polymarket and Kalshi are reenacting OpenSea’s 2021 fate—or can successfully reinvent themselves amid new threats. Polymarket recently expanded into perpetual products, but its users are unlikely to shift from prediction markets to perpetuals simply because that’s their original intent. In contrast, Robinhood benefits from a core user base loyal to its high-risk, zero-fee tools. This group appears better positioned than Polymarket’s.

Today, the market views Robinhood as a traditional brokerage with a side prediction market product—explaining why prediction markets contribute only 7% to its revenue. But if Robinhood CEO Vladimir Tenev delivers on his stated vision, Robinhood will become a platform that prices every financial opinion—on earnings, rates, elections, commodities—in real time, while enabling trading in the assets driven by those opinions.

A standalone prediction market only attracts users already trading event contracts. A prediction market embedded within a retail brokerage becomes an information pricing machine for everyone else. Vertical integration among capital aggregators is everywhere.

Original author: @Decentralisedco

Disclaimer: Contains third-party opinions, does not constitute financial advice

NVIDIA attracts $85 billion in investor demand during massive bond issuance

06-16

Ethereum surges over 10% in 24 hours, currently priced at $1,841.31

06-16Amazon announces a multi-billion dollar investment in Missouri to build a data center campus, expected to create over 400 long-term positions

06-16Binance Platform's SpaceX Perpetual Contract Trading Volume Surpasses $9 Billion, Capturing Over 60% Market Share

06-16Binance platform XLM/USDT short-term spike down to $0.17, now recovered to $0.225

06-16

Trump: The Strait of Hormuz has been fully reopened as of Friday, and all agreements have been signed

06-16SlowMist: Aztec Connect Contract Hacked for $2.19 Million Due to ZK-Rollup L1/L2 State Boundary Vulnerability

06-15